Cross-border going to sea is a small circle. People in the circle like to exchange and share, and go to overseas markets to search for gold together.

This article was first published on the overseas website, welcome to moveletschuhai.comSee more global business related information.

Write at the beginning: Author’s statement

The more you look at cross-border, the more you like this track. Cross-border going to sea is a small circle. People in the circle like to exchange and share, and go to overseas markets to pan for gold. This article comes from my thinking and industry research on the industry itself.

Cross-border e-commerce is nothing more than three things in my eyes: business flow, logistics, and seller service (logistics is also a service, but it is calculated separately because it is large enough). These three tracks are all in the position of capital. This article takes the business flow as the main body and elaborates on my personal point of view. I hope everyone can criticize and correct me.

1. Existing market analysis (data derived from interviews and public data compilation)

-

In the past few years, the rapid development of China’s cross-border e-commerce industry has accumulated valuable experience in cross-border e-commerce for Chinese companies, and they have seized the major opportunities released by the demand side of developed countries in Europe and America. Laid a solid foundation:

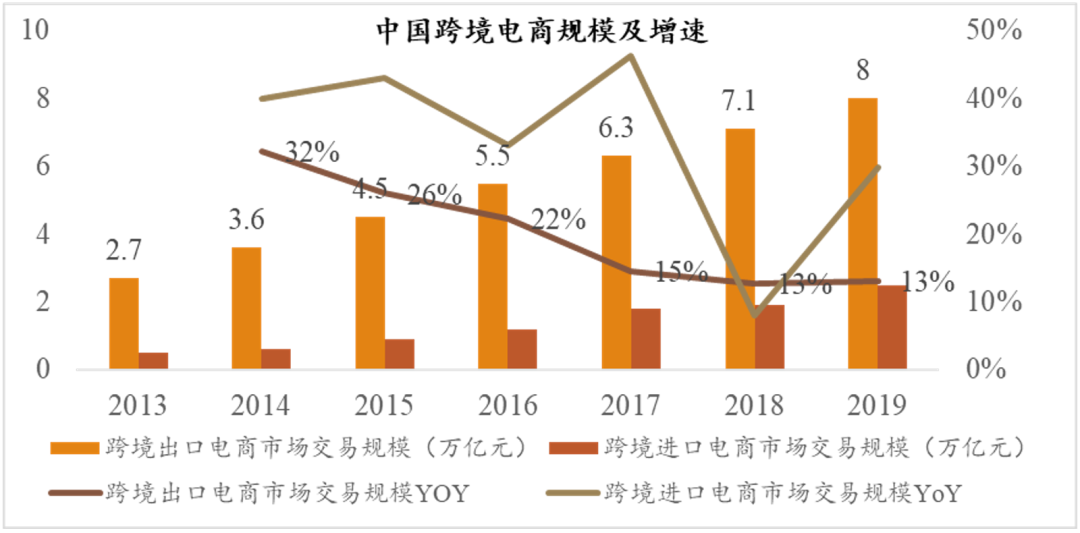

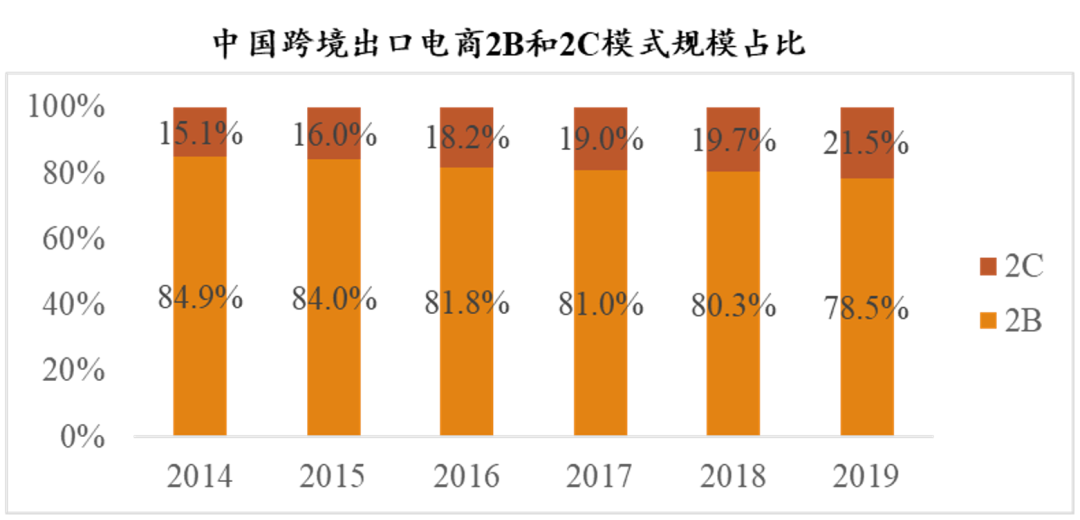

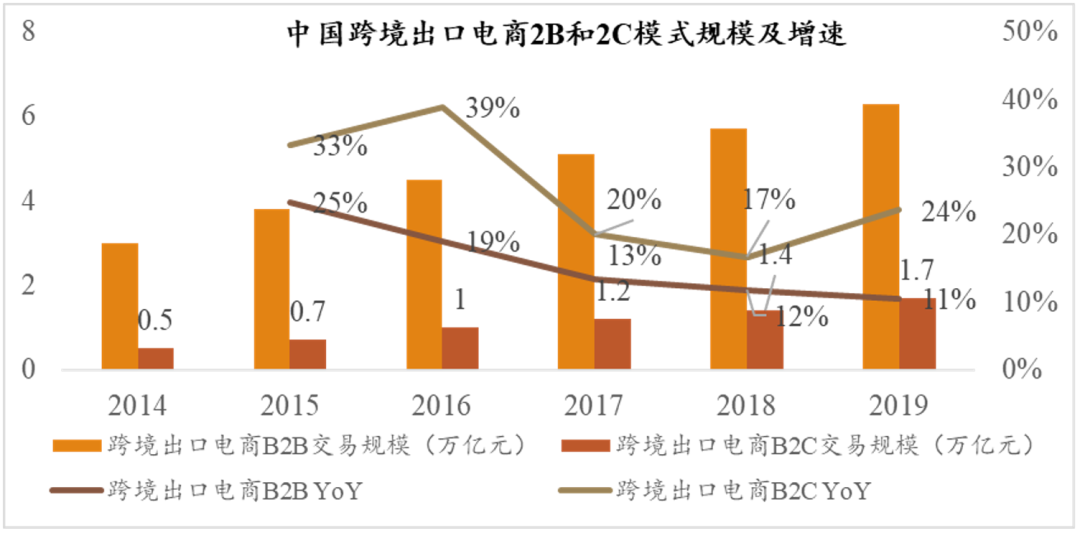

In 2019, the scale of China’s cross-border e-commerce transactions reached 10.5 trillion yuan, of which exports accounted for 76.5%. That is, the scale of China’s cross-border export e-commerce market in 2019 was about 8 trillion yuan, a growth rate of 13.1%; In terms of model, the 2C model transaction scale in 2019 was 1.7 trillion yuan, accounting for 21.5% of the total export e-commerce, and a growth rate of 23.6%. Compared with the 2B model, although 2C currently accounts for a relatively low proportion, it is gradually increasing.

-

Before the epidemic, my country’s cross-border e-commerce destinations were the hardest hit areas of the epidemic—developed countries in Europe and America:

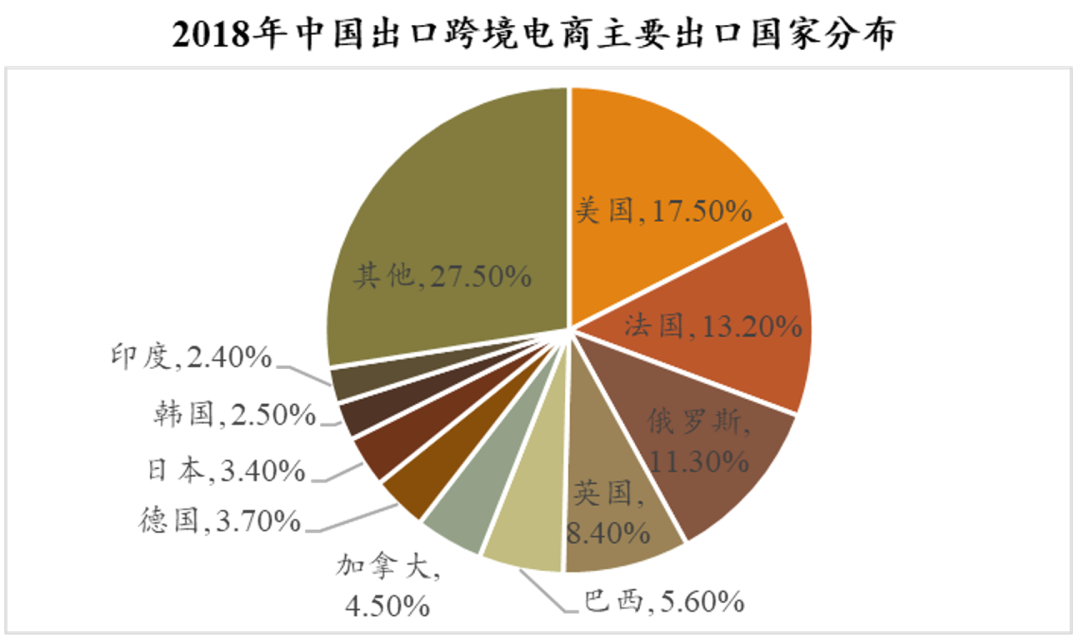

China’s overseas destinations are mainly Europe, the United States, the Middle East and North Africa, Japan, South Africa, South Africa, India, and Southeast Asia. The United States is China’s largest cross-border e-commerce exporter, accounting for 17.5%, France and the United Kingdom. Other developed countries account for the absolute majority of the total; (Russia is the headquarters of AliExpress) According to Tmall’s overseas market sales data, in terms of consumption frequency, Southeast Asia, North America, and Australia are the highest, and in terms of customer unit price, North America and Australia are the highest.

After the epidemic, cross-border e-commerce in the Pre-pay market in developed countries has benefited from the sudden increase in e-commerce penetration. We have seen many cross-border e-commerce startups have experienced rapid growth last year. .

-

The cross-border e-commerce model of Chinese sellers is more mature than other countries, and they are more willing to cooperate in localization in developed countries in Europe and America:

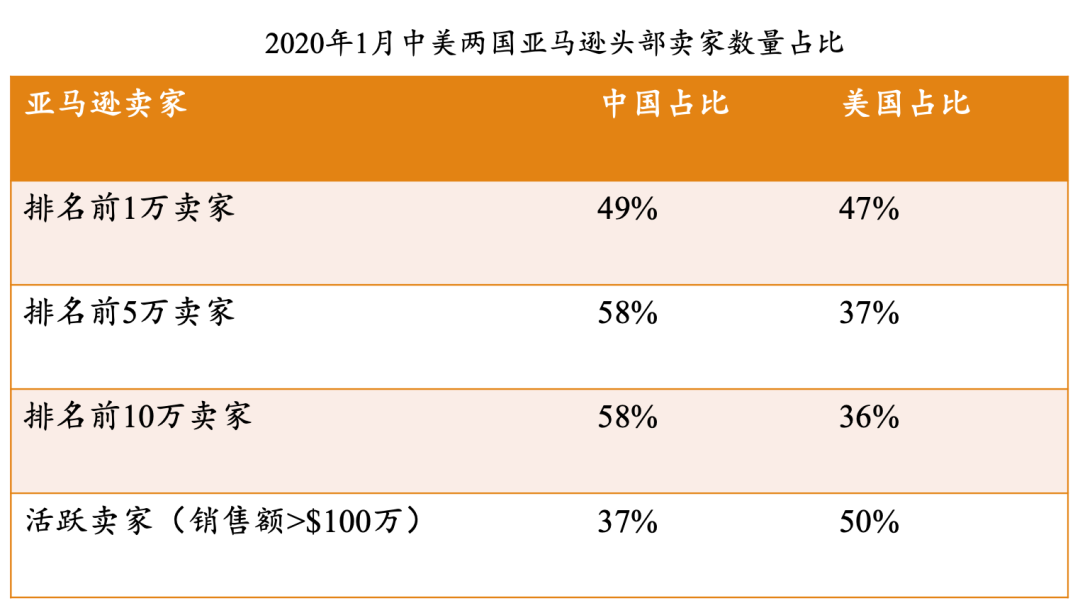

Take Amazon, the largest e-commerce platform in the United States, as an example. 95% of Chinese sellers in the top sellers of the US Amazon market use FBA, while only close to 65% of sellers in other countries use FBA. This determines the terminal logistics efficiency and also affects store rankings. , So Chinese sellers can get 49% of the top 10,000 sellers on Amazon. Other overseas platforms, such as NOON in the Middle East and Meikeduo in South America, have begun to attract Chinese sellers since 19 years.

-

Advantages of China’s supply chain: Most Chinese sellers come from the Pearl River Delta and the Yangtze River Delta, with low-cost, high-efficiency, and flexible supply chain advantages

China has become a “world factory” by virtue of its low-cost and high-efficiency manufacturing advantages, especially in the Pearl River Delta and the Yangtze River Delta with developed manufacturing industries. In recent years, the geographical distribution of sellers has continued to expand from the Pearl River Delta and the Yangtze River Delta to inland, covering more industrial belts.

Chinese sellers have continuously upgraded their ability to respond quickly to changes in the overseas environment and consumer demand. They can quickly identify global consumer trends and flexibly adjust product selection strategies, forming a flexible supply chain advantage. For example, during the new crown epidemic, Chinese sellers can quickly respond to the new needs brought about by the epidemic, and use a flexible supply chain to meet the new needs of global consumers for medical protection, personal health, household and kitchen supplies.

In addition, the advantages of China’s manufacturing industry are not only in terms of cost performance and production capacity, but also in the research and development of many categories. China has its own absolute advantage: Take Hibobi, a maternal and child overseas brand invested by the factory as an example. The research and development of fabrics for maternal and child products, the research and development and production capacity of diapers are at the world’s absolute leading level, as is the field of consumer electronics.

-

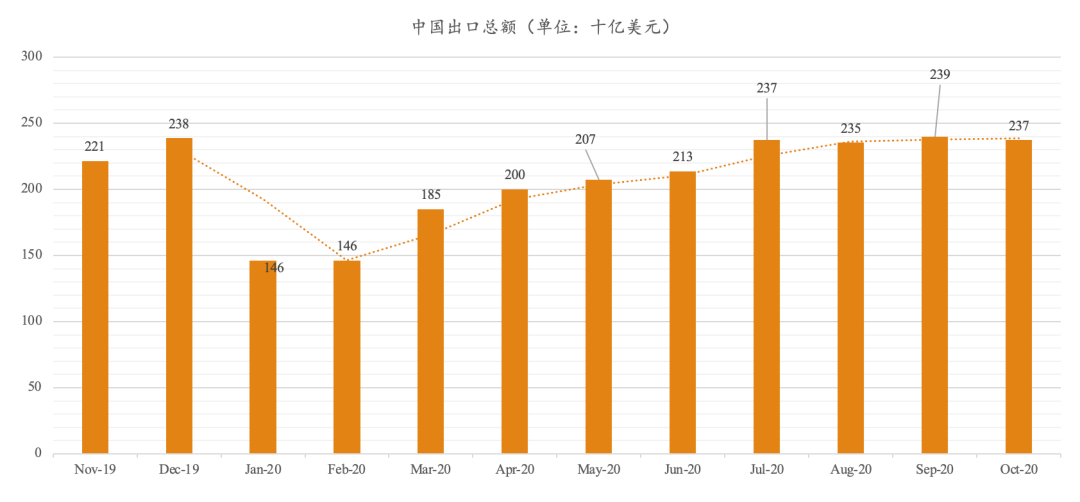

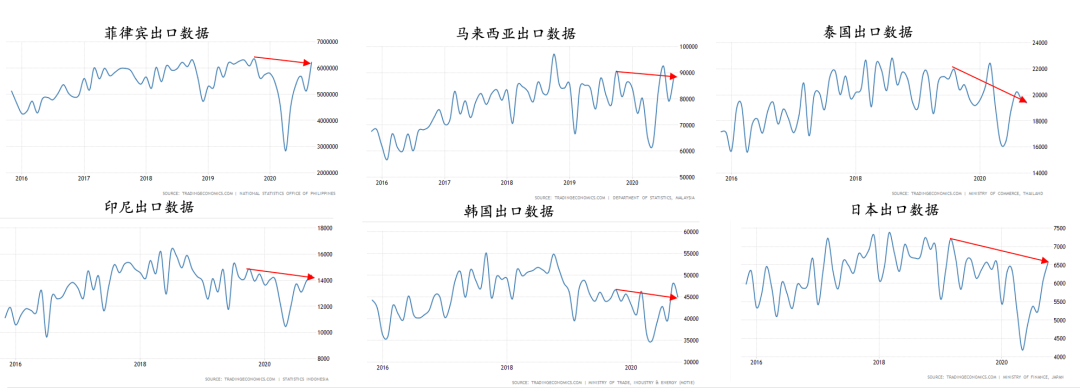

After the epidemic, China’s production capacity has recovered well and has returned to a 19-year high in the middle of 20 years, while other “industrial competition” countries in Southeast Asia have been slow to recover (except Vietnam)

2. What has changed in the market

-

Intermediate and short-term benefits

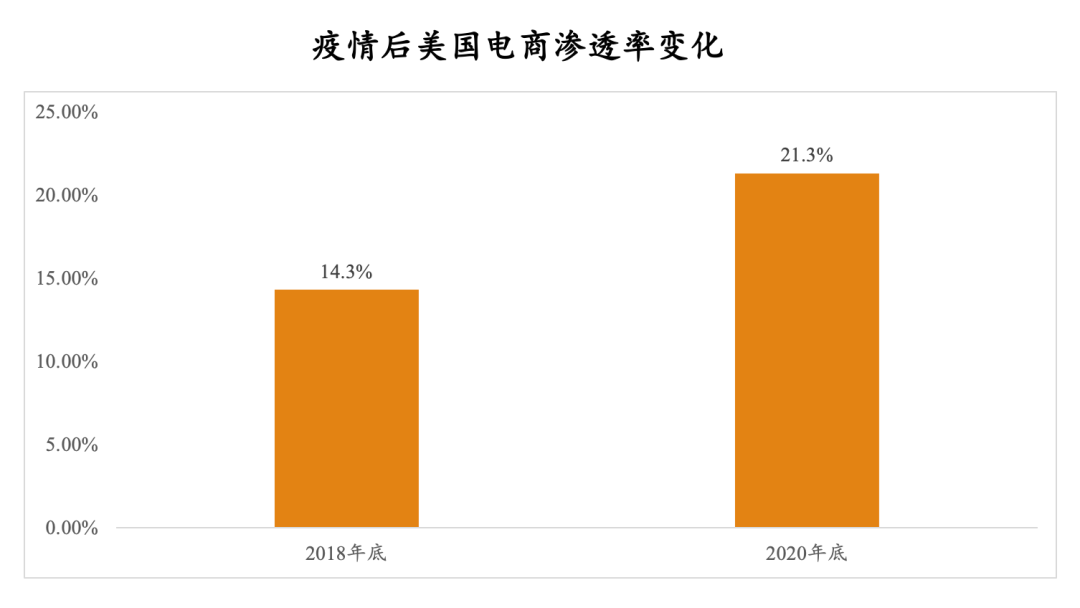

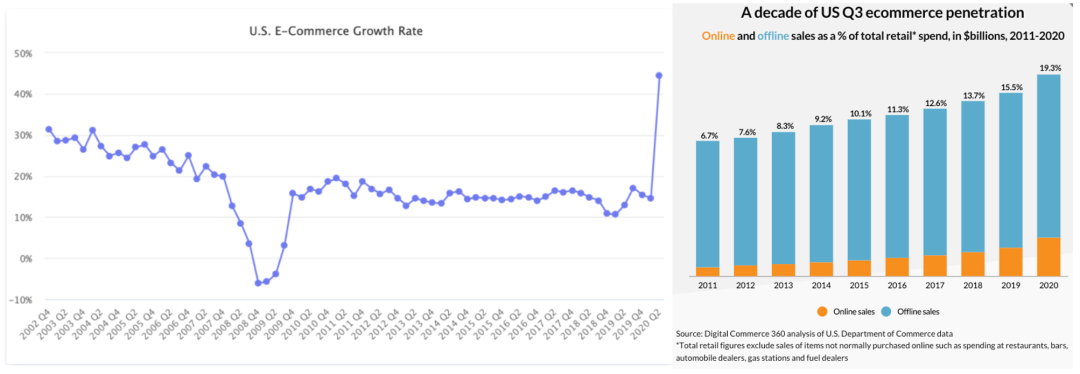

The COVID-19 epidemic has completely changed the original development path of e-commerce in the United States. Offline retail formats have been rapidly online, and the e-commerce penetration rate has increased rapidly: 14.3% before the epidemic (by the end of 2018, relatively stable), 2020 21.3% per year (U.S. e-commerce sales in 20 years were US$861.12 billion, a year-on-year increase of 44%). For online, this is a huge increase, which needs to be supported by the B-end supply chain. The domestic supply chain and seller system in the United States cannot fully undertake this change, which is bound to be made in China.

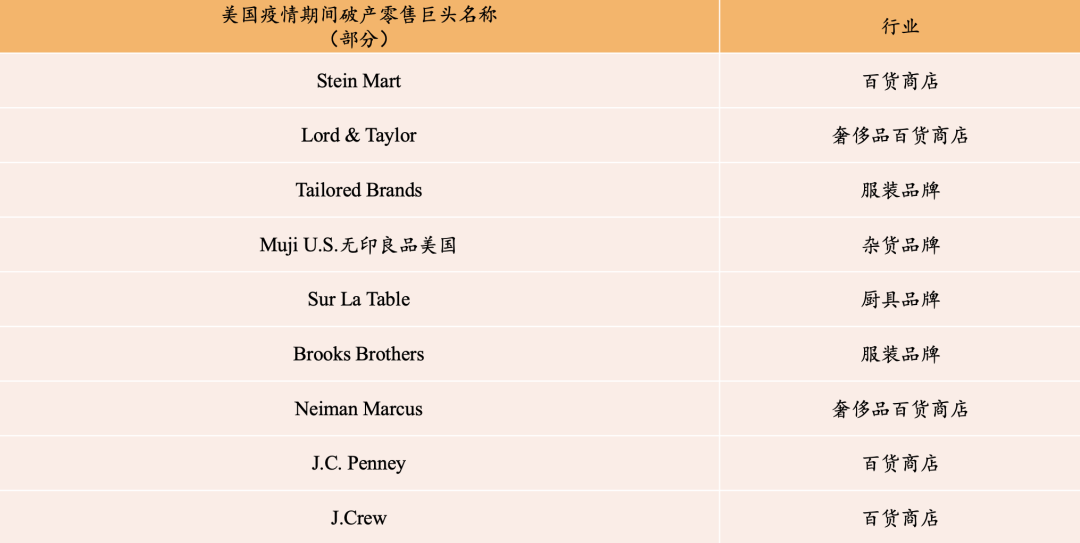

On the other hand, under the impact of the new crown epidemic, many traditional retail companies in Europe and the United States went bankrupt. In the medium term, the original brands and retail models were broken, and the consumption power of developed countries in Europe and America was suppressed. There is huge room for new channels , Brings opportunities for the birth of new brands, and creates opportunities for China’s supply chain to go overseasGreat opportunity for the brand.

In addition, in the short term, the impact of Biden’s release of water on cross-border exports: The latest estimate of the German Allianz Group on March 16th, Biden’s $1.9 trillion stimulus package will bring an additional $360 billion in 21-22 With additional import demand for goods and services, China is expected to receive an additional export demand of 60 billion U.S. dollars. This is just the additional demand brought about by the economic stimulus. (Refer to the news media extraction)

-

Long-term trend

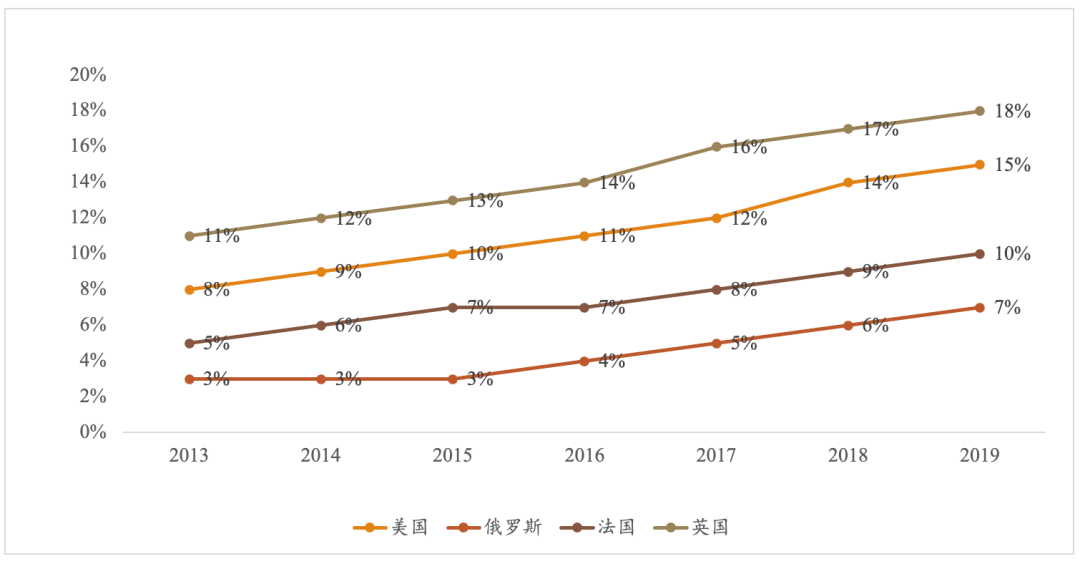

a) In the long run, the online penetration rate of developed countries in Europe and the United States is still very low, and there is huge room for growth: my country’s main export countries, the United States, France, Russia, and the United Kingdom, have seen their e-commerce penetration rates continue to rise in the past few years. The UK has the highest penetration rate, reaching 18% in 2019, followed by the US at 15%, France at 10%, and Russia at 7%, providing a good environment for my country’s e-commerce exports.

The short-term epidemic has promoted a surge in online penetration, and it is likely to be permanent: According to historical experience and data, the process of e-commerce is often irreversible, because of the changes in consumption habits brought by the epidemic (towards more convenient The evolution of the e-commerce market) has brought huge room for the increase in the e-commerce market; at the same time, the global e-commerce penetration rate has increased year by year, which also reflects our judgment. Even after the epidemic is over, we predict that the growth rate may stabilize or decline slightly, but we will not be able to return to the market before the epidemic.Accounted for.

b) Behind the process of global consumer online is not only the simple channel transformation from offline to online, but also the huge opportunity for each consumer category to re-do it and iterate with new and old brands: with Europe and the United States Compared with its own supply chain, the advantages of China’s cross-border e-commerce are mainly the full-category of China’s superior manufacturing production capacity (including excess capacity) and a large group of sellers with excellent operational capabilities; overseas sellers have far greater iteration speed and learning capabilities. Inferior to domestic products, the product iteration speed is also much lower than that of domestic products. I think the competition dimension of most categories today is still the competition between Chinese sellers and overseas local sellers and brands. In this process, Chinese sellers have the opportunity to improve their supply chain through cost performance, and gradually increase their brand premiums and seize the market share of original European and American brands.

-

Summary:

Demand side: From a long-term perspective, developed countries in Europe and the United States have a general trend of online retail, and China has an opportunity to “make it again” in various daily consumer categories; in the short and medium term, there are obvious positive factors for China and the development of Europe and the United States The country has a strong demand for China’s cost-effective products.

Supply side: China’s cross-border e-commerce has developed rapidly in the past few years, especially the developed countries in Europe and the United States as our main overseas destinations, and focus on adapting to the local business environment to accumulate overseas experience, and the advantages of Chinese cross-border overseas sellers on a global scale It is already quite obvious; China’s own supply chain has the characteristics of high cost performance. Compared with Japan and South Korea, most of the products have the same technical level but the comprehensive cost of manpower and materials is significantly lower. Compared with Southeast Asia, China’s supply chain has “high flexibility and high quality”. The characteristics of “high efficiency” have obvious competitive advantages on a global scale.

Global competition: Looking at China’s main rivals in the supply chain, the export capacity of major countries in Southeast Asia, Japan and South Korea, except Vietnam, has been significantly reduced under the impact of the epidemic, and Vietnam’s supply chain is insufficient, and the current European and American demand side releases opportunities It can be said that only China can grasp it.

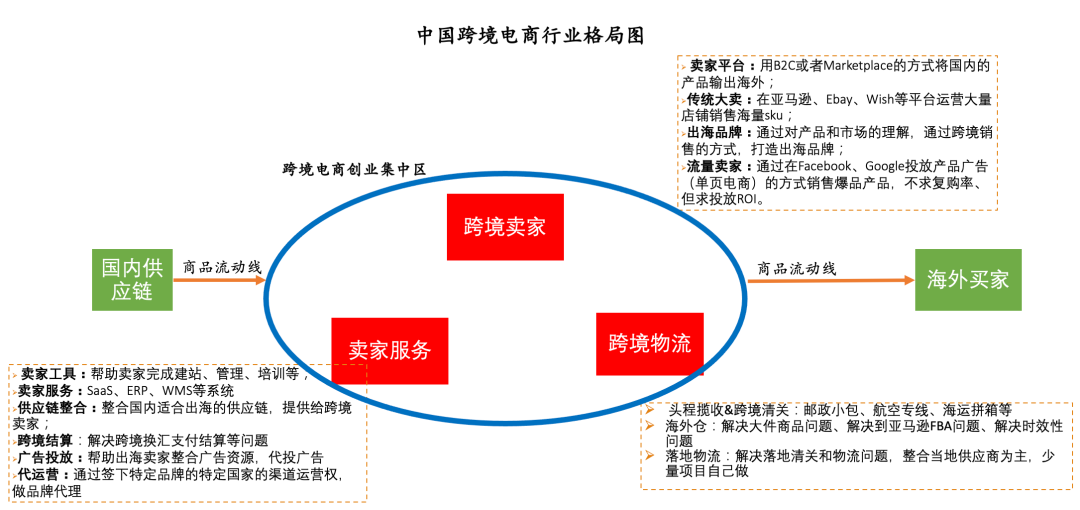

3. Take business flow as an example, the existing market structure and player types

-

Big seller

Multi-platform: The platform has been dominated by Amazon in recent years, but generally all channels are involved and distributed;

A large number of accounts: generally a single platform hasThere are hundreds of accounts, and the ban of a single account has little impact on the company as a whole;

Massive distribution, multiple SKUs: The general layout of big sellers is earlier in cross-border e-commerce, and the big sellers adopt a multi-category SKU distribution model, and the number of SKUs is generally more than 10,000; p>

Typical sales representatives include: Yougeshu, Cross-border Communication, Yibai Network, Tongtuo Technology (500,000+SKU), Aoji, etc.;

Characteristics of big sellers:

1. There are many SKUs, and a large number of products will be stocked based on overseas warehouses and FBA. The inventory pressure is high, the product turnover speed gap is large, the distribution of accounts receivable is scattered, the payment speed is slow, and the cycle is long. Therefore, Amazon’s typical big sales often have the saying “sell goods to make money but no money, the money is in inventory”;

2. Low R&D investment: Big seller does not need (or cannot) establish a brand image, and the R&D expense rate is low. For example, the R&D expense rate of Yikeshu in 2017 and 2018 is less than 1%;

3. The category is scattered, high sales costs on the platform and no scale effect can be formed, and the advantage of declining marginal costs in the later period cannot be obtained. In the sales costs, warehousing and logistics costs account for a relatively high proportion (about 35-50%); < /p>

4. The product coverage is wide, and the difference in consumer preference between different regions is balanced, and the income is relatively stable. But at the same time, the profit margin of a single product is small, and the gross profit level is relatively low;

5. The core competitiveness lies in product selection + low price + the ability to market explosive products.

-

On-site boutique sellers

Definition: The brand sellers we refer to here mainly refer to two types of companies. One is that they have a good brand accumulation in China and want to expand overseas markets through overseas sales. Sellers who use overseas as their main battlefield to occupy overseas markets with a small number of SKUs, single or a few brand images, in subsequent discussions, we generally refer to brand sellers as the second category, and the first category is not within the scope of overseas investment discussions;

Brand sellers have only one or several brands(One for each series), the number of SKUs is small (thousands or less), the third-party platform is used as the main battlefield, the independent station is used as an additional battlefield of a certain scale, and the cost-effectiveness is the main means of entering the market. Sales of more than 300 million), improve the supply chain capacity of single products, and gradually allocate staff to product research and development, and it is easy to produce explosive products under fine polishing; large marketing investment, establish a moat of brand image, and have a “station inside transfer station outside” “line” The typical “trilogy” of the brand evolution of “upstream to offline” and “export to domestic sales”.

Features:

1. Less SKU, less pressure on inventory and accounts receivable. From the perspective of the proportion of inventory to assets, the proportion of branded inventory to assets is generally lower than that of the big-selling model (brand 30-50%, big-selling 40-60%);

2. After achieving a certain scale, focus on building its own brand and high R&D investment. The improvement of brand influence requires the creation of hot items. After the hot items open the market, R&D is used to improve the product matrix and pay attention to the promotion of R&D to brand value. For example, the R&D expense rate of Anker Innovation in 2019 is as high as 6%;

3. Focus on brand exposure. In addition to on-site investment, it will also use social platforms and search engines to place advertisements, promote through social media KOLs, form word-of-mouth, and further guide consumption. Sales expenses account for a relatively high platform rate (60 -70%);

4. Enjoy the high gross profit margin brought by the brand premium. For example, Anker’s gross profit margin has been maintained at 50%+ from 2016 to 2019, and its net profit in 2019 is 11%;

5. Core competitiveness: strong supply chain self-control + marketing ability to establish brand image + localized operation ability;

6. Risk: Due to the focus on a certain category or categories, it will be greatly affected by the industry’s prosperity.

-

Independent sellers: Cross-border sellers who sell products through independent websites. There are mainly three types of independent sellers:

1. Independent platform sellers: I hope to build a platform on my own to sell goods overseas by integrating our own and introducing a three-party supply chain system. There are also pan-platforms (Jollychicwish, etc.) and vertical track platforms (Shein, etc.) Such projects are often open and closed, and they are one of the main battlefields for cross-border investment in U.S. dollars;

2. Independent website brand sellers: There is no clear distinction between this category and the on-site boutique sellers;

3. Independent station group sellers: mainly through the establishment of massive stations, promote products through purchases, no repurchase, essentially a traffic transactionIt means that in the future, we will seek to integrate the supply chain on a large scale and become a master station, but the transformation is difficult and painful.

Features:

1. Because they can’t enjoy the natural drainage of the platform without the third-party platform, independent sellers must use various channels such as Facebook, Instagram, Google, etc. to divert for themselves, and the marketing investment is large. And localized marketing capabilities are the core capabilities that all independent sellers must have.

2. For independent brand sellers, in addition to the third group of sellers, customer stickiness and repurchase rate are extremely important, so they will invest heavily in website maintenance, operation, and design. Self-built website allows sellers to master all customer data, which is convenient for follow-up marketing and optimized operations.

3. For traffic sellers, follow the trend to sell explosive products, pursue the profit of the first order, do not seek repurchase, and the product price increase multiple is relatively high. There is also a variant model of this type of seller, which cannot be expressed in words, and is a high incidence of false transactions and fraud.

4. For brands and independent sellers of big sellers, the mall attribute of the independent station will increase the customer’s stay and wandering time on the page, and it is more likely to sell other products, so the overall customer unit price is higher.

4. Where are the future opportunities?

In the past few years, Innovation Works has made many investment arrangements in cross-border overseas. On the one hand, we have invested in Snaptube, Xiaoying and other overseas-based traffic community projects at a very early time. We have also made outstanding achievements overseas. The scale of users is not bad, and it also holds a leading position in the vertical market.

In the past six months or so, we have also invested in Suntisfy, which makes toys to go overseas, and Hibobi, which is a maternal and child brand. We have also invested in Project Z for overseas post-00s newcomers. There is also an environment in cross-border logistics. World Logistics and other investment layouts. The follow-up innovation workshop going to sea team will continue to pay attention to traffic, business flow, logistics, and seller service projects.

Business flow: We continue to invest in boutique brand sellers who sell on the platform and companies with channel attributes (or potential); here we focus on categories with three major bonuses:

-

Pandemic dividends: Categories that increase the demand for more time at home (positive examples: fitness equipment, game consoles, projectors, gardening tools, etc., negative examples: travel and outdoor related, office related, etc.) Short-term demand rises, and it is easy to create new brands by occupying the market in the next one or two years;

-

Category bonus: it is a new category, or although the category is not new, it is because the new technology is in a period of rapid growth in the market; (Example: TWS headset, sweeping robot, air fryer, etc.)

-

Big-brand benchmarking bonus: There is a clear benchmarking of high-priced giants, but because of the epidemic, the overseas middle class cannot afford big-name brands. Through cost-effectiveness and clear market positioning, new brands have been given opportunities; (Dai Sen substitution, etc.)

Logistics: We pay attention to overseas warehouses, special line small packages, large-scale logistics and regional Chinese landing distribution companies;

Service: Pay attention to whether more new sellers will enter the market in the past two years, pay attention to opportunities for cross-border supply chain transformation, and pay attention to ERP and SAAS projects;

Traffic: Focus on new overseas crowds, new gameplay with platform potential, and traffic monetization dividends from TikTok commercialization and short video e-commerce.

At the end: For entrepreneurs in the industry

In the first phase of cross-border e-commerce, companies such as Cross-border Communication, Youkeshu, and Banggu were born. These companies entered the market very early and used first-mover advantages and the rise of FBA to spread the goods. Mainly. However, with massive inventory, poor product sales, and weak insights into front-end consumers, these companies are either transforming to high-quality products, or to import and export and supply chains. They are large in scale, but at the current stage, the industry is more competitive. weak.

Currently, my own understanding is the second stage of cross-border e-commerce, evolving from shop to boutique, and will gradually give birth to some influential brands in the subdivision field, the most typical cases are Anker and VeSync . China used to be the world’s factory and used the B2B trade model to continuously export a large number of products to the world. However, apart from a few categories such as mobile phones and computers, we have hardly exported very well-known overseas brands, but the world-renowned big-name products are also Most of them are produced domestically.

Carefully study the development history of developed countries and the development history of well-known brands. We can find that, due to historical origins, most developed countries have studied the needs and user preferences of most countries in the world earlier and absolutely Most well-known brands have enough time, enough cognitive reserves, and enough technology to iterate their products. The end result is that multinational brands have almost swept the world, especially in developing countries.From food (Nestle, Coca-Cola, McDonald’s), used (P&G, Philips), worn (Nike, Adidas), opened (BBA) and so on.

For domestic brands, there is a major cognition. GAP mainly comes from the fact that domestic manufacturers and brand owners have too little research on overseas market demand. It is not unwilling, but there is no way to understand it in the past. Because of the epidemic and cross-border e-commerce, for the first time, Chinese manufacturers and brand entrepreneurs have the ability to truly understand the needs of overseas consumers, iterate quickly, and continuously improve their competitiveness. Startups that have the potential to emerge in the second stage (which can achieve a sales scale of 5 billion in the next three years) often have the following characteristics:

-

Have strong operational capabilities and front-end data analysis capabilities, know how to sell to whom, and can seize market dividends to quickly increase their sales scale;

-

Through the sales scale, we have certain control over the upstream supply chain;

-

Have a certain R&D capability on a certain sales scale;

-

Enough courage and financing ability;

-

Have a big dream of being a world brand;

There are many companies currently in the second stage, and they have achieved good growth and profits in the past year and for a period of time in the future. However, I don’t think there will be many companies that can grow from companies at this stage to listed companies. Maybe in the next two years, no more than 20 companies will go public. There are a lot of companies who are not thinking about danger in peace, and who are satisfied with the annual net profit. They don’t understand why they want to raise funds. Very few companies are willing to invest heavily in research and development, branding, and compliance.

The threshold for cross-border e-commerce is relatively high. The short-term barriers mainly come from the flow of the whole chain, the capital cost occupied by FBA, and the marketing and cognition of front-end consumers. The long-term barriers remain the same as domestic brands. , Supply chain and channels; after the second stage, I think the level of competitors faced by boutique sellers in the third stage will rise rapidly. This stage may begin in the second half of 22 years. Faced with the pressure of cross-border giants to expand horizontally, they will use capital and matrix R&D capabilities to defeat (or M&A) small-scale boutique brand sellers.

The fourth stage of competition mainly comes from the overseas expansion of new domestic brands after the convergence of the domestic battlefield. Objectively speaking, there is a big gap between the R&D capabilities and brand capabilities of cross-border seller brands and domestic brands of the same level. On the one hand, the domestic market for China’s new domestic brands is still growing in the short-term, with long overseas processes, high pressure on cash flow, and short-termThe future looks down on (or don’t know how to do) the cross-border e-commerce market. The current stage of attempts is still at the stage of B2B trading, looking for an agent, or a small number of attempts. In the future, relying on the domestic conqueror’s posture, relying on research and development, brand power, and supply chain capabilities, when seeking overseas expansion, it will become a strong competitor of traditional cross-border e-commerce companies. After the third and fourth stages, the market share of cross-border e-commerce companies without R&D capabilities and brand power will be quickly eroded by the above-mentioned types of competitors, and domestic players in overseas markets will begin to converge.

The fifth stage is that China can really give birth to a wave that can compete with Dyson, Peloton and other famous overseas brands in the market where they are good at and their unit price.

In fact, the various international hot events in recent days are all competing against comprehensive national strength. This world has always been a world where whoever has the biggest fist counts. Because I see that the sea is cross-border, I have done research on the economic growth of mainstream countries and regions in the world, and I gradually understand that the opportunity to become a developed country will always belong to The fewest countries. China has gone through 40 years of reform and opening up, and its economy is growing rapidly, and it is facing a key node of upgrading and transformation. The Chinese are one of the most diligent people in the world. China has the most powerful, complete and efficient manufacturing industry system in the world. At the same time, it is becoming more and more digital, intelligent and flexible. China has the strongest in the world. The big Internet and e-commerce talents, except for chips, what we lack is that we need time and patience.

Cross-border e-commerce is a long-term track. The short-term money-making effect and the rapid growth brought by the epidemic dividend have attracted a large number of new entrants, including first-time entrepreneurs, investors and FA. I also hope that everyone can give this track more patience and time. This industry welcomes more people with long-term dreams to enter. Cross-border entrepreneurs are also welcome to communicate. Innovative Works is optimistic about this track for a long time, and is also concerned about investment opportunities in this industry.

Editor’s note: This article was contributed by the specially invited author “Ran Fei, Investment Director of Innovation Works”. Ruan Fei pays attention to the sea track, and initially focused on the domestic Internet going overseas. In 2016, he also invested in Snaptube in the first round. In 2019, he mainly focused on the Indian and Middle East market. In 2020, he began to look at cross-border e-commerce. He invested in Hibobi, Suntisfy, and Project Z. And other cross-border and overseas projects.

LET’S CHUHAI CLUB Salon Event Preview

On April 15th, the first salon of LET’S CHUHAI CLUB, created by going overseas, will land in Shenzhen. This event will start from several hot topics such as brand going overseas, cross-border e-commerce, financial technology and overseas marketing, and discuss how Chinese companies going overseas can plan and move under the wave of globalization, and talk about current crises and challenges.

Welcome to scan the code to fill in the form and register for offline participation.