Wearables are becoming the “Red Sea” battlefield for the next giant to fight.

Editor’s note: This article comes from WeChat public account “Lan Xi” (ID: techread), author 丨 Lu Li.

Wearables are becoming the “Red Sea” battlefield for the next giant to fight.

First of all, it is inextricably linked to the hot trend of the smart phone market. At the beginning of November, the international data agency IDC released the global smartphone market data for the third quarter of 2019, which shows that the market share of the leading camps has further expanded-this quarter is composed of the top five camps composed of Samsung, Huawei, Apple, Xiaomi and OPPO. This represented a 71.3% market share for global smartphones, compared with 69% in the second quarter of this year.

Looking at the Chinese market, the stock market in the smart phone industry is inferior to the Red Sea competition. Similarly, according to IDC’s data report, Huawei, oppo, vivo, Xiaomi, and Apple’s leading camp has already occupied China this season. 94.9% market share.

Under such a background, a large number of players in the field of hardware technology have begun to look for new growth points. In addition to exerting strong demand for the smartphone industry such as 5G mobile phones, the horizontal expansion of business boundaries has become the focus of the former. An important direction is that wearables are one of the very typical areas.

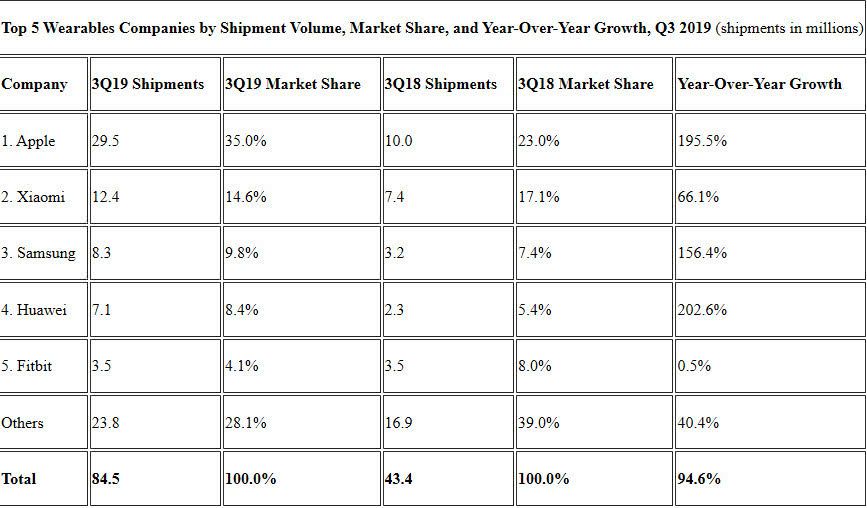

According to the latest data released by IDC, global shipments of wearable devices in Q3 2019 totaled 84.5 million units, a year-on-year increase of 94.6% . Apple, Xiaomi, Samsung, Huawei, and Fitbit occupy the top five, and this leading brand figure is exactly the same as last year, and even the rankings have hardly changed.

An obvious conclusion is that The Matthew effect in the field of wearables-the trend of getting stronger is becoming increasingly apparent.

The past of disorderly growth

The earliest wearable devices were born in the vast majority of peopleUnexpected scene-casino.

In 1961, MIT professor Edward Thorpe and Claude Shannon jointly designed a small wearable computer to study the application of the Kelly equation in roulette gambling. Computer rates during gambling, thereby verifying their formula is correct. In the 1980s and 1990s, the field of wearable devices began to accelerate, and many categories were born during this period.

In 1981, “Father of Wearable Technology” Steve Mann designed the first head-mounted camera in history; in 1984, Casio launched the world’s first digital watch Casio Databank CD-40 capable of storing information; In 1989, Reflection Technolog introduced the Private Eye head-mounted display; in 1994, researchers at the University of Toronto developed a wrist computer that could hold the keyboard and display on the forearm.

Limited by bottlenecks such as technology, cost, application scenarios, and supporting facilities, these new products have not been able to form a consumer-grade market, benefiting the general public. Take the Private Eye display as an example, this product is like a headset, equipped with a 1.25-inch 720 * 280 pixel monochrome screen, which can achieve the viewing effect of about 15-inch display. In addition to being able to read the text of the document, this wearable device basically has no other functions, and its portability is not satisfactory.

The smart watch category is even more so, The first smartwatch MSN Direct launched by Microsoft in 2004 opened the curtain of the second screen technology, but it can only provide news, weather, text messages and other information content receiving functions-even users need to pay monthly or annual Usage fee-but cannot connect to the phone to receive notifications and messages. Of course, although these very early wearable devices were quickly eliminated, they have formed the prototype of the wearable field, and their avant-garde design philosophy has also affected some products later.

Along with the history of the digital technology revolution, it is not a long history. One accepted rule is that once there are enough developers involved, a mature market can be formed. Once the market becomes saturated, developers will start to try to bring differentiation to their products, which will trigger the trend of vertical segmentation in the field.

After entering the 21st century, with the significant progress of software and hardware technology, the above bottlenecks have been gradually broken, and a series of truly intelligent wearable devicesBegan to enter the vision and life of ordinary people. Among them, Fitbit launched the industry’s first fitness equipment that can be clipped on clothes in 2008 to track and record the user’s steps, walking distance, calorie consumption, exercise intensity and sleep status. For example, in 2012, many foreign hardware companies, including Sony and pebble, launched smart watch products.

In the domestic wearable device field, It has entered an explosive development stage since 2015. According to the “Wearable Device Research Report” released by the China Academy of Information and Communications Technology that year, the size of China’s smart wearable device market was 12.58 billion yuan in 2015, with a growth rate of 471.8%. Behind this, Apple officially launched the Apple Watch this year. Relying on Apple ’s complete application ecosystem, the number of applications on the Apple Watch has also increased rapidly since its release. This year, the product achieved sales in the Chinese market. 1 million units.

In the domestic wearable device field, It has entered an explosive development stage since 2015. According to the “Wearable Device Research Report” released by the China Academy of Information and Communications Technology that year, the size of China’s smart wearable device market was 12.58 billion yuan in 2015, with a growth rate of 471.8%. Behind this, Apple officially launched the Apple Watch this year. Relying on Apple ’s complete application ecosystem, the number of applications on the Apple Watch has also increased rapidly since its release. This year, the product achieved sales in the Chinese market. 1 million units.  Huawei, Xiaomi, ZTE, Shanda, Baidu and other domestic companies have successively released Smart bracelet, smart watch, smart glasses and other products. Among them, Xiaomi Bracelet became the product with the highest sales volume in the Chinese smart wearable device market at that time by breaking the tens of millions of sales with its low price and strong online marketing capabilities. A series of children’s watch brands represented by 360 are also emerging in market segments.

Huawei, Xiaomi, ZTE, Shanda, Baidu and other domestic companies have successively released Smart bracelet, smart watch, smart glasses and other products. Among them, Xiaomi Bracelet became the product with the highest sales volume in the Chinese smart wearable device market at that time by breaking the tens of millions of sales with its low price and strong online marketing capabilities. A series of children’s watch brands represented by 360 are also emerging in market segments.

From disorderly growth to blossoming flowers is a historical process of wearable devices.

Watches, bracelets, TWS headphones, the three kingdoms stand up

Today, from the perspective of category distribution, the domestic wearable device market has been dominated by smart watches, smart bracelets and TWS headsets, which together account for more than 95% of the market share in this field. Let’s take a look at the “now” of these three wearable device categories.

Smartwatches: According to the statistics of the China Business Industry Research Institute, the total sales of China’s smartwatches (excluding children’s smartwatches) in 2018 were about 2.05 million , A year-on-year increase of 63%, and more than 500 smartwatch brands. It is expected that the Chinese smartwatch market will maintain a 55% growth rate in 2019, with a total sales volume of 3.2 million units, and a compound growth rate in the next three years will remain above 50% . This statistic also points out that in 2018, six smart watch manufacturers including Huawei, Apple, Huami, Honor, Ticwatch, and Jiaming occupied more than 60% of the Chinese market share.

From a global perspective, according to research firm Trendforce, global smart watch shipments in 2019 will reach 62.63 million units, compared with 44 million units in 2018, which will continue to grow significantly, while also forecasting global growth in 2022. Smart watch shipments will exceed 100 million for the first time, reaching 113 million.

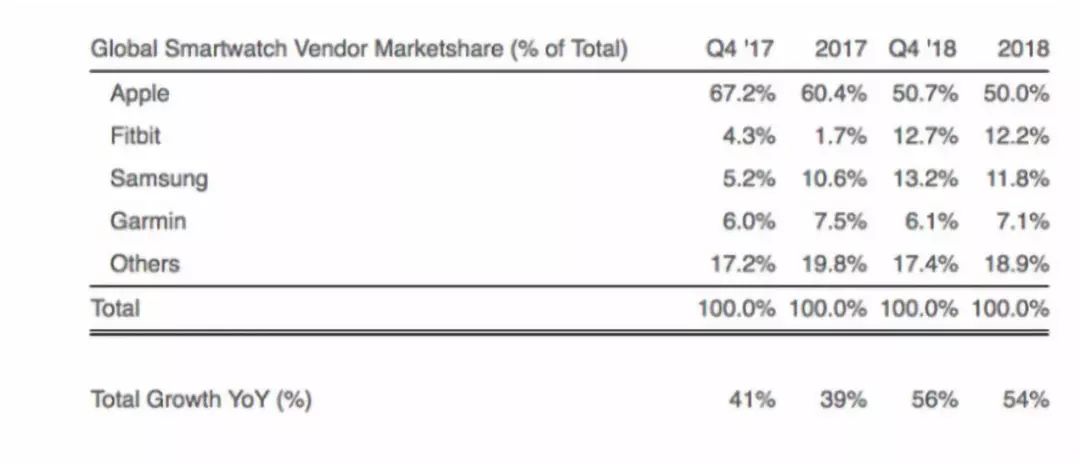

Among them, Apple is a well-deserved leader in this field. Three of the TOP 5 smart watch product sales in 2018 by Counterpoint Research are Apple Watches. Its leading position is also becoming increasingly stable. In the research report released by Strategy Analytics, the global market share of Apple Watch has increased from 45% in the third quarter of 2018 to 48% in the third quarter of 2019.

Samsung ’s global shipments of smart watches in Q3 2019 were 1.9 million, almost doubling from 1.1 million in the same period last year. Its market share has also jumped from 11% to 13% in Q3 2019, and the position of the second top spot has been continuously consolidated. Domestic brands in this field that currently stand the battle are Huami’s Amazfit and Huawei. Also according to Counterpoint’s data report, Amazfit has entered the global smartwatch shipments in the first quarter of this year Volume TOP 5 and China’s TOP 2 ranks, the latter is behind Amazfit.  The smartwatches today are at the product level and smart Some mobile phones are similar, such as video chat, mobile payment, sending and receiving text messages, and information inquiry.

The smartwatches today are at the product level and smart Some mobile phones are similar, such as video chat, mobile payment, sending and receiving text messages, and information inquiry.

However, aside from the characteristics of the smart watch itself that can be combined with the field of fashion consumer goods, the tiny screen of the smart watch makes it difficult to provide users with the same as a real smart phone.The intelligent age will eventually be the next foreseeable future of human society. Wearable devices and the software, applications and content services behind them are likely to become an inseparable part of everyone’s daily work. This determines this. The future of the field is bound to be a battleground for tech giants.

In the domestic wearable device field, It has entered an explosive development stage since 2015. According to the “Wearable Device Research Report” released by the China Academy of Information and Communications Technology that year, the size of China’s smart wearable device market was 12.58 billion yuan in 2015, with a growth rate of 471.8%. Behind this, Apple officially launched the Apple Watch this year. Relying on Apple ’s complete application ecosystem, the number of applications on the Apple Watch has also increased rapidly since its release. This year, the product achieved sales in the Chinese market. 1 million units. Huawei, Xiaomi, ZTE, Shanda, Baidu and other domestic companies have successively released Smart bracelet, smart watch, smart glasses and other products. Among them, Xiaomi Bracelet became the product with the highest sales volume in the Chinese smart wearable device market at that time by breaking the tens of millions of sales with its low price and strong online marketing capabilities. A series of children’s watch brands represented by 360 are also emerging in market segments. Today, from the perspective of category distribution, the domestic wearable device market has been dominated by smart watches, smart bracelets and TWS headsets, which together account for more than 95% of the market share in this field. Let’s take a look at the “now” of these three wearable device categories.

Smartwatches: According to the statistics of the China Business Industry Research Institute, the total sales of China’s smartwatches (excluding children’s smartwatches) in 2018 were about 2.05 million , A year-on-year increase of 63%, and more than 500 smartwatch brands. It is expected that the Chinese smartwatch market will maintain a 55% growth rate in 2019, with a total sales volume of 3.2 million units, and a compound growth rate in the next three years will remain above 50% . This statistic also points out that in 2018, six smart watch manufacturers including Huawei, Apple, Huami, Honor, Ticwatch, and Jiaming occupied more than 60% of the Chinese market share. From a global perspective, according to research firm Trendforce, global smart watch shipments in 2019 will reach 62.63 million units, compared with 44 million units in 2018, which will continue to grow significantly, while also forecasting global growth in 2022. Smart watch shipments will exceed 100 million for the first time, reaching 113 million. Among them, Apple is a well-deserved leader in this field. Three of the TOP 5 smart watch product sales in 2018 by Counterpoint Research are Apple Watches. Its leading position is also becoming increasingly stable. In the research report released by Strategy Analytics, the global market share of Apple Watch has increased from 45% in the third quarter of 2018 to 48% in the third quarter of 2019. Samsung ’s global shipments of smart watches in Q3 2019 were 1.9 million, almost doubling from 1.1 million in the same period last year. Its market share has also jumped from 11% to 13% in Q3 2019, and the position of the second top spot has been continuously consolidated. Domestic brands in this field that currently stand the battle are Huami’s Amazfit and Huawei. Also according to Counterpoint’s data report, Amazfit has entered the global smartwatch shipments in the first quarter of this year Volume TOP 5 and China’s TOP 2 ranks, the latter is behind Amazfit. However, aside from the characteristics of the smart watch itself that can be combined with the field of fashion consumer goods, the tiny screen of the smart watch makes it difficult to provide users with the same as a real smart phone.The intelligent age will eventually be the next foreseeable future of human society. Wearable devices and the software, applications and content services behind them are likely to become an inseparable part of everyone’s daily work. This determines this. The future of the field is bound to be a battleground for tech giants.