How to survive the cold winter will be a problem that car companies must face.

Editor’s note: This article comes from “ Future Car Daily ” (WeChat public account ID: auto-time), author: Jiaoman Ting.

Article | Jiao Manting

Edit | Xu Yang

“The first winter in the Chinese passenger car market is coming. Although this does not necessarily mean that China’s growth engine has completely stalled, it does pose a challenge for OEMs who have never experienced the winter.” BCG thinks so.

In January 2020, the Boston Consulting Group (BCG) released a report, “Knowing the Change and Responding to Success-How Car Companies Can Rise in the Downward Market,” said that starting in 2017, passenger cars The market entered a negative growth area, and 25 consecutive years of growth officially came to an end. BCG predicts that the market will continue to decline for two years, and it will continue to test about 4% before returning to growth, after which the market will return to a modest growth trend.

Specifically, in the short term, the possibility of an immediate rebound in the passenger car market is unlikely, and the bottom of the passenger car market will appear in the next two years or so.

It can be seen from the government ’s recent relaxation of restrictions on joint ventures, double points policy, and cancellation of the “white list” of power batteries that the government ’s attitude toward the automotive industry has changed from escorted to guided innovation. The upside is that the pace of further declines in the passenger car market is slowing. Factors leading to the decline in current sales, such as the withdrawal of the last round of purchase tax deductions and the impact of the switch to the Sixth National Standard, are fading.

Long-term observation, compared with mature markets in China’s current stage of development, China ’s passenger car penetration rate is much lower. In addition, the rise of shared mobility does not have a significant impact on car purchase demand. This means that China’s car ownership has sufficient growth potential. BCG predicts that the overall penetration rate of passenger cars in the age-appropriate population (15-64 years old) will increase from about 160 cars per thousand people today to about 310 cars per thousand people by 2030.

In China, the increase in future profits is concentrated in emerging areas, especially considering that China is at the forefront of exploring innovative business of “autonomous driving, connected cars, electric vehicles, and shared mobility” and requires more investment To keep up with the trend.

BCG expects that the market downturn coincides with key investment windows for new technologies. It states that Chinese hosting vendors areFaced with a “double blow”: On the one hand, the main business profit has continued to decrease; on the other hand, new business areas still require continuous blood transfusion. Under this premise, the profitability of car companies is facing a severe test, and it is expected that they will face a risk of a substantial decline of about 20% to 30% in the next few years. Mainframe vendors that have sustained losses and lost market share in recent years will be forced out.

“We have observed a large amount of R & D investment by mainstream host manufacturers, and we expect more investment in the next few years, mainly in the areas of electrification, autonomous driving, and upgrading of traditional components.” BCG said.

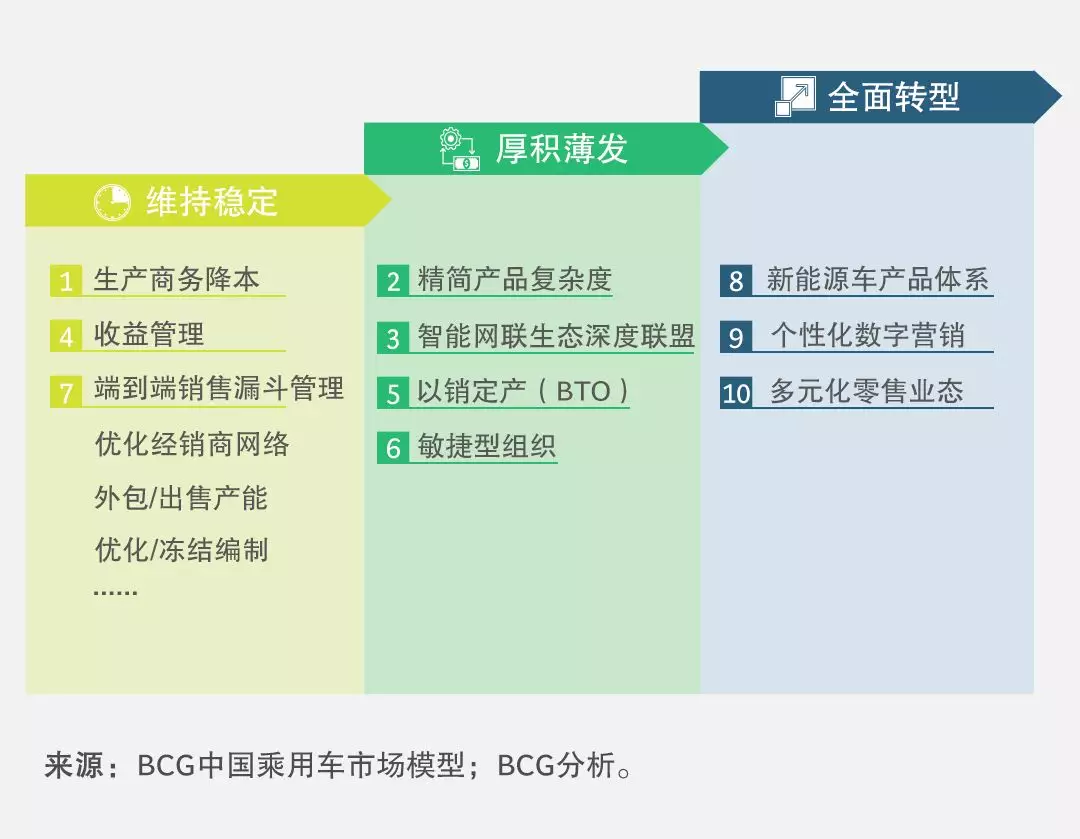

Under the cold winter situation, BCG provides the “good strategy for winning” for the mainframe manufacturers. BCG believes that there are three key goals that mainframe vendors need to achieve in the next few years: 1. Maintaining stability in the short term and evaluating feasible solutions that can quickly improve the status quo; 2. Accumulating in the medium term: Specializing key functions To continuously improve profitability; 3. Long-term comprehensive transformation, actively support innovation, and invest in key areas to maintain competitiveness.

In the short term, the three major problems of idle factory capacity, loss of distribution network, and insufficient investment resources are urgent.

To cope with the problem of idle factory capacity, mainframe manufacturers can turn to China ’s increasingly recognized export market for products, manufacture for new forces that do not have production capacity or licenses, and sell capacity to industry with limited experience but Well-funded new entrants.

To deal with the loss of distribution network, a basic principle is that it is better to keep a small and healthy network than to collapse the entire channel together. BCG found that some mainframe vendors are closing low-performance stores, concentrating resources to support the remaining stores, and strengthening cooperation with major dealer groups.

As for the lack of investment resources, BCG recommends streamlining research and development costs, focusing only on key topics, and forming alliances with other industry participants.

In the face of long-term profitability challenges, mainframe manufacturers can take advantage of five major grasps to achieve key function specialization, including streamlining products to focus on specific market segments, seeking cooperation to reduce investment and hedging risks, and precise personalized markets Marketing, building a leaner, faster and more flexible organization and empowering resellers to help OEMs increase their profits by 20-30%.

Automotive companies must also undergo a comprehensive transformation and continue to invest in key projects to maintain long-term competitiveness.

In the field of new energy, China is a global leader. It is expected that by 2030, pure electric vehicles (BEVs) will account for 30% and plug-in hybrid (PHEV) vehicles will account for 5% of China’s passenger car sales.. Under this trend, mainframe manufacturers should build systemic product platforms to respond to faster iterations of new energy vehicle products.

Meanwhile, Chinese consumers are used to digital channels. Hosting companies need to grasp the media browsing habits and purchasing habits of young consumer groups to carry out personalized and digital user lifecycle management transformation.

Also, in China, low-tier cities are on the rise. The original 4S store investment model challenged the profit model. Establishing an efficient and financially sustainable network model for low-tier cities is an important issue for channel development.

Picture from BCG