In the first quarter of the A-share market, there will be hardly any spring turbulence, but Davis may have a double kill.

Editor’s note: This article is from WeChat public account “Suning Fortune Information” (ID: SuningWealthInsights), authors Gu Huijun and Lu Shengbin.

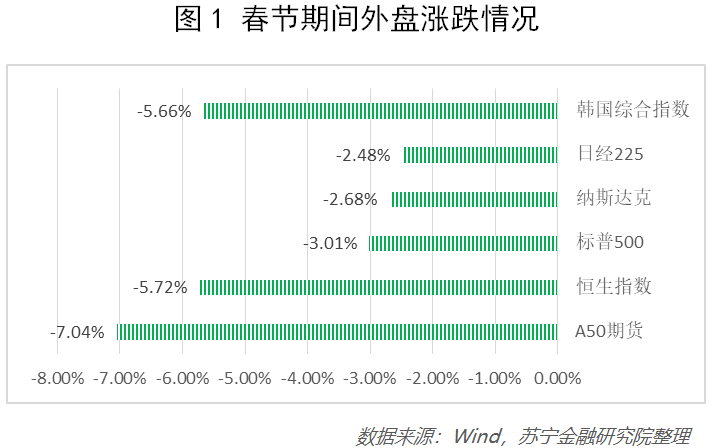

On the last trading day before the Spring Festival, A shares suffered a severe setback under the influence of the outbreak of fermentation, and then closed for the Spring Festival holiday. During this period, US stocks and Hong Kong stocks were significantly affected (see Figure 1).

It can be seen that The pneumonia epidemic not only affects our lives, but also strains the nerves of global capital markets.

As the opening of the A-share market is approaching and the risk aversion is reflected in advance in the outer disk, the World Health Organization has listed the new coronavirus pneumonia as an “international public health emergency”. What will the A-share market react to and what should investors do In response, this article will give some suggestions based on the reaction of the capital market after the outbreak of SARS and other regions for readers’ reference.

Overall impact

First look at the impact of previous epidemics on the capital market. As can be seen from Figures 2, 3, and 4 below, during the initial and peak periods of the epidemic, the capital market did receive a relatively large impact, but in the following 1-3 months, a relatively obvious rebound occurred.

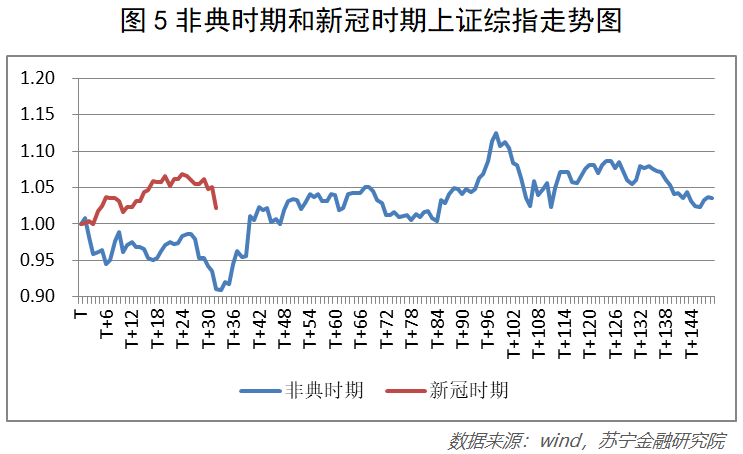

The cause, development and social impact of this epidemic have many similarities with SARS in 2003, and the impact on the capital market can also be used for reference (see Figure 5). During the SARS period, the panic in the capital market did not spread due to the lack of attention in the initial stage. After the periodical correction, there was a spring turmoil in the market. During the severe period of the epidemic, the Shanghai Composite Index made a significant correction, with a cumulative decline of 7%.

Reviewing the SARS period in 2003, in the short term, the impact of the different stages of the epidemic will have a significant (about 7%), short-term (about 7 trading days) negative impact on the A-share market, and then it will enter a consolidation or The rebound period; in the medium term, with the end of the epidemic, the obvious decline in GDP in the second quarter has gradually affected the capital market, and A shares have entered a 4-month decline cycle with a decline of 13%; in the long run, China ’s macroeconomic Except for the quarterly decline, there was no trend decline. During the overall epidemic, monetary policy remained stable and liquidity remained loose, thus not changing the long-term trend of China’s economy and capital market. Therefore, in terms of prolonged cycles, The impact of the A-share index is relatively small.

Compared with the current development of the new crown epidemic, the strong movement of personnel during the Spring Festival has basically determined that the high incidence of the epidemic will be concentrated from February 1 to February 15, and it is expected to reach its peak in April to May . In the short term, compared with the SARS period, the national control of this epidemic is timely and efficient, and national awareness and self-isolation are strong, which will help shorten the spread and outbreak of the epidemic; but the severity of the epidemic It has also surpassed SARS. As of January 28, the number of new coronavirus diagnosed has exceeded the number of SARS diagnosed in 2003, and the follow-up uncertainty is still large. Therefore, it is expected that the fermentation and market digestion of this epidemic situation will be significantly faster than during the SARS period, and the A-share market as a whole is characterized by “short callback time and deep range.”

In the medium term, the overall profitability of A shares in the third quarter of last year has stabilized or even weakly recovered. The market is expected to improve in the fourth quarter and the first quarter of this year. The profit situation in the first quarter is not optimistic, which will produce poor profit expectations, which will drive the overall decline of the A-share market; after the valuation level has risen sharply in 2019, it is currently difficult to improve.As a result, with the expectation of capital outflow and weakening sentiment, the valuation may fall sharply, so A-shares in the first quarter will not have a spring turmoil, but Davis may have a double kill.

In the long run, the impact of the outbreak on the A-share index is expected to be small. On the whole, the current Chinese economy is very different from that in 2003. Soon after China joined the WTO in 2003, it was the starting point for its rapid economic growth. At present, China’s economy is in a downward cycle; it is also because the WTO accession in 2003 did not last long. China’s linkage with the world economy is weak, while China’s accession to the WTO has been long since now, and it is deeply bound to the world.

In the short and medium term, the hedging effects of macro policy also need to be considered. The epidemic may prompt the central government to proactively introduce monetary and fiscal policies, such as tax deductions and subsidies for specific industries, and even comprehensive cuts in interest rates / rates. If the policy stimulus exceeds expectations, it will affect the A-share market. Bringing a positive impact, thereby counteracting the negative impact of the epidemic.

Specificity during the epidemic

In 2019, the net inflow of foreign capital exceeded 350 billion yuan, and the annual turnover of northbound funds was close to 10 trillion yuan, accounting for about 7.6% of the total A-share turnover. It has become an important part of the A-share market that cannot be ignored. In addition to the expansion of Mingsheng, FTSE Russell, and S & P Dow Jones Indices, A-shares have brought a large amount of foreign passive investment funds, and the high-quality assets of A-shares have also attracted many active allocation funds. Since the outbreak of this epidemic on the Internet, foreign capital has continued to withdraw on a large scale. During the three trading days from January 21 to January 23, foreign capital continued to net out, accumulating up to 19.6 billion. During the A-share market break, when the external disk fell sharply and concerns about the epidemic continued to spread, the risk appetite of foreign capital will significantly decrease. It is expected that a large number of foreign investment will leave the market shortly after the opening of the A-share market, which will have a certain impact on the A-share market. .

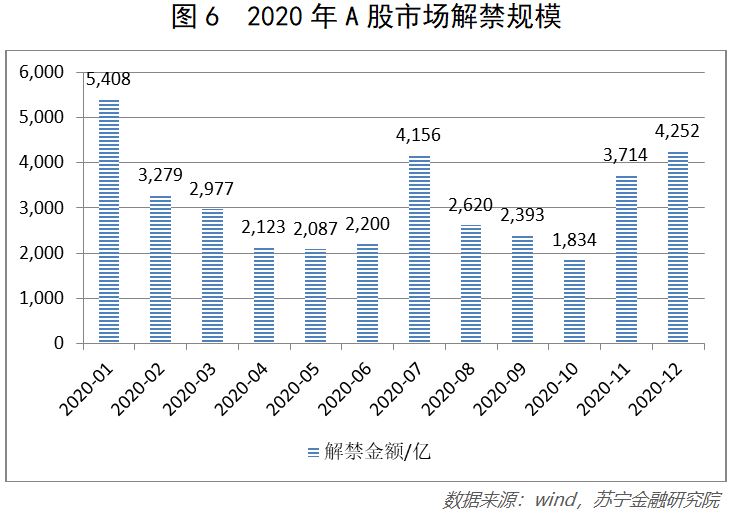

2020 is the period of centralized lifting of the A-share market (see Figure 6). The total amount of lifting of the ban in the first quarter reached 1.17 trillion. According to the impact ratio of approximately 10% in 2019, the impact of the reduction in holdings on the A-share market in the first quarter It will exceed 100 billion; the scale of lifting the ban in January will reach 540.8 billion, which will put some pressure on the A-share market.

Analysis of asset allocation for large categories

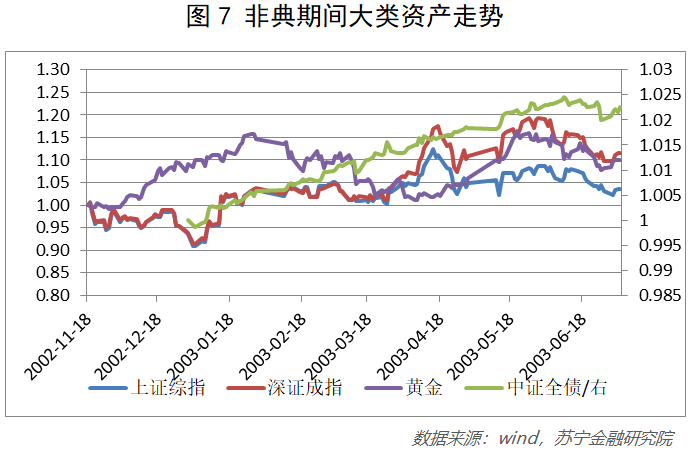

While watching SARS in 2003,These assets have different trends (see Figure 7). The stock market will be more obvious in the short to medium term, and the price of crude oil will be even more severe. During the SARS epidemic, Brent crude oil experienced a short-term huge correction of 31.4%, which lasted for about one and a half months, and then slowly rebounded. The main reason is that the market expects that the epidemic will have a strong impact on heavy industry (the fact also proves that China ’s heavy industry fell by 8.1% from February to May 2003), resulting in a significant contraction in crude oil demand. Since January 20 this year, the price of crude oil has fallen by more than 10%, and it is expected that it has not been adjusted.

Gold as a safe-haven asset during the SARS epidemic experienced a periodical rise only when the epidemic was severe, with an increase of approximately 15% and a duration of approximately one and a half months. Since January 20 this year, the price of gold has risen by nearly 1.5%. The current Brexit boots have landed, the first phase of the Sino-US trade agreement has been reached, and the tension between the United States and Iran has gradually faded. It is expected that the price of gold will be more susceptible to the new crown epidemic. Therefore, in the short term, the current investment value of gold is more certain.

During the SARS epidemic, the bond index rose steadily. Although the market interest rate gradually increased in 2002, the market interest rate began to fall due to the market’s concerns about economic recovery. However, during the peak of the epidemic in April and May, interest rates accelerated downward. The yield on 10-year Treasury bonds fell from 3.2% to about 2.85%; after the epidemic ended, in order to alleviate the domestic economy overheating and prices rise too fast, both the policy side and the capital side were tightened, and the bond market entered a bear market cycle. Therefore, during the epidemic fermentation period, it is recommended to focus on investment opportunities in interest rate debt.

In general, during the SARS epidemic, domestic house prices continued to rise steadily without any significant impact. Therefore, the impact of the epidemic on housing prices can basically be ignored, and it is expected that the current housing prices will remain stable.

U.S. stocks have not been significantly affected during the SARS epidemic and have not changed their upward trend. In Southeast Asia, which has also been affected by the epidemic, except Vietnam, which is similar to A shares, the markets of other countries have not been significantly affected. But now that China has entered the WTO for almost 20 years, both on the supply side and the demand side, China has long been deeply bound to the world. Therefore, while affecting the domestic economy and capital market, the epidemic will also affect the world economy and the global capital market. Shock, the decline in the global capital market during the Spring Festival is proof, if the opening of A shares drops sharply, it will also bring short-termThe global capital market fell further.

A-share industry analysis

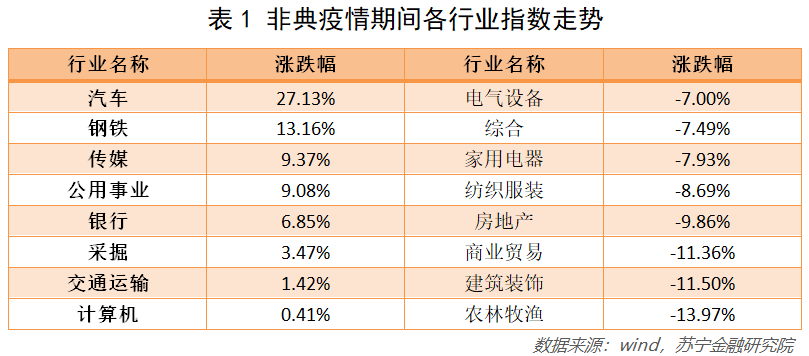

Reviewing the trends of various industry indexes during the SARS epidemic in 2003 (see Table 1), the industries with the largest gains were automobiles, steel, media, and public utilities, while the industries with the largest declines were agriculture, forestry, animal husbandry and fishery, building decoration, and commercial trade And real estate, structural investment opportunities are obvious. Looking at the industries with the highest gains, we can see that in 2003 China mainly relied on investment to drive economic growth.

Follow the industry:

(1) Medical organisms: Although during the SARS epidemic, the medical organisms fell by 2.68% as a whole, there was a significant excess return during the fermentation period in April; SARS has advanced in advance. This section fell by more than 3.3% in the two trading days before the market closed for the Spring Festival this year. It is recommended to continue to pay attention to the opportunity to increase positions.

(2) Media: In order to avoid large-scale gathering of people, this year ’s Spring Festival movie theaters are all offline. The online premiere of “Aunt” has a great impact on offline theaters. Be wary of this fine-molecule industry; online video has become a beneficiary sub-sector during the epidemic, eating up offline market share, and there will be significant excess returns in the short term.

(3) Banks: The current valuation of banks is low and the dividend yield is high. Under the risk aversion mood, they can focus on excess returns and increase market preferences brought by stable dividend yields.

Be wary of the industry:

(1) Commercial trade, transportation, leisure services: Experience in the SARS epidemic Under the lessons, this year’s Chinese New Year has seen a marked decrease in staff turnover and a strong willingness of citizens to isolate themselves, which will inevitably have an impact on these industries. Due to the rapid development of e-commerce, the impact of the textile and apparel sector is expected to be less than that during the SARS period.

Summary

The opening of A shares is approaching. It is recommended to pay attention to the short-term investment opportunities of gold and interest rate bonds. For A shares, it is recommended to focus on defensive and structured investment in the short term, and pay attention to the industries such as medical biological callback, online media, and banking.

This article does not constitute investment advice

In 2019, the net inflow of foreign capital exceeded 350 billion yuan, and the annual turnover of northbound funds was close to 10 trillion yuan, accounting for about 7.6% of the total A-share turnover. It has become an important part of the A-share market that cannot be ignored. In addition to the expansion of Mingsheng, FTSE Russell, and S & P Dow Jones Indices, A-shares have brought a large amount of foreign passive investment funds, and the high-quality assets of A-shares have also attracted many active allocation funds. Since the outbreak of this epidemic on the Internet, foreign capital has continued to withdraw on a large scale. During the three trading days from January 21 to January 23, foreign capital continued to net out, accumulating up to 19.6 billion. During the A-share market break, when the external disk fell sharply and concerns about the epidemic continued to spread, the risk appetite of foreign capital will significantly decrease. It is expected that a large number of foreign investment will leave the market shortly after the opening of the A-share market, which will have a certain impact on the A-share market. .

2020 is the period of centralized lifting of the A-share market (see Figure 6). The total amount of lifting of the ban in the first quarter reached 1.17 trillion. According to the impact ratio of approximately 10% in 2019, the impact of the reduction in holdings on the A-share market in the first quarter It will exceed 100 billion; the scale of lifting the ban in January will reach 540.8 billion, which will put some pressure on the A-share market.

Analysis of asset allocation for large categories

While watching SARS in 2003,These assets have different trends (see Figure 7). The stock market will be more obvious in the short to medium term, and the price of crude oil will be even more severe. During the SARS epidemic, Brent crude oil experienced a short-term huge correction of 31.4%, which lasted for about one and a half months, and then slowly rebounded. The main reason is that the market expects that the epidemic will have a strong impact on heavy industry (the fact also proves that China ’s heavy industry fell by 8.1% from February to May 2003), resulting in a significant contraction in crude oil demand. Since January 20 this year, the price of crude oil has fallen by more than 10%, and it is expected that it has not been adjusted.

Gold as a safe-haven asset during the SARS epidemic experienced a periodical rise only when the epidemic was severe, with an increase of approximately 15% and a duration of approximately one and a half months. Since January 20 this year, the price of gold has risen by nearly 1.5%. The current Brexit boots have landed, the first phase of the Sino-US trade agreement has been reached, and the tension between the United States and Iran has gradually faded. It is expected that the price of gold will be more susceptible to the new crown epidemic. Therefore, in the short term, the current investment value of gold is more certain.

During the SARS epidemic, the bond index rose steadily. Although the market interest rate gradually increased in 2002, the market interest rate began to fall due to the market’s concerns about economic recovery. However, during the peak of the epidemic in April and May, interest rates accelerated downward. The yield on 10-year Treasury bonds fell from 3.2% to about 2.85%; after the epidemic ended, in order to alleviate the domestic economy overheating and prices rise too fast, both the policy side and the capital side were tightened, and the bond market entered a bear market cycle. Therefore, during the epidemic fermentation period, it is recommended to focus on investment opportunities in interest rate debt.

In general, during the SARS epidemic, domestic house prices continued to rise steadily without any significant impact. Therefore, the impact of the epidemic on housing prices can basically be ignored, and it is expected that the current housing prices will remain stable.

U.S. stocks have not been significantly affected during the SARS epidemic and have not changed their upward trend. In Southeast Asia, which has also been affected by the epidemic, except Vietnam, which is similar to A shares, the markets of other countries have not been significantly affected. But now that China has entered the WTO for almost 20 years, both on the supply side and the demand side, China has long been deeply bound to the world. Therefore, while affecting the domestic economy and capital market, the epidemic will also affect the world economy and the global capital market. Shock, the decline in the global capital market during the Spring Festival is proof, if the opening of A shares drops sharply, it will also bring short-termThe global capital market fell further.

A-share industry analysis

Reviewing the trends of various industry indexes during the SARS epidemic in 2003 (see Table 1), the industries with the largest gains were automobiles, steel, media, and public utilities, while the industries with the largest declines were agriculture, forestry, animal husbandry and fishery, building decoration, and commercial trade And real estate, structural investment opportunities are obvious. Looking at the industries with the highest gains, we can see that in 2003 China mainly relied on investment to drive economic growth.

Follow the industry:

(1) Medical organisms: Although during the SARS epidemic, the medical organisms fell by 2.68% as a whole, there was a significant excess return during the fermentation period in April; SARS has advanced in advance. This section fell by more than 3.3% in the two trading days before the market closed for the Spring Festival this year. It is recommended to continue to pay attention to the opportunity to increase positions.

(2) Media: In order to avoid large-scale gathering of people, this year ’s Spring Festival movie theaters are all offline. The online premiere of “Aunt” has a great impact on offline theaters. Be wary of this fine-molecule industry; online video has become a beneficiary sub-sector during the epidemic, eating up offline market share, and there will be significant excess returns in the short term.

(3) Banks: The current valuation of banks is low and the dividend yield is high. Under the risk aversion mood, they can focus on excess returns and increase market preferences brought by stable dividend yields.

Be wary of the industry:

(1) Commercial trade, transportation, leisure services: Experience in the SARS epidemic Under the lessons, this year’s Chinese New Year has seen a marked decrease in staff turnover and a strong willingness of citizens to isolate themselves, which will inevitably have an impact on these industries. Due to the rapid development of e-commerce, the impact of the textile and apparel sector is expected to be less than that during the SARS period.

Summary

The opening of A shares is approaching. It is recommended to pay attention to the short-term investment opportunities of gold and interest rate bonds. For A shares, it is recommended to focus on defensive and structured investment in the short term, and pay attention to the industries such as medical biological callback, online media, and banking.

This article does not constitute investment advice

Reviewing the trends of various industry indexes during the SARS epidemic in 2003 (see Table 1), the industries with the largest gains were automobiles, steel, media, and public utilities, while the industries with the largest declines were agriculture, forestry, animal husbandry and fishery, building decoration, and commercial trade And real estate, structural investment opportunities are obvious. Looking at the industries with the highest gains, we can see that in 2003 China mainly relied on investment to drive economic growth.

Follow the industry:

(1) Medical organisms: Although during the SARS epidemic, the medical organisms fell by 2.68% as a whole, there was a significant excess return during the fermentation period in April; SARS has advanced in advance. This section fell by more than 3.3% in the two trading days before the market closed for the Spring Festival this year. It is recommended to continue to pay attention to the opportunity to increase positions.

(2) Media: In order to avoid large-scale gathering of people, this year ’s Spring Festival movie theaters are all offline. The online premiere of “Aunt” has a great impact on offline theaters. Be wary of this fine-molecule industry; online video has become a beneficiary sub-sector during the epidemic, eating up offline market share, and there will be significant excess returns in the short term.

(3) Banks: The current valuation of banks is low and the dividend yield is high. Under the risk aversion mood, they can focus on excess returns and increase market preferences brought by stable dividend yields.

Be wary of the industry:

(1) Commercial trade, transportation, leisure services: Experience in the SARS epidemic Under the lessons, this year’s Chinese New Year has seen a marked decrease in staff turnover and a strong willingness of citizens to isolate themselves, which will inevitably have an impact on these industries. Due to the rapid development of e-commerce, the impact of the textile and apparel sector is expected to be less than that during the SARS period.

Summary

The opening of A shares is approaching. It is recommended to pay attention to the short-term investment opportunities of gold and interest rate bonds. For A shares, it is recommended to focus on defensive and structured investment in the short term, and pay attention to the industries such as medical biological callback, online media, and banking.

This article does not constitute investment advice