How much savings do I need to save before retirement? Can saving money alone achieve financial freedom for the elderly? Or do we need to carry out asset planning as early and reasonably as possible to avoid becoming a reserve for “bankruptcy”?

This article is from WeChat public account “AgeClub” (ID: AgeClub), the original title “Heavy Release: 2020 China Banking Industry Senior Finance Innovation Trend Report Series-Banking Clients Aging, Opening the Second Life 》

The aging of China is accelerating. Starting from 2021, the average annual growth rate of the elderly population will increase from the current average of 10 million to 20 million. The large-scale middle-aged and elderly groups have begun to deeply affect Chinese business. The development and change trend of all walks of life in society;

We have previously analyzed the trend of passive aging of offline commercial department stores. In this report, we will focus on the development and innovation opportunities of comprehensive aging of banking customers.

This report is produced by AgeClub’s New Senior Business Research Institute. It combines the research and analysis data of the NewAgingPro insight team of independent consulting brand owned by AgeClub. Innovation Trend Report 2020: Starting a Wonderful Second Life;

This article is an excerpt from part of the report. Here are some exciting points:

-

AgeClub’s offline survey found that the elderly have gradually changed their financial management from “I don’t understand, I try not to touch” to “I know something, I am willing to buy products that suit me”, especially the new elderly in first-tier cities. Compared with the second- and third-tier cities, it shows diversity and accepts risks more than other cities;

-

At present, most domestic banks’ products and services for elderly users are still at a relatively early stage. A few banks have realized the importance of middle-aged and elderly customers, gradually penetrated into the middle-aged and elderly group from all angles, and vigorously Development of pension finance: Only two years after Industrial Bank launched the pension finance business “Life in Life”, VIP customers have exceeded 1 million and trust assets have exceeded 510 billion yuan; CITIC Bank’s elderly customers reached 12.64 million at the end of October 2019, and managed assets Reached 1.04 trillion yuan;

-

Alipay, which has a large number of young and middle-aged users, has also joined the old-age finance camp. It has built-in old-age money management modules in its wealth management services, and there are also old-age money management programs produced by other financial institutions, which can be seen from its user reviews. Pension financial products attract attention and need professional answers;

-

The Japanese banking industry adheres to the positive concept of “retirement is the starting point of a wonderful second life”, and plans financial solutions after retirement based on the user’s family structure, career, and future life vision, and targets dementia.Patients with financial management carried out meticulous product design.

“The Bankruptcy of the Old Age: A Nightmare named” Longevity “” is a full record of the interview process of the recording group of the NHK special program. This show reveals some of the property problems encountered by the Old Age. Medical, interpersonal, and other influences.

For example, the owner of a construction company lost her dependence after the death of her only son and husband. In order to save money, she would not dare to see a doctor if she was ill …

The pet shop owner closed the shop and concentrated on caring for the seriously ill mother. After sending the mother away, he was unable to re-employ. He had to sell the house where he lived with his mother to make a living …

Elderly people living on pensions simply go bankrupt because of illness and injury and can no longer live on their own income. Such cases are constantly happening.

Once you reach old age, these situations can happen to anyone. Especially the elderly living alone, without family care, medical and nursing expenses will become a heavy burden.

In the previous article, we made a detailed analysis of the consumption of different categories, scenes and channels of middle-aged and elderly people, and how much savings do you need to save before retiring? Can saving money alone achieve financial freedom for the elderly? Or do we need to carry out asset planning as early and reasonably as possible to avoid becoming a reserve for “bankruptcy”?

I. After the upgrade of new elderly consumption, the concept of financial management will also keep up

1.1 Consumption upgrade, where does the money come from?

According to data disclosed by the National Bureau of Statistics, China ’s annual per capita consumption expenditure in 2018 was 19853 yuan, and the annual per capita consumption of urban residents was 26112 yuan, and it was growing at an annual growth rate of 7.5%.

If you live in an urban area, your life expectancy is 80 years. After you retire at 60, the total consumption expenditure in 20 years is about 1.24 million yuan.

After the children of middle-aged and elderly groups grow up and become married, family and work have less and less restraint on them, and they will have more time and energy to arrange their own lives and satisfy all aspects of hobbies.

Although many seniors have changed their consumption concepts, they are willing to spend money on themselves, and their health promotion, social entertainment, hobbies, and online consumption all highlight their awareness and behavior of consumption upgrade. The consumer sector has become wider, and consequently consumer spending has also increased.

Most of these hobbies require a certain amount of financial support, but the space for the elderly’s economic income to grow significantlyIt’s not big anymore.

More and more silver-haired people use modest consumption to add color to their later life. The consumption has been upgraded. Where does the money come from?

First is the savings that were saved when they were young. For them, the accumulated wealth is the guarantee of future life. Middle-aged and elderly people basically have a certain wealth accumulation before retirement, but how to take care of this money is the pain point of most middle-aged and elderly people.

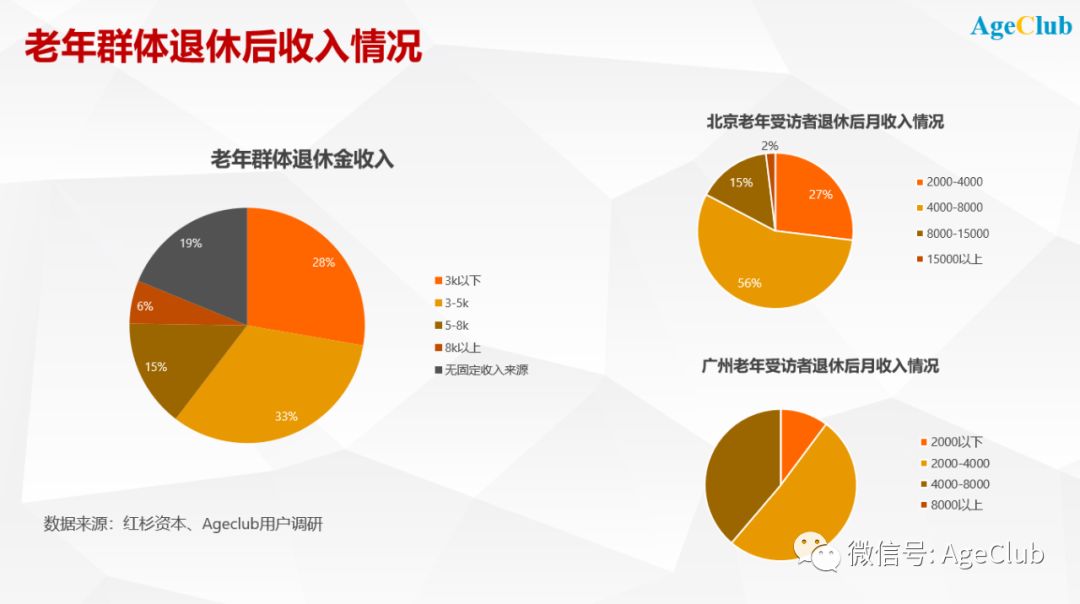

Second is retirement benefits. According to the 2017 White Paper on the Consumption Habits of the Elderly in China, 88% of the elderly in China have endowment insurance. According to Sequoia’s 2019 survey data, 61% of the respondents have a monthly pension of less than 5,000 yuan.

According to data from our user surveys, first-tier cities such as Beijing and Guangzhou have the highest monthly income after retirement of less than 8000.

Finally, financial management income. At present, most middle-aged and elderly people are more conservative in financial management concepts. In addition to income, principal security is still the most important factor for them to purchase financial management products.

In this case, their first choice is time deposits. Many people are basically confused about how to invest and what to invest, and they dare not make jokes about their savings for many years.

According to the results of our offline survey of the first-tier and new-tier cities’ elderly groups, we find that current financial management and asset allocation still prefer stable financial products (represented by regular savings and bank financial products).

But with the gradual improvement of the related quality of the elderly, it has shown diversity compared to second- and third-tier cities, and its risk acceptance (in terms of stock speculation, property speculation, foreign currency speculation, etc.) is higher than other cities.

1.2 By age, what do they need?

We summarize its asset management needs based on the asset status, consumption characteristics, and risk tolerance of each life cycle:

-

The customer base of the youth stage has less savings in itself, and the life pressure is less biased towards savings, high-risk investment and financial products for housing loans;

-

The middle-aged customer base has accumulated a certain amount of wealth, but the family burden is more inclined to invest steadily, and a small amount of funds will be allocated for insurance or high-yield investment;

-

At this stage, the dynamic elderly group aged 50-70 is in a state of retirement / immediate retirement. Their income is mainly pension and pension insurance, and they tend to financial products such as medical insurance and related pension plans; p>

-

The proportion of senior citizens above 70 in health care expenditure is gradually increasing, with zero or less risk and investment tools with stable returns, and the liquidity of wealth management funds has higher requirements.

For most of the elderly, although they have some savings, their income is gradually decreasing, and high expenditures on medical care are gradually increasing. At present, most elderly people are in urgent need of financial services and products for the elderly.

1.3 What do they need for groups with different assets?

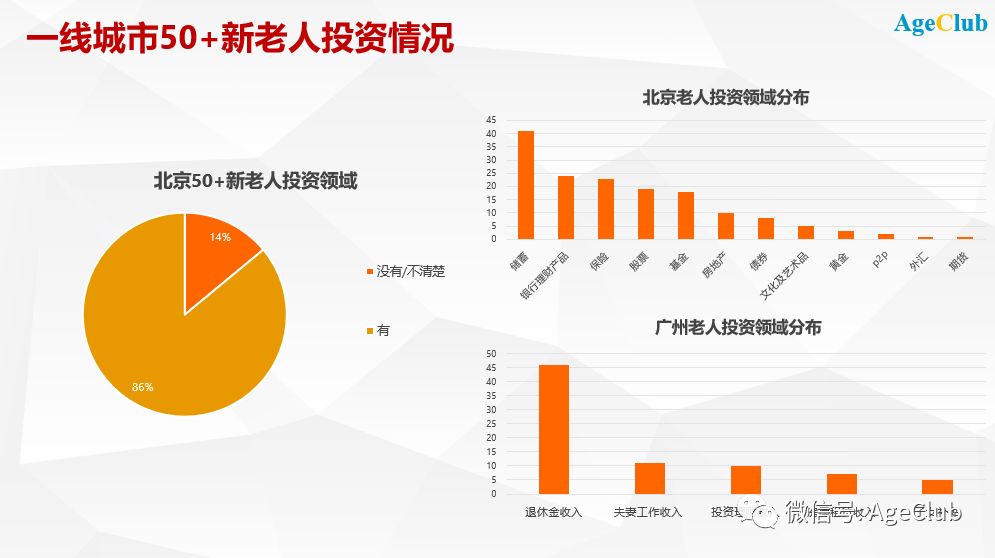

According to Ageclub’s survey of first-line new seniors, it can be seen that 100% of respondents have a stable cash flow income after retirement, and 86% of new seniors will invest.

Among the elderly groups interviewed, those with assets below 100,000 have to pay their daily expenses and actively subsidize their children’s juniors. They have hardly bought any pension products; those with assets between 1 million and 10 million , Spending more on tourism, medical examinations and health products, cultural and entertainment products; groups with assets of 10 million or more prefer pension real estate.

Elderly people with different assets have different choices of financial products:

-

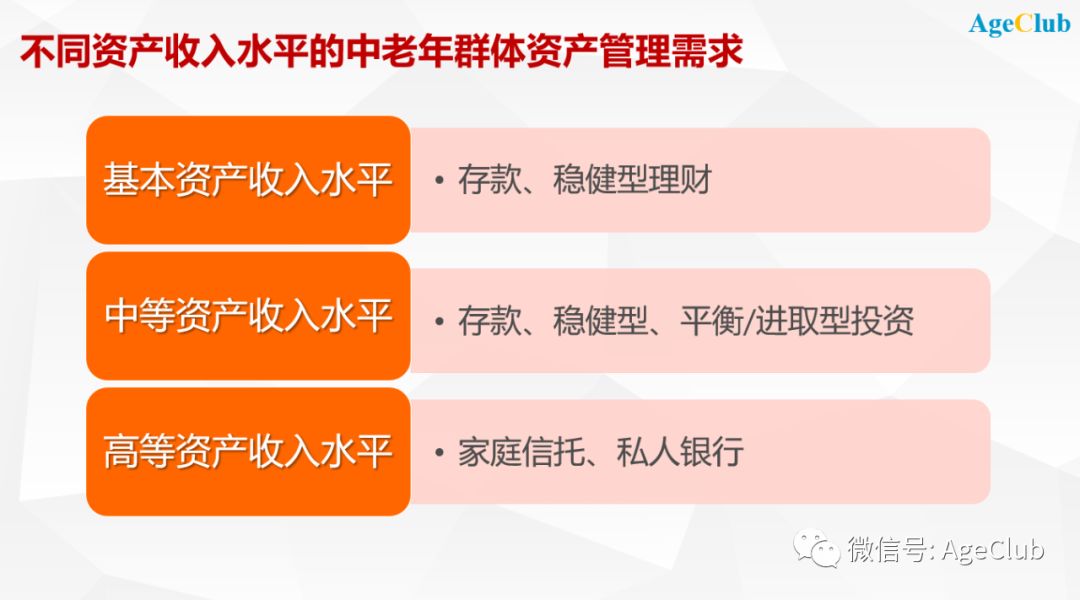

Elderly people with basic income levels generally choose deposits and stable financial management to maintain the stability of their assets;

-

Middle-income seniors can basically meet their daily expenses becauseAs their consumption in entertainment and consumption gradually increases, there is also a part of their spare money. For them, on the basis of deposits and stable financial management, add some high-yield financial products;

-

For the elderly with higher income level, they have enough funds to spend and support them to make various investments. For them, choosing private banking and family trust is a relatively easy and guaranteed choice.

Second, the design of domestic banks’ pension services and products is still in its infancy.

As the family income and consumption situation gradually stabilizes, the financial needs brought about by the aging of the population will gradually ferment, and the middle-aged and elderly groups have a certain amount of savings for asset investment management, becoming a large number of new forces.

Under this situation, many banks have launched endowment finance, and have continuously introduced financial products and services for middle-aged and elderly customers.

We conduct a summary analysis of pension financial products and related services launched by domestic listed banks, categorizing these products and services according to the bank’s launch time and the degree of meeting customer demand for property management, organized as follows:

2.1 After the concept of pension finance for the elderly has gradually become hotter, various banks have taken the lead to issue pension wealth management products, and we have sorted and classified the exclusive services provided by banks for senior customers.

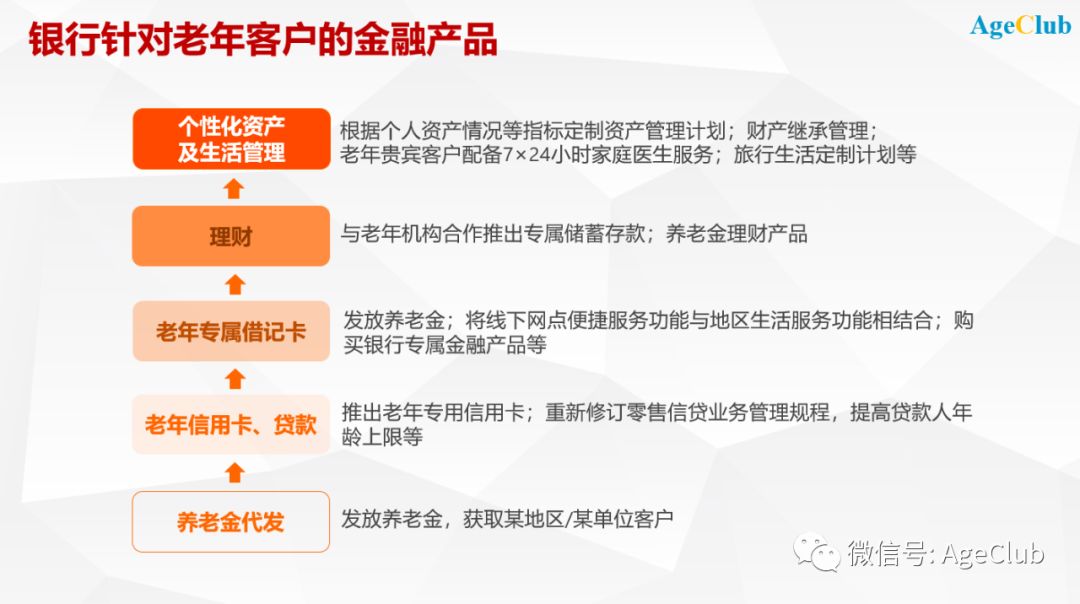

2.2 Pension payment

Pensions are the main source of income for the elderly, and most banks have pension distribution services.

The generation of pensions can increase the number of effective customers in sub-branches. Banks act as agents to pay wages and pensions to individuals. Based on the information provided by the enterprise, the bank issues it to the bank account of each worker and retiree through a specially developed wage generation transaction.

Elderly people prefer small gifts. On the basis of providing pensions, they use daily necessities such as rice and oil as gifts to stimulate elderly customers to deposit.

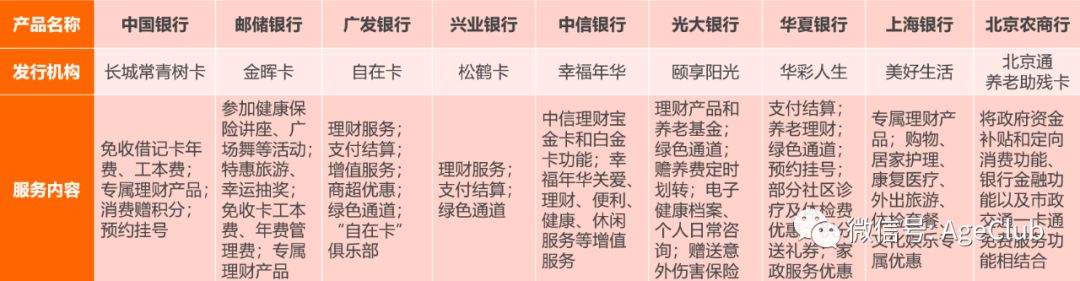

2.3 Debit card for seniors

Not only that, some banks tailor-made exclusive debit cards for middle-aged and elderly customers, and through the issuance of bank cards, they provide exclusive discounts on financial investment and living expenses for the elderly.

For example, Guangfa Bank launched the “Free Card” for middle-aged and older customers over 50 years old, which includes exclusive financial management, payment settlement, value-added services, business discounts and other services; CITIC Bank also launched the “Happy Years Card”, targeted at middle-aged and elderly people. The immediate needs of the group and the characteristics of investment and financial management, issuing gold and platinum cards …

Bank card segmentation appeared earlier, but because of the limited ability of old people to accept new things, the traditional concept of using cash for consumption has reduced the significance of using bank cards in this group of people.

The elderly card now launched is slightly different from the basic bank card functions such as fee-free, SMS reminder, and cost-free fee. On this basis, entertainment and health care related to middle-aged and elderly people are added.

2.4 Exclusive wealth management products for the elderly

Based on bank cards, major commercial banks take full advantage of their wealth management product platform to launch wealth management products designed to meet the investment needs of the elderly.

This kind of wealth management products are generally low and medium-level risks, with higher interest rates than ordinary time deposits, and use segmented interest rate calculations. Products can be purchased and redeemed at any time, which meets the elderly’s appreciation and liquidity of funds. Demand.

For example, Minsheng Bank launched a starting point of 50,000 yuan “Dinghuobao” with an annualized rate of return higher than the five-year time deposit rate; SPD Bank launched “Enjoy Win” to meet the elderly’s preference for safe deposit; Banks launch reassurance deposits for senior customers, with half-year or one-year yields of 4% …

In addition to single-type products, some banks further subdivide the financial needs of elderly customers, according to the elderly

People with different risk tolerance have designed different types of risk-reward wealth management product packages.

For example, the Bank of Shanghai launched a wealth management package that includes “Hua Cai Life” which bears a lot of risks and benefits; investment tends to be conservative; “Easy life”.

2.5 Senior credit cards / loans

Most elderly people lack stable income, face health risks, and have relatively weak repayment capabilities. Therefore, most banks generally limit applicants’ age plus repayment period to 65 years of age due to concerns about the risk of bad debts.

Hengfeng Bank revised the retail credit industry in 2015The management regulations limit the age of the borrower to 70 years old; subsequently, ICBC also extended the maximum age of the individual housing loan borrower to 70 years old, and the sum of the age of the borrower and the loan term does not exceed 75 years.

In addition to opening loans, some banks have also opened up special credit cards for the elderly. For example, CITIC Bank is the first in China to launch the “Ruyi Card”, an exclusive credit card for the elderly whose applicant age has increased to 70.

The business brought by credit card consumption, overdrafts, transactions, etc., is not the whole reason for CITIC Bank to launch the “Silver Hair”, but to use credit cards as a bridge to preempt, including pension, wealth management, health, wealth inheritance, etc. Of the entire elderly financial market.

2.6 Personalized assets and life management

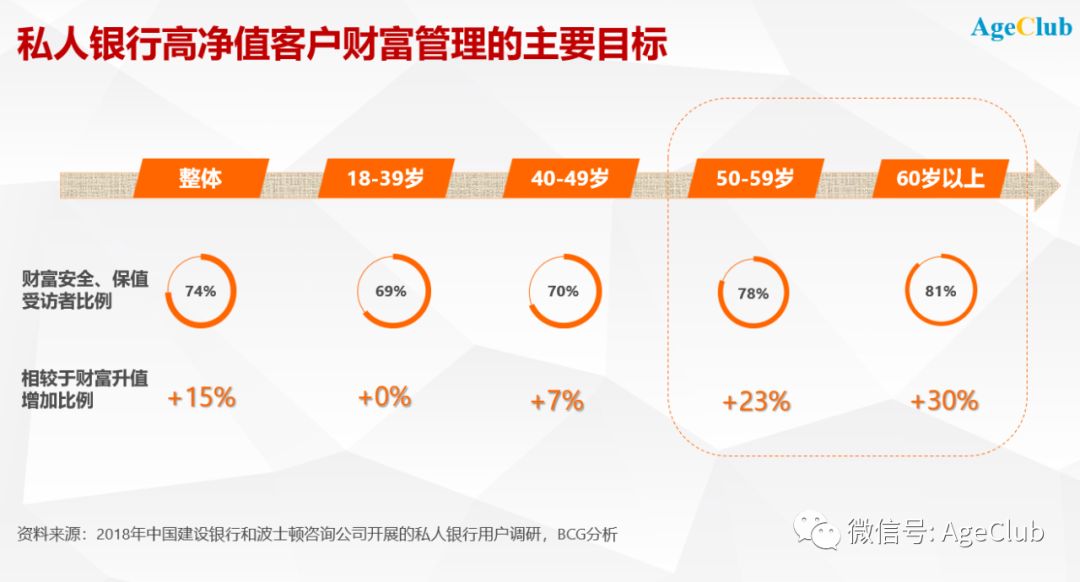

According to the “China Private Bank 2019” report issued by CCB and the Boston Consulting Group, the primary financial goals of high-net-worth individuals in private banks have shifted to the safety and preservation of wealth, and 50 years of age is a watershed in the transformation of financial goals.

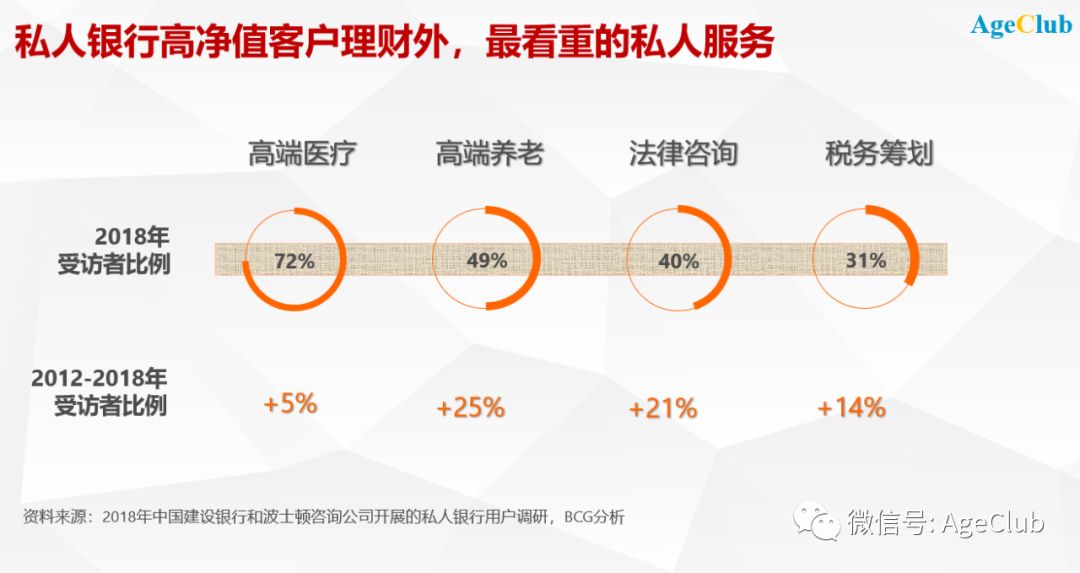

For high-net-worth clients, in addition to the appreciation of their wealth, the most valued private services are high-end medical care and high-end pensions, and the demand for high-end pensions has grown faster than before.

Aiming at the high-net-worth middle-aged and elderly people, CCB also launched a retirement planning service “Happy Old Age” for its senior citizens. Its services are in addition to the regular private bank VIP services such as private doctors, VIP experiences, and VIP medical treatments. Banks that include pension planning services in their main services.

This service will be based on the customer’s pension demand goals and current financial situation, based on the family assets, liabilities, and income provided by the customerExpenditure and future cash flow, etc., to predict the supply of pensions for customers, to provide them with investment planning and consulting, various insurance planning and consulting, and wealth inheritance and consulting.

In addition to wealth management services and consultancy services, it will also provide clients with exclusive value-added services such as medical and health care, home care, and social interaction.

CITIC Bank accounts for less than 13% of senior customers over the age of 50, but their contributions to asset management, savings deposits, VIP customers, and private banking all exceed 50%.

The related business of senior customers of its private banks mainly has the characteristics of “heritage” and “club”. CITIC Bank relies on the strong brand and comprehensive strength of CITIC Group to integrate the internal and external quality resources of the group to provide professional services for high net worth private banking customers And comprehensive family trust solutions and supporting services.

It will also create five major clubs for investors, health and wellness, future leaders, happy living, and travellers for private banking clients. From the financial and non-financial dimensions, through expert consultation, value-added services and market activities, for private banks. Customers build differentiated service platforms.

In addition to providing comprehensive high-end medical services, the health and wellness club extends the upstream and downstream services of the health industry such as fitness, sports, and maintenance, covering various states such as health, sub-health, disease, and surgery. Highlights include global physical examination and medical treatment channels, and the industry’s first one-to-one normalized consultation and diagnosis of experts, providing customers with periodic expert diagnosis and treatment services.

The Travel Furniture Club will combine high-end customers’ attention to travel, integrate travel resources, and create leisure activities and services that are close to nature and unique personality. At the same time, the theme of photography and travel are combined to create a “CITIC Bank Love Photography Alliance” and organize related photo exhibitions and photo contests.

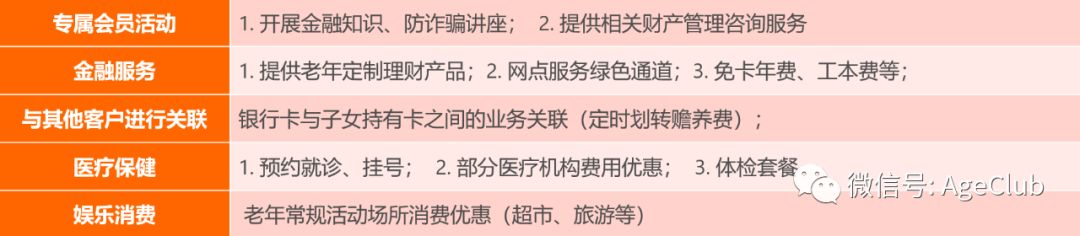

2.7 Additional services for senior customers

In addition to setting related financial products, each bank will upgrade the financial management scenes of senior customers appropriately, extend from the offline scenes that are familiar and loved by senior customers to online, and finally combine online and offline to form a service closed loop Convenient for older customers.

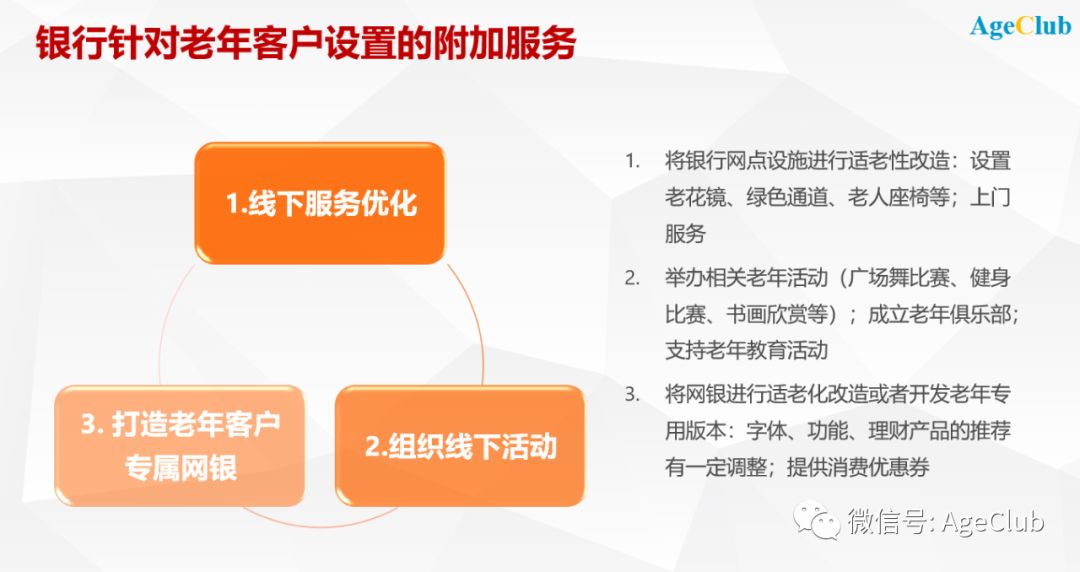

2.8 Offline service optimization

Most middle-aged and elderly people will go to bank outlets for related services. We know from all sources that basically every bank will improve the defects in hardware supporting for the elderly, such as setting up barrier-free ramps and handrails Facilities such as reading glasses and reading glasses will also be equipped with exclusive seats for silver hair, and green service channels will be opened for special customers.

Specialized personnel will also be arranged to provide “on-site” financial services for special customers who cannot physically come to the counter to handle business due to their physical conditions.

2.9 Organize offline events

In addition to improving the business experience of senior users, banks will also organize various offline activities to meet the financial needs of middle-aged and elderly people.

Aiming at the pain point of lack of wealth management knowledge for middle-aged and elderly customers, banks will hold special lectures at outlets and communities to share relevant knowledge on pension management, financial fraud prevention, and online financial management tools.

We will also cooperate with institutions where seniors such as senior universities, community streets, and senior activity centers gather to organize activities that are of interest to seniors to attract the attention of seniors, and teach them to use online financial tools to help the elderly Products are promoted on the spot to actively seek financial markets for the elderly.

Changsha Bank, a local listed bank in Hunan, has also been seeking breakthroughs in financial services for the elderly. It has joined hands with Happy Elderly Newspapers to organize exchange activities to clarify the real needs of the elderly for products and services in order to develop financial products that meet the fundamental interests of the elderly.

It will also jointly launch the “Winter Literature and Art League” event, which will create a stage for self-employment for the elderly students offline at Happy Elderly University. It will also enable Changsha Bank’s various services and services to reach the middle-aged and the elderly, and help them to establish a healthy Financial management concepts.

In addition to providing financial and online tools for senior citizens, they also focus on the spiritual needs of senior customers. For example, special events such as health lectures, square dance competitions, calligraphy and painting appreciation, and sports competitions were held to enhance the stickiness between banks and senior customers.

Since 2017, the Bank of Communications has facilitated the use of more than 3,000 branch offices throughout the country to launch the first “Ward Cup” square dance contest, using “square dance”, a kind of health that middle-aged and elderly people love to see. Lifestyle, guide people to learn to enjoy life in retirement happily.

Community outlets will also provide services such as physical examinations, physiotherapy, and consultation with famous doctors on a regular basis to address the common health problems of the elderly, providing protection for the health of elderly citizens.barrier.

For example, the Yunnan Branch of the Bank of Communications also holds a TCM wellness experience experience event from time to time. Invited a well-known health care expert team across the country to carry out health care lectures and experience activities for middle-aged and elderly customers, take the pulse of the scene, and develop personalized health care programs for middle-aged and elderly people. It has also been welcomed and paid attention by middle-aged and elderly customers.

2.10 Create exclusive online banking for senior customers

Considering that the elderly may have reduced physical functions and inconvenience, they cannot go to the offline sales outlets in person to handle business.

Now the older and more elderly people start to touch the Internet, and they have acquired a certain ability to surf the Internet, and the new elderly people gradually like online convenient services.

For this reason, some banks have established online marketing channels, which provide convenient channels for the promotion and sales of aging financial products and services.

At the same time, considering that the waiting time for processing business is too long, the elderly may be physically exhausted, and an appointment system has been established to reduce the waiting time for elderly customers.

In 2019, ICBC launched a new version of Happy Life Mobile Banking for the elderly. It integrates biometrics and voice to lower the threshold for the elderly to use mobile financial services, and introduced a “one-click help” function to facilitate the elderly in Mobile banking has used interaction, big data, intelligent analysis, etc. to design and develop business processes suitable for the characteristics of the elderly.

China Everbright Mobile Bank launched the “Jane Love Edition” mobile banking this year, and can switch freely with the normal version. The “Jane Love Edition” mobile banking not only adjusts and optimizes the pages of commonly used functions, such as enlarging fonts, using more vivid Color matching, its commonly used functions mainly include: account inquiry, transfer and remittance, sunshine finance and payment recharge.

Banks can also collect and mine information on health and wellness, medical rehabilitation, living services, financial needs and other information of specific groups, grasp user data, and realize precision financial services for the elderly.

2.11 What are the problems in domestic senior finance?

According to relevant data, we have summarized various banks that set up products and services for the elderly. It can be seen that most of the banks’ products and services are still at a relatively basic stage. There are still relatively few banks that can segment and interpret personal financial products and services for most groups.

Currently, China’s pension finance is still in its infancy in terms of innovation and development, and faces many practical difficulties.

-

The elderly wealth management products developed by many banks are similar to conventional wealth management products in terms of purchase thresholds, risks, and returns. They only have a slight increase in the rate of return. Sex. The core concepts of early planning for pension finance and long-term investment based on the status of personal property are not fully reflected;

-

Many members of the public do not have the concept of pension finance. Although the savings rate of residents in China is relatively high, they still remain at a relatively single level of financial products such as savings deposits and wealth management products, and have not yet formed a well-designed asset suitable for everyone Management ecology;

-

Although online financial service platforms have brought convenience to the financial services of the aging population, these channels still need to promote the process of publicity among the elderly.

III. Innovation Cases on Pension Finance

According to relevant statistics, since August 2018, China has launched more than 50 pension target funds to assist the retirement investment of Chinese savers. With the positive progress of the pension product end, how to encourage people to increase their savings and take the initiative to achieve retirement goals through various investment tools will become a big challenge.

3.1 State-owned banks: use their own advantages to apply private banking wealth management services to ordinary customers

The results of the 2019 survey show that, in addition to basic pension awareness, Chinese residents also need more specific and personalized pension guidance and support to help them balance financial target priorities and set personal pension savings goals.

The popularization of pension finance requires going through several stages of awakening consciousness, knowledge accumulation, long-term practice, and habit formation. Providing simple and easy-to-use pension planning tools is an effective way to promote pension finance.

3.1.1 Bank of Communications

This year, Bank of Communications launched the “Ward Pension Plan” on the basis of “Ward Financial Advisors”. Based on the information provided by customers, big data analysis is used to generate financial planning solutions that meet customers’ individual needs based on their risk preferences. With the knowledge of the risks and benefits of each wealth management product, customers can purchase through the Bank of Communications APP with one click.

“Wolder Pension Plan” not only for the elderly, but also for customers of other ages who will eventually enter the elderly life, has established a complete set of pension plans, and everyone can use the Bank of Communications mobile banking app “Financial consultants” find the right one for youFinancial planning program.

By sorting out the real situation of customers and their expectations for the future, we can comprehensively calculate the various financial planning that need to be completed to maintain a reasonable standard of living.

According to our trial of this product, we find that only elderly people over the age of 60 can choose insurance, and the recommended wealth management products for age-appropriate people will not vary much with income.

With the continuous development of “fintech”, users can enjoy financial services through mobile phones. Bank of Communications is committed to creating a new sales scenario, “Bank of Communications Live Broadcasting”, which closely integrates live broadcast and sales. The live broadcast page is the product sales page. Users can complete the financial products by watching and buying with a simple operation, which can greatly improve financial products. Sales conversion.

The live broadcast is mainly divided into four major categories-“Investment in Progress”, “Civil Life”, “The Big Coffee Has Something to Say”, and “Ward Banking Room”.

-

When investing: in the form of social topics, neighborhood collections, etc., and invite financial experts to pass on investment and wealth management knowledge to the audience, and recommend the most suitable products from a professional perspective;

-

Yunhui Life: use story plots such as short stories and life scenes to show usage scenarios and softly embed various preferential welfare activities;

-

The big coffee has something to say: The live broadcast platform invites senior experts from the financial, investment, and collection industries to explain products from the shallow to the deep with professional knowledge and unique insights, and uncover the story behind the industry;

-

Ward Banking Room: Account managers from major branches across the country recommend products that involve investment, wealth management, insurance, etc. Broadcast frequently on a weekly basis and recommend a variety of products for customers with different needs. Live broadcast has also become an important channel for front-line account managers to acquire customers and live customers.

Live content is based on original or popular marketing content to drive traffic. For example: after the new tax regulations were introduced, Bank of CommunicationsThe first time the live broadcast invited experts in the industry to broadcast “Revealing the New Year’s” Tax Reduction Gift Package “-A New Tax Rule You Must Know.”

Or in conjunction with holiday hotspots, during the Christmas season, the Christmas Surprise Big Conjecture is launched. The two teams answer the pk, compete for the final physical gold reward, and implant various products into the pk topic.

During the live broadcast, you can focus on actively interacting with guests and anchors through barrage messages, rewards, likes, etc. At the same time, according to the topic, a lottery turntable, voting gas stations, and encourage customers to participate in interaction, sharing, and fission Communication for marketing purposes.

According to statistics, since the launch of BOCOM Live Broadcast in October 2017, as of April 2019, the cumulative number of reservations has exceeded 3 million, the cumulative viewing has exceeded 8 million, and the cumulative number of interactive points of praise and praise has reached nearly 10 million. There are more than 7.5 million interactive barrage.

Among them, the single-stage live broadcast of the finals of the “Bank of Communications” “Ward Cup” square dance contest in 2018 reached 260,000 people, and the number of likes and comments was close to millions.

3.1.2 Construction Bank

In addition to the Bank ’s online banking app, CCB has developed a financial technology application product “Relief for the Aged” app for the elderly in the field of innovation to achieve full service coverage. Its functions include:

-

Support the acquisition of elderly resources, help the elderly find suitable resources and enjoy services through the elderly platform;

-

Realize intelligent management of elderly health information, and measure daily health and safety warnings through smart devices;

-

Meeting children and health care workers to check and care for the health, safety and care information of the elderly;

-

Meet the interaction, reminders and greetings of the elderly and children on the APP;

-

You can buy senior care products on the platform, including household appliances, dietary aids, household daily use, etc.

In addition to conducting online research on elderly care, CCB has also made arrangements for other people with elderly care needs.

We found that there is a small program called “Timing Time Machine” produced by CCB Fund Wealth in Alipay, which aims to unlock new options for pension management for more people. This small program is based on the calculation of future pensions and is calculated based on relevant interest ratesIncome generated after investment.

3.2 Commercial banks: CITIC and Industrial Bank vigorously develop pension finance

Some banks have gradually pursued income and profits and even social value assessment from the initial “race horse enclosure”, while others still have the main goal of expanding their business scale, and they have also sought to transfer to personal business lines or corporate operations. breakthrough.

As early as 2012, Industrial Bank began to promote pension finance, planning to launch pension finance, pension industry finance, pension retail finance, and established a pension finance center.

Slightly different from other banks’ methods of collecting middle-aged and elderly users, Industrial Bank mainly works in community banks, which is an important platform for the bank to expand retail channels and achieve breakthroughs in retail business transformation.

In order to consolidate the elderly customer base it has, it focuses on introducing exclusive pension financial services in community banks, as well as withholding services that provide daily consumption.

After years of exploration and experimentation, the development of the Industrial Bank’s community banks has gradually improved, with more than 1,000 establishments, 80% of the elderly in the customer group, and more than 60% of the total assets contributed by the elderly customers.

According to its official data, nearly 60% of community banks’ more than 160 billion financial assets are held by elderly people.

CITIC Bank also planned to enter the field of pension finance at an early stage, seizing the entire elderly financial market including pension, wealth management, health, and wealth inheritance.

One of the Industrial Bank ’s retail brands, “Anyu Life”, corresponds to the pension finance business. Take “Anyu Life” as an example. In just two years after its launch, VIP customers have exceeded 1 million and the entrusted assets have exceeded 510 billion yuan, of which the sales channels of community bank outlets have contributed.

3.2.1 CITIC Bank

CITIC Bank has started to provide pension finance since 2009. The first is the launch of the first “Happy Years” debit card for the elderly in China. In 2012, it was the first to carry out aging transformation at outlets across the country. In 2016, the company launched the “Monthly Interest” large-value deposit certificate product for senior citizens, which has reached RMB 102.3 billion yuan. In 2017, the “notarized pension” business was launched, providing will testimony, property notarization and financial services to nearly 10,000 elderly people.

In 2019, we plan to provide “happiness +” elderly university information platform to more than 70,000 seniors and 8 million students in the country. It also provides more than 300 to the residents’ communityOnline learning opportunities for middle-aged and elderly people’s intelligent life courses, published and distributed the country’s first reading book on financial knowledge for the elderly.

In October 2019, CITIC Bank launched the country’s first elderly-only credit card. The age of applicants has been relaxed to 70. In addition to basic flight delay insurance, fraud protection insurance, VIP line and concierge services, it also integrates elderly The health and travel concerns of the customer base bring multiple customized benefits.

At present, the service quality of CITIC Bank in operating elderly customers is among the leading echelons in the industry. As of the end of October 2019, CITIC Bank’s elderly customers reached 12.64 million, with assets under management reaching 1.04 trillion yuan, and the proportion of assets managed by all retail customers reached 52.62%.

At present, CITIC Bank’s pension financial system has several major functions: one is to provide a set of pension financial products tailored for the elderly; the other is to provide 7 * 24-hour VIP family doctors for senior VIP customers, Services such as health consultation; third, providing a set of “smart life courses”, including wealth appreciation and inheritance, using mobile payments, and preventing financial fraud; fourth, organizing a variety of elderly culture and art contests to enrich the cultural life of the elderly.

3.3 Internet finance joins the pension camp

In addition to the middle-aged and elderly people’s investment behavior in order to better support the elderly, the younger people have also begun to plan their own elderly life.

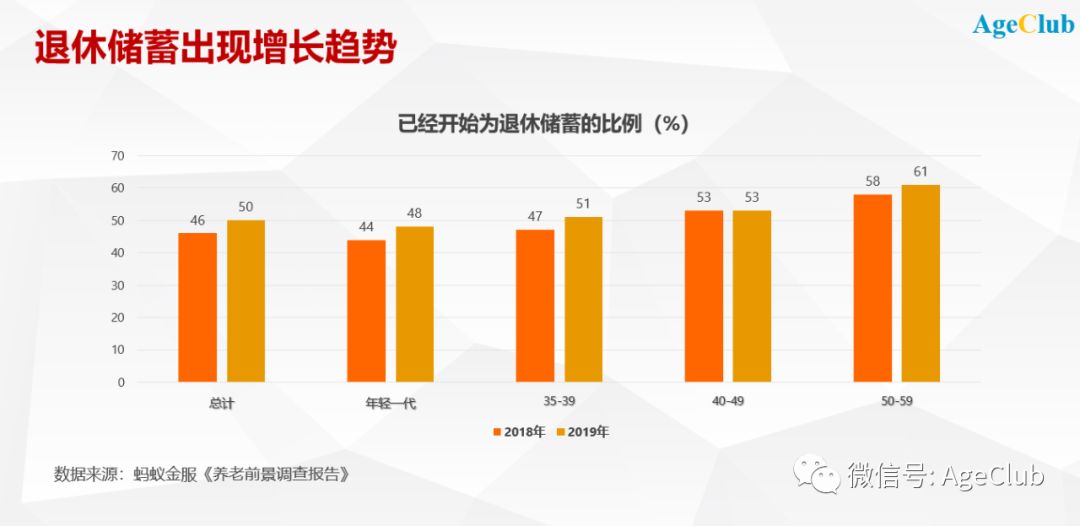

Data from this year’s Ant Wealth and Pension Outlook Survey report show that more respondents are beginning to save. And among the younger generation of those who have started saving, more than half have started before the age of 30.

The report proposes that this information is basically consistent with the trend observed on Ant Wealth Platform: Although the amount of investment in the initial stage is not high, the people who are starting to manage pensions are becoming younger.

In addition to traditional financial institutions, Alipay, which has a large number of young and middle-aged users, has also joined the pension finance camp.

We found that Alipay’s wealth management service also has an embedded wealth management section, which has a long entry path and is not easy to find. Increased retirement income.

It will also calculate the risk appetite based on Alipay’s back-office on my asset income and recommend related financial products.

In addition to Alipay’s own endowment financial management program, the APP also embeds endowment financial management programs produced by other financial institutions.

These financial management products are mainly based on the popular science knowledge of “Encyclopedia of Senior Citizens” as the recommendation point. At the end of the article, the connection of financial management products is attached.

From the comments on the article, we can see that old-age wealth management products are still attracting attention. Middle-aged people who are approaching retirement age will pay attention to these products, and some customers will also pay attention to the issue of fund inheritance. Each comment also has customer service. answer.

The Alipay approach has shortened the distance between young people and old-age financial management, and provides a more direct and convenient way to understand and purchase channels for people who have rarely visited bank outlets.

3.3 Japan Case: Second Life and Dementia Trust

3.3.1 Customize financial solutions according to life wishes and occupation categories, and start a happy second life

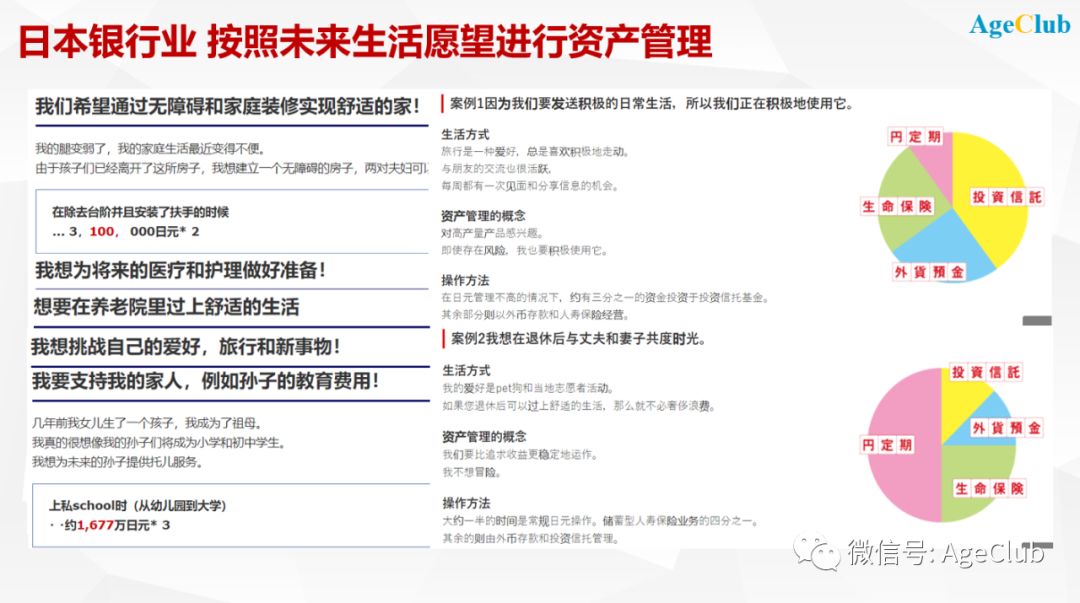

The Japanese banking industry generally uses “Second Life” as its core concept to describe life after retirement. The concept conveyed is that after retirement, it is not a sign that people are beginning to age, but a starting point for a wonderful Second Life.

Mitsubishi UFJ Bank is the largest commercial bank in Japan. It sets up a pension management calculation model for senior customers. Based on the results of the Ministry of Health and Welfare survey, it calculates that the 65-year-old will spend a total of 90 years in daily life, travel, health, and children. How much money, and indicate the difference in income between property management and non-property management.

Different from the domestic pension financial product recommendation method, the asset allocation of elderly customers will provide customers with diversified financial products, services and solutions based on different risks, income preferences and personal living conditions. Financial productsMeet customers’ personalized asset management needs.

It will also recalculate the cost of senior care and recommend related asset management product portfolios according to the current arrangement of the assets and the future life vision of the elderly.

For example, if the client needs to live a stable old life, he will propose to increase the proportion of regular savings and decrease the proportion of investment trusts and foreign currency funds, but a part of it will be reserved for future life security.

In addition to following the elderly’s future plans, customers will be roughly divided into civil servants, corporate employees, self-employed households, housewives, etc. according to occupational types and types of pensions, and then analyze the financial management of pensions based on their family attributes and consumption.

3.3.2 Financial solutions for certain elderly diseases

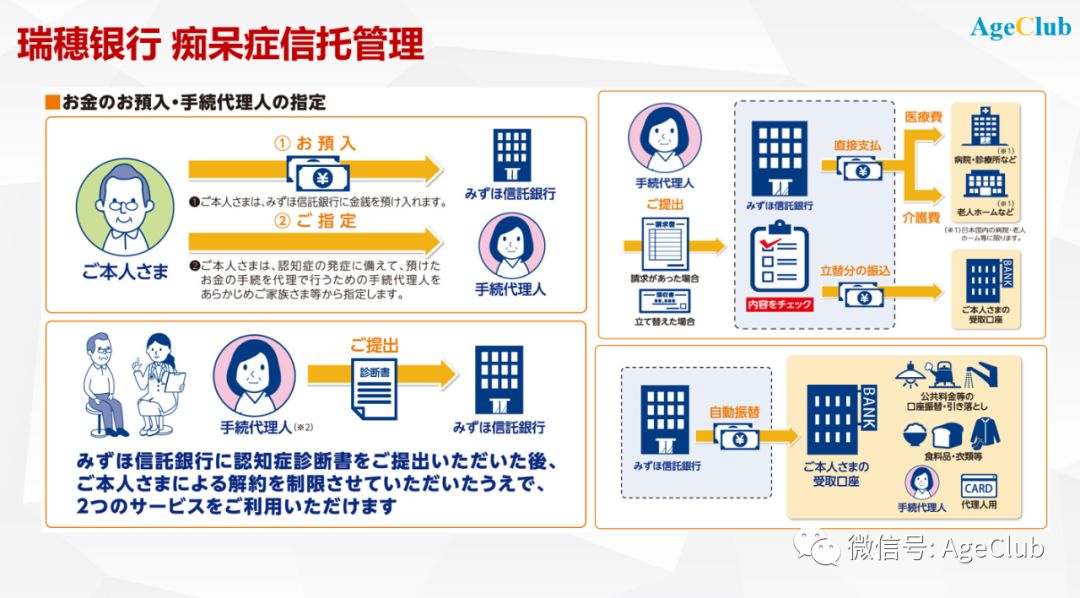

According to reports, in 2017 Japanese dementia patients held 143 trillion yen (about 8.7 trillion yuan) in financial assets.

It is estimated that Japanese household financial assets will reach 2070 trillion yen (about 125.6 trillion yuan) by 2030, and the assets held by dementia patients will increase to 215 trillion yen.

It is estimated that the stocks and other securities held by the elderly with dementia will reach 15% of the total of Japan by 2035.

In this situation, Mizuho Bank launched the Dementia Trust, which can be prepared before the occurrence of dementia, so even if the client has dementia, his money can be smoothly used for living expenses and medical expenses.

If the doctor diagnoses the client with dementia, he can submit a hospital certificate to MizuhoTrust bank. From the perspective of fraud prevention, the bank can transfer the trust property to the savings account according to the specified amount and frequency, and use it for living expenses, expensive medical expenses, and nursing expenses according to the requirements of the program agent. Wait.

On the way to gradually entering a oligosocial and aging society, we must not only have a wealth management awareness of rational planning in the future, but also financial institutions must be able to stand on the standpoint of the elderly and provide a real benefit for the elderly Financial products and services enable us to achieve a wonderful Second Life after retirement.

-

-

-

-

-