At present, commercial and residential apartment projects on the market are generally surplus.

Editor’s note: This article comes from Zhongjing Jingwei , author Liu Hongli, reproduced with permission.

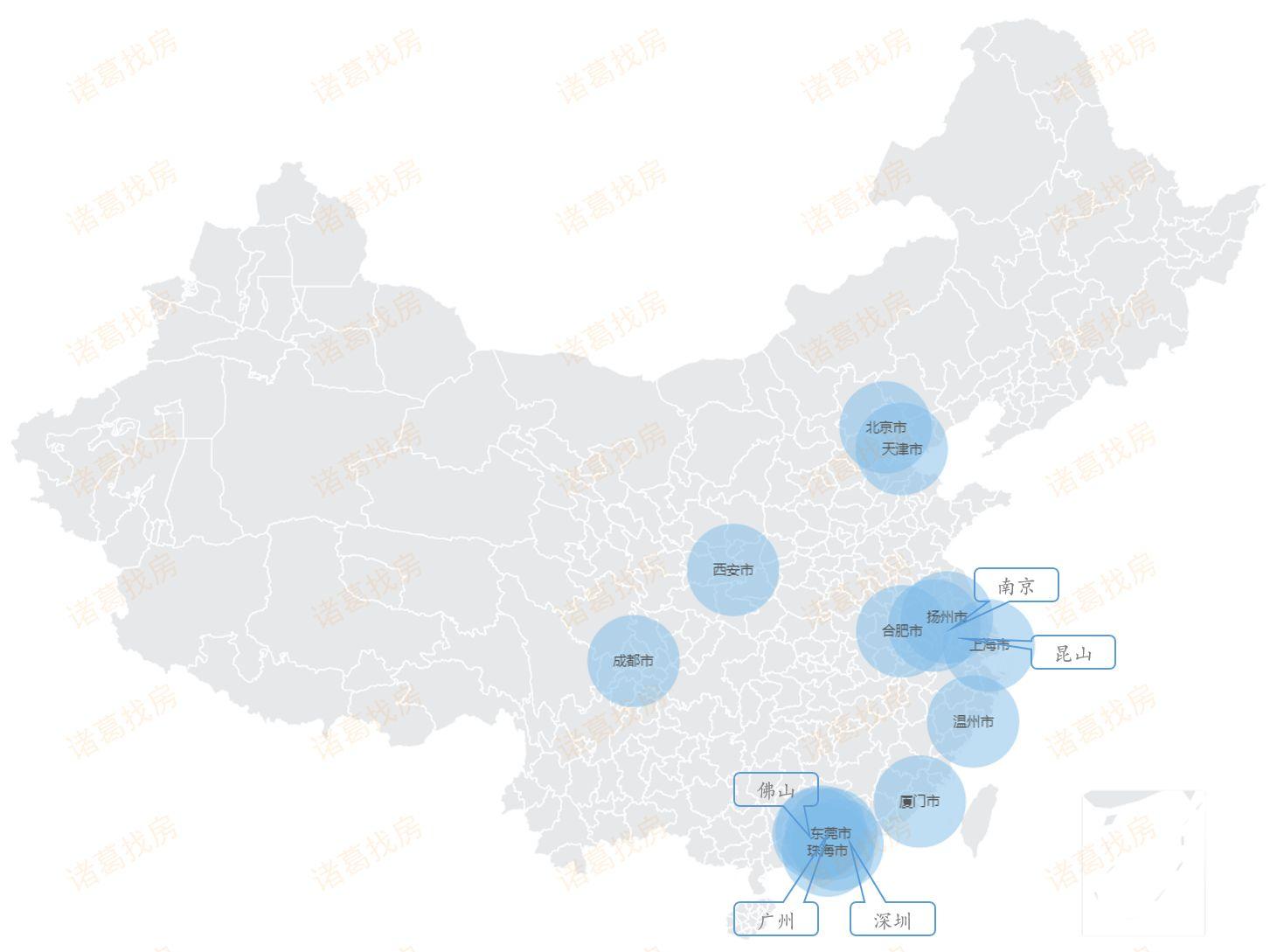

The Zhuge Finding Housing Data Research Center recently released a special study saying that the prohibition of “commercial reform and housing” policy to expand the city. Since Beijing issued a regulatory policy for commercial projects in March 2017, Shanghai, Guangzhou, Shenzhen, Chengdu First-tier cities such as Xiamen, Foshan and some hot-spot second-tier cities are close behind. In the future, the apartment market will still be mainly destocking. It is expected that the policy will not be released in the short term, and the policy may spread from first-tier and hot second-tier cities to other cities, and the apartment market will face a cooling crisis.

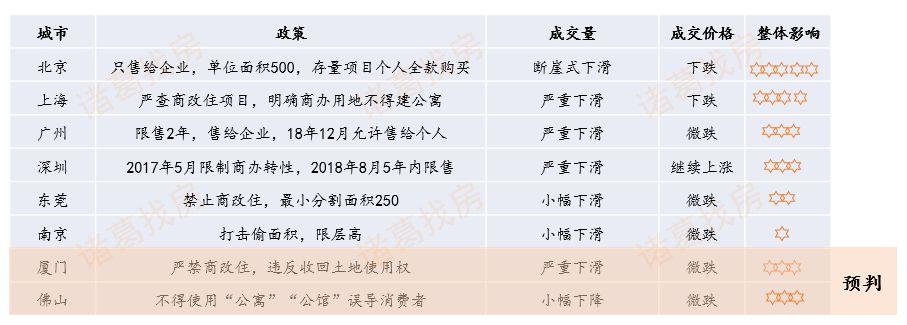

Research said that since Beijing introduced a regulatory policy for commercial projects in March 2017, first-tier cities such as Shanghai, Guangzhou, Shenzhen, and Chengdu and some hot-spot second-tier cities have followed closely, and in August 2019, Xiamen was introduced The strictest “prohibition of apartment” is strictly prohibited. Followed by November 15th, Foshan introduced a new policy prohibiting commercial transformation of apartments. From the perspective of comprehensive multi-regional control policies, it must not be changed into residential use without authorization, which has become a basic principle. Any real estate development company that violates the plan and changes commercial real estate projects to residential uses shall adopt a firm attitude of “once verification and serious handling”. Regarding “commercial reform and housing reform” and “commercial reform office”, the policy intensity of each city is different. The policy restricts the apartment to enter the market, and how to break the apartment market becomes a problem.

Distribution of major cities with commercial policies since 2017

Policy: The policy of prohibiting commercial reform and housing expansion will expand the city and tighten the trend in the future

According to the study, it can be seen from the urban distribution of the policies that the first-tier cities and hot-spot second-tier cities are the main ones, and the Yangtze River Delta and the Pearl River Delta regions are concentrated. The spillover of demand in the residential market caused the overheating of the apartment market and promoted the introduction of regulatory policies. The real estate market in first-tier cities and hot second-tier cities has developed rapidly and the regulatory policies are relatively strict, and investors are more optimistic.

A list of restrictions on business and housing reforms introduced by cities since 2017

The study pointed out that from the perspective of the policy, standardizing the commercial nature of prohibiting the conversion to residential use has become the basic condition of each city’s policy. In addition, Beijing has also stipulated that the minimum divided unit must not be less than 500 square meters and used Commercial projects must be sold in full payment and other items; Shenzhen, Chengdu and other places focus on product design management and control at the supply side; Beijing and Guangzhou stipulate that the purchased commercial properties cannot be transferred to individuals and can only be transferred to legal entities.

In addition, the study also suggested that Beijing, Guangzhou, Shanghai and other cities have introduced policies to encourage commercial reform of rents, providing another way out for commercial-use housing. Behind the introduction of the “commercial-to-rental” policy is the status quo of a large number of commercial-owned properties left idle in China’s first- and second-tier cities. Due to various reasons such as tightening of regulations, the backlog of commercial property is serious. For developers, the vacancy backlog of a large number of commercial-owned property listings is a huge waste of resources and also faces great sales pressure. Therefore, the “commercial-to-rental” implementation is in line with the market demand. However, in the final implementation process, many localities encountered many problems. The actual progress is not smooth at present, and the implementation policy needs to be further detailed.

Focus on apartment policy

Analysis of research indicates that the non-residential market will usher in major changes as the regulatory policies for apartments are successively introduced. There will be a clear difference between residential and apartment products. In the future, commercial plots must be sold as commercial plots. At the same time, the introduction of related policies is also a big negative for the commercial market. The office products themselves are difficult to decompose. In the future, commercial land cannot be used as apartment products, and the product value is suppressed. Commercial land and residential land prices have further spread. For home buyers, it is necessary to be more cautious to start with, and fine-decorated products such as high-rise apartments, such as edge cleaning products, due to unauthorized addition of floors, increase building area and other illegal activities, leading to certain risks; but also makes developers want to take advantage It’s getting harder to wipe the ball.

走势 Trends in various cities: policies affect market activity, volume generally declines

The study said that after the policy was introduced, it would have a more or less impact on the local commercial and residential apartment market. Six cities including Beijing, Shanghai, Guangzhou, Shenzhen, Nanjing, and Dongguan, which introduced a ban on commercial and residential changes in 2017, were selected. The volume and price changes of the apartment market before and after the policy in each city are used to judge the impact of the policy on the apartment market.

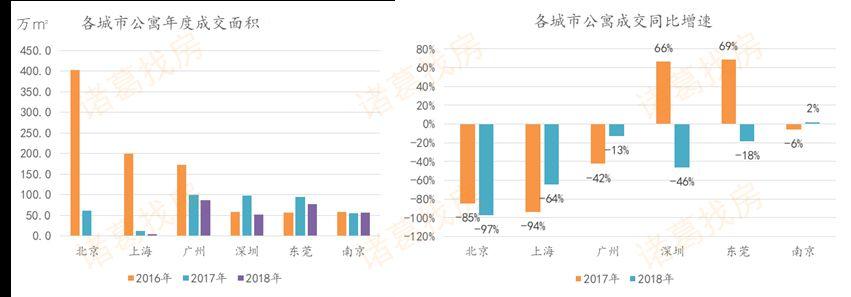

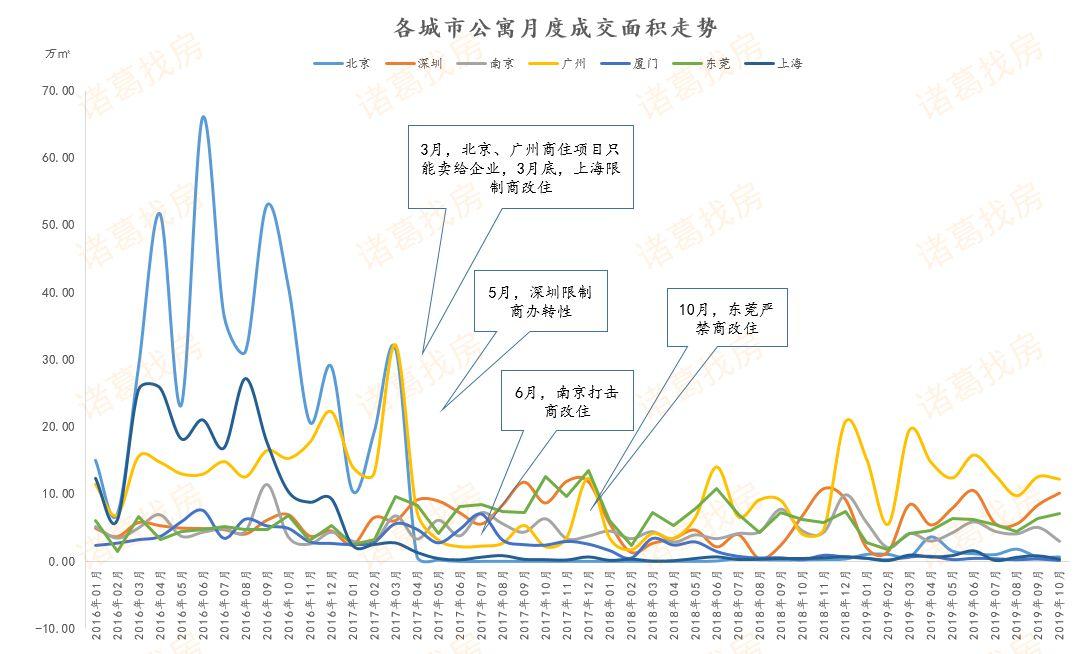

Volume: Different cities have different influences. Beijing and Shanghai have been fatally hit, followed by Guangzhou and Shenzhen. After Beijing and Shanghai introduced policies in March 2017, apartment transactions in 2017 and 2018 fell sharply. In terms of transaction area, Beijing and Shanghai fell by 85% and 97% year-on-year in 2017 and 2018. Shanghai dropped 94% and 64% respectively. From the monthly data, in the first month of the policy, that is, in April 2017, the transaction area of the Beijing and Shanghai apartment markets fell by a cliff, with chain declines of 97.4% and 51.1%, respectively, and the subsequent transactions were sluggish. Shanghai’s monthly transactions were less than 1 10,000 square meters, Beijing has no transactions for more than a month.

Guangzhou in March 2017 restricted commercial resale and stipulated that commercial resale can only be sold to enterprises. In the first month of the policy, the transaction area fell sharply to 73,700 square meters, a significant drop of 77.1% from the previous month. The whole year of 2017 decreased by 42% year-on-year. However, in December 2018, Guangzhou’s apartment policy no longer restricted sales targets. The sales area in December 2018 reached a new high since March 2017, and the decline for the whole year narrowed to only 13%.

Shenzhen in May 2017, although restrictions on commercial reforms were changed, the policy did not restrict purchasers. In addition, the residential housing market in Shenzhen was severely scarce and the apartment market was relatively strong. In the first month after the introduction, the policy effect was not obvious. Sales continued to rise, with a year-on-year growth rate of 66%. However, on the one hand, due to the impact of the policy, some buyers have doubts about the appreciation space of commercial and residential apartments. On the other hand, in 2018, the sales of commercial and residential apartments in Shenzhen were restricted for five years.

The impact of apartment policies in Nanjing and Dongguan is relatively mild. The transaction area has not changed much, especially in Nanjing. In 2017 and 2018, the transaction area of commercial and residential apartments fell by 6% and 2% year-on-year. Dongguan issued a policy in October 2017. In 2018, the transaction area of commercial and residential apartments fell by 18% year-on-year.

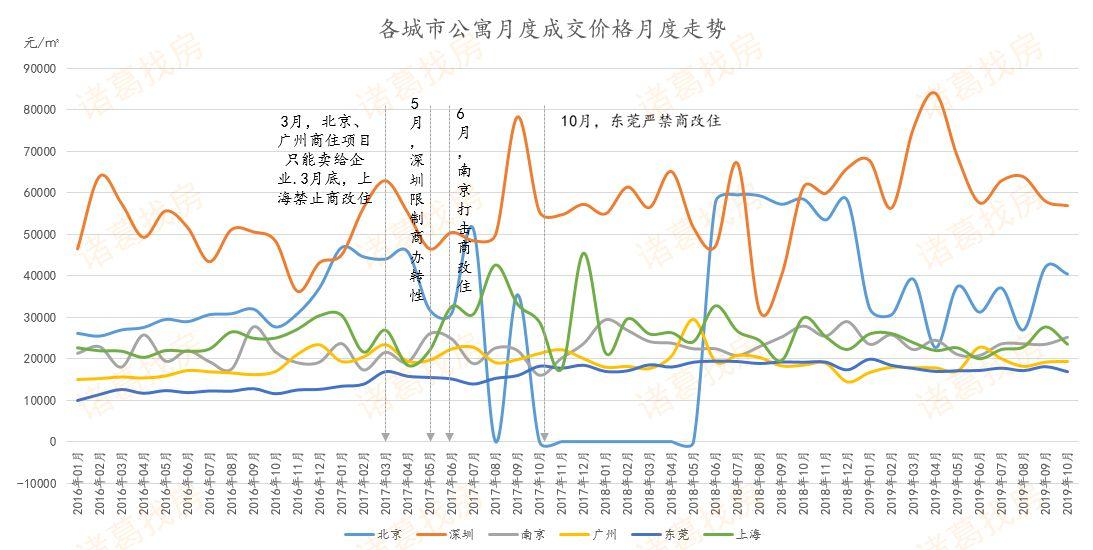

Transaction price: Price influence lags behind quantity. Except for Shenzhen, prices in other cities have fallen by different degrees. From the perspective of the transaction price trend, after the policy was introduced, the price was not motivated to rise. Except for the Shenzhen price trend, prices in other cities fell in different degrees. Among them, the price of Beijing fell the most. In the first ten months of 2019, the average transaction price of Beijing apartments was 34,013 yuan / ㎡, a decrease of 41.1% compared with 2018. Since 2017, the apartment market in Shanghai has vigorously inspected the residential redevelopment projects and carried out the rectification of “demolition of walls, demolition of gas, and removal of water and sewage” for “class housing”. After 2017, apartment prices in Shanghai showed a downward trend.

The average prices of Nanjing, Guangzhou, and Dongguan in the first ten months of 2019 decreased by 6.6%, 4.4%, and 4.4% respectively compared with 2018.

Due to the scarcity of new residential projects in Shenzhen, although the policy has squeezed some demand, prices are still relatively firm. In the first ten months of 2019, the average apartment price in Shenzhen was 65,196 yuan / ㎡, an increase of 18% compared with 2018.

Influence: Policy affects market activity, and volume generally declines. According to research and analysis, in summary, the prohibition on commercial-residence policies has affected the activity of the commercial and residential apartment market, and buyers and speculators are more cautious about starting commercial and residential apartments. Continued decline in volume will bring down prices. On the whole, Beijing and Shanghai were severely affected by the policy, which was a fatal blow to the apartment market, with both volume and price falling; again, Guangzhou. Nanjing and Dongguan were mildly affected, with volume and price falling slightly. Due to the particularity of its market, there is a serious shortage of commercial housing in Shenzhen, and the apartment market has high-end demand customers.Driven by households, the market still maintained an overall rise after the policy was introduced. But it is not meaningful for other cities.

Research and analysis indicates that among the cities that have recently introduced policies, Xiamen is expected to have a significant impact on the transaction volume of apartments due to stricter policies and violations of the right to recover land use rights without compensation. Foshan places restrictions on the planning and construction of commercial land projects. It is not allowed to build apartment products, not to sell such products during the sales process, not to mislead consumers, and to publicize the differences between commercial projects and residential projects to buyers. The projects to be run are commercial water and electricity, and supporting facilities must not be settled in school, etc., which is expected to have a greater impact on the market.

Influence ratings of commercial and residential apartment policies in various cities

Status and trend characteristics of commercial market in typical cities

Beijing: After the policy was introduced, both volume and price fell, and the commercial and residential apartment market was “slumped”, making life difficult.

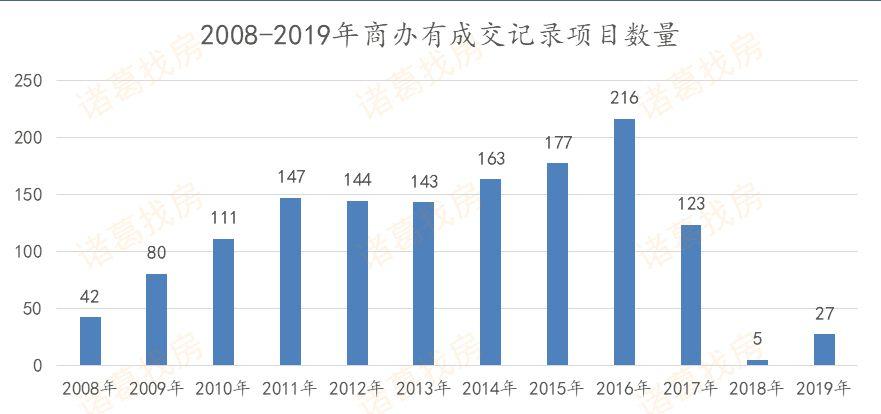

Supply and sales situation: The policy effect of 326 is significant, and the turnover has declined sharply. With the rise in residential prices, commercial and residential apartment products have gradually become substitutes for commercial housing due to the characteristics of low total prices and unlimited purchases. Since 2009, the transaction volume of commercial and residential apartments has gradually increased. By 2016, the transaction area of commercial and residential apartments reached its peak. The annual turnover was 4.029 million square meters, which was 2.8 times that of 2015. However, on March 26, 2017, the Commercial New Deal stipulated that projects under construction could not be sold to individuals. Existing projects must be eligible for residential purchase and paid in full. The policy impact was significant. After 2017, the transaction of commercial and residential apartments fell steeply. The once-hot fire is gone, and the market was even more indifferent in 2018, with only 18,000 square meters of transactions in the year. The transaction in 2019 was slightly better than that in 2018, but far lower than the level before the policy.

In terms of supply, after the introduction of the policy, on the one hand, developers are more cautious in entering commercial and residential projects on the market, and on the other hand, new land cannot be built into commercial and residential apartments, so supply is also very small. After March 2017, Beijing The supply of residential apartments increased by only 79,900 square meters, with a total of 647 units. Only a few of them were welcomed in November 2017 and June 2018. They are Tongzhou’s Hejing Center and Tongzhou’s Vanke Metropolis. With no supply in 2019, the apartment has entered the era of digesting existing projects.

Transaction price: After the policy, the price has dropped significantly, and it is still impossible to reverse the “priceless market” market. After the 326 policy, the prosperity of commercial and residential apartments is gone forever, market transactions are cold, and prices are not motivated to increase. According to the data, the average prices of commercial and residential apartments in 2017 and 2018 were 44675 yuan / m2 and 57863 yuan / m2, up 50.1% and 29.5% year-on-year. Low-quality commercial and residential projects are forced to delist, and even face large-scale check-outs. Some high-quality commercial and residential projects struggle to survive. In 2018, only 5 projects entered the market and were located in Tongzhou District. Therefore, the average commercial and residential prices in the city were raised . In 2019, after more than a year of policy digestion, some commercial and residential apartments tried to enter the market. However, due to transaction conditions, the transaction was not optimistic. Only price reductions could be used. The transaction price of commercial and residential apartments in 2019 was 30,900 yuan / ㎡. , A year-on-year decrease of 46.6%.

Inventory: As the transaction speed slows down, the de-chemicalization cycle is up to 117 months. In 2018, with the difficulty of deconstruction of apartments, there were no transactions for many months, and there was little supply. Only in June 2018, Vanke Metropolis entered the market. However, deconstruction is not optimistic. The inventory area increased compared to May, reaching 1.427 million square meters. MoM increased 3.6%. Subsequently, commercial and residential apartments entered a situation of continued low transactions, and inventory fell steadily. As of October 2019, the inventory area was 1.355 million square meters, a decrease of 4.3% year-on-year, and the elimination cycle was 116.9 months, a year-on-year decrease of 91.8%.

Project: After the 326 policy, there is no market price and no market, it is difficult to dissolve and the transaction is difficult to obtain. After 2008, residential prices climbed, and commercial and residential apartments with low total prices gradually became developers’ projects. The number of projects entering the market gradually increased and reached a peak in 2016. The year-round transaction covered 216 projects. There were 123 annual transactions, a decrease of 43% compared to 2016. In 2018, only 5 projects entered the market, and all of them were concentrated in Tongzhou District. In 2019, the number of projects entering the market increased. As of October 2019, the transactions covered a total of 27 projects. .

Nanjing: The policy influence is relatively mild, the market scale ceiling appears, and the price fluctuates slightly.

Supply and sales situation: The average monthly turnover for four consecutive years is about 40,000 cubic meters, and the market scale ceiling is gradually emerging. In March 2017, Nanjing introduced a policy that commercial buildings should not be designed in accordance with residential suites. As commercial housing is strictly controlled, the number of such products will be significantly reduced in the future, and there will be fewer and fewer apartment products on the Nanjing market. . After the introduction of the policy in March 2017, a small wave of transactions occurred, with a turnover of 67,000 square meters, an increase of 144.6% month-on-month. In the following months, the transaction volume remained high. In April, the apartment market added 212,100 square meters, an increase of 82.2% from the previous month. The reason is that after the policy controls commercial and residential apartment products, such products will become increasingly rare in the market, attracting a large number of investors. Since 2016, the average monthly transaction in the market has fluctuated around 40,000 square meters, and the ceiling of the market scale has gradually appeared. However, the surge in transaction volume after the policy is only a temporary phenomenon.

Transaction price: The price rose slightly in March 2017, with little price fluctuation. Judging from the average transaction price, the fluctuation range is not very large. The price rose slightly by 24.6% in March 2017. The average transaction price in May 2017 reached the highest value of 25931 yuan per year.㎡. Nanjing’s policy on apartments is relatively modest. The policy stipulates that the height of apartments should be limited from 4.8 meters to 3.6 meters. The main impact is to choose apartment products, and lofts such as loft have become out of print. On the premise that Nanjing already has a large number of small apartment products, the advantages of apartment products are not great.

Inventory: The overall inventory is large and the dechemicalization is slow. In October 2019, the dechemicalization cycle was 17 months. The overall inventory of the Nanjing apartment market is large, and the rate of desalination is slow. After the introduction of the commercial remediation policy in 2017, the market inventory and the elimination cycle have gradually increased. In September 2019, the inventory reached 796,100 square meters, and the elimination cycle reached 17.4 months. The purchase of apartment products in Nanjing is mainly for investment purposes, and the disadvantages of high loan and interest rate requirements and limited return on investment make it difficult to demolish apartments.

Guangzhou: After the 330 policy, the transaction volume fell sharply. After the 1219 policy control was loosened, it rebounded significantly.

Supply and sales situation: After the policy was introduced, the transaction quickly turned cold, but overall it was better than going north. The policy adjustment and relaxation eased the market to heat up. Due to factors such as residential purchase restrictions and investment demand, the Guangzhou apartment market has also risen. By March 2017, the supply was 298,100 square meters, and the transaction volume was 321,300 square meters, reaching the highest value in recent years. In order to regulate and regulate the apartment market, Guangzhou introduced a 330 regulation and control policy, which has a greater influence. It is clearly stipulated that the purchaser of a commercial apartment can only be a legal entity, and an individual cannot purchase an apartment. The promulgation of the policy caused the commercial and residential apartment market in Guangzhou to freeze into an instant, and the transaction volume showed a cliff-like decline. In December 2018, Guangzhou issued a notice notifying the “330 Policy” transaction of real estate projects. Commercial service properties are no longer limited to sales targets, and the sales area has clearly rebounded after adjustment and loosening, with a turnover of 206,500 square meters that month. Since December 18, Guangzhou apartment transaction volume has skyrocketed. Under the influence of policies and developers’ sprint performance at the end of the year, the transaction volume has remained high. In addition to the inertia of the online signing in February this year, The single-month transaction is basically above 100,000 square meters. The trading volume in 2019 gradually recovered to the level during the non-regulation period.

Transaction price: The price fluctuated slightly, showing a downward trend as a whole. In terms of transaction prices, the average apartment transaction price in 2017 was the highest in recent years. The introduction of apartment regulation policies in 2017 had a small impact on prices in the short term, and the prices fluctuated slightly. In April 2017, the price dropped to 19,415 yuan / ㎡. On the whole, the average price of the market transaction has been declining from the time of the policy’s introduction to October 2019.

Inventory: Inventory and dechemicalization cycles have risen significantly after the policy, and inventory has been steadily digested after the 1219 policy. The stock of apartments in Guangzhou is relatively large. Since the introduction of the 330 policy in 2017, the inventory has gradually increased. As of November 2018, the inventory reached 1.6 million square meters. The elimination cycle is nearly 29 months, and the elimination cycle is significantly longer. “121After the “Policy 9” was issued, the market responded positively, and apartment inventory was steadily digested. The dechemicalization cycle dropped significantly. In October 2019, the dechemicalization cycle dropped to 10.6 months.

Market prediction: Tightening policies are expected to continue to spread, and the apartment market is facing a cooling crisis

Research and analysis said that due to the restriction of residential purchase restrictions, apartment products have become a hot market due to unlimited purchases. Due to policy restrictions, buyers who do not have the qualification to purchase a house or lack of funds use the apartment as a transition product for a residential project, resulting in a sharp rise in apartment product transactions in recent years. In fact, there are great differences between apartments and residential products in terms of nature, supporting facilities, charging standards, taxes and fees. In recent years, problems caused by commercial reforms have emerged, mainly due to the basic supporting facilities such as commercial water, electricity and electricity for residential use after delivery, and the owner’s rights protection caused by failure to enjoy education and settlement facilities. The introduction of policies to regulate the market for commercial and residential apartments is a general trend.

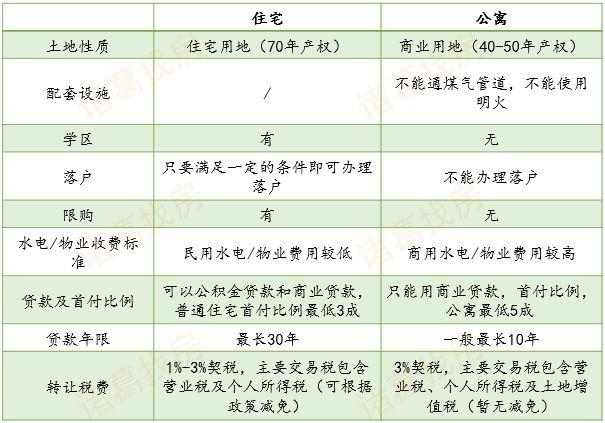

The difference between residential and apartment products

Since March 2017, first-tier cities and hot second-tier cities led by Beijing and Shanghai have successively introduced commercial-oriented policies to regulate the market. First, product-design, planning, and approval procedures for commercial-oriented projects have become more standardized, and policies have been introduced successively It can be seen that the local supply and transactions have declined in different degrees. Secondly, the impact of the policy is large, and the scope of the expansion of the city is wide. It is foreseeable that the policy regulation will last for a long time. The goal of the regulation is to crack down on commercial and residential apartment products and regulate the commercial market.

Research believes that, from the perspective of new supply in the apartment market, after the introduction of the new policies in various regions, many apartment projects to be launched for sale have been suspended and postponed, and rectification is underway according to the new policies. Real estate that had been sold before the new policy was introduced but still had a lot of goods in the future is also under policy digestion, and it is difficult to predict the situation of further sales. With the gradual strengthening of the policy, the actual number of projects entering the market will be greatly reduced, and the situation of depuration will not be optimistic. It is more likely that this state will continue to be maintained in the future.

From the perspective of the apartment market’s deactivation situation, urban projects with severe policy conditions face serious difficulties in dechemicalization. Overall transactions in cities that have introduced remediation policies have declined in different degrees. The owner of the apartment may be eager to sell off. As a result, many projects will gradually reduce the price and exchange the price.

The current commercial and residential apartment projects in the market are generally surplus. The strict specification of this product makes it impossible for developers to explore legal space for commercial and residential apartment products. Although some citiesThe city has introduced a policy to encourage commercial reform of rents, but the implementation process lacks supporting policies, and the overall implementation is not ideal. In the future, the apartment market will still be mainly destocking. In addition, the policy is not expected to be liberalized in the short term, and the policy may spread from first-tier and hot second-tier cities to other cities, and the apartment market will face a cooling crisis.