From “small screen” to “big screen”, why do mobile phone brands “cross-border” go the same way?

Editor’s note: This article is from the micro-channel public number “smart relativity” (ID: aixdlun) , Author: She Kaiwen .

A few days ago, the American chip giant Broadcom sent Netflix to the defendant’s seat, and Broadcom sued Netflix for infringing eight technology patents related to online video services.

Broadcom said that Netflix’s infringement has led to an increase in the “squad family”, which has reduced the demand for Broadcom chips. The so-called “Square Line” refers to those who favor online video services and abandon traditional cable TV services.

Actually, it ’s not just the “squash clans” that are growing, but the global “non-TV families” has also been growing rapidly in recent years. At this stage, it can be said that the entire TV industry chain is in an “anxious” state.

But at the same time, the domestic market is “lively and abnormal”. Since 2018, major mobile phone brands have entered the TV market. OPPO recently confirmed that it will enter the smart TV industry. What are the charms of the TV market that allow mobile phone brands? Are they rushing?

01 grab the market? Show strength? What is the mobile phone brand map?

If the smartphone market is a “Red Sea,” then the TV market is actually a “Bitter Sea.” From the perspective of the industry as a whole, the TV market has already reached the ceiling of the market, and it has been in a slight increase or decline in the past two years.

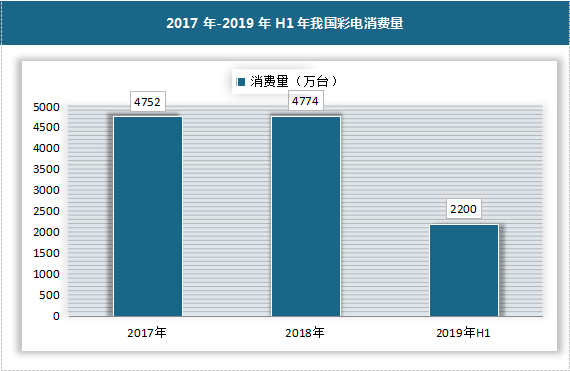

According to data released by the China Electronics Chamber of Commerce, domestic color TV consumption in the first half of 2019 was about 22 million units, a decrease of 4.3% year-on-year, and the annual consumption situation is expected to be at most the same as 2018.

Data source: public data collation

In 2020, we encountered a “black swan” start. According to AVC data, in the ninth week of 2020 (the first two months), the retail sales of color TVs in the offline market fell by 56.2% year-on-year.

And AVC predicts that the scale of retail sales of China’s color TV market will shrink further in 2020, with 46.13 million units sold throughout the year, down 3.3% year-on-year; retail sales of 126.2 billion yuan, down 5.8% year-on-year.

In terms of market competition, the color TV market is already extremely fierce.The competition is mainly concentrated in two camps, one is the QLED camp led by Samsung and TCL, and the other is the OLED camp clustered by many brands such as Hisense, LG, Konka, Skyworth, Changhong, Sony, and Philips.

Before the “mobile phone brands” entered the market, they were already in trouble, especially online channels. The price war was extremely fierce and reached the “peak” in 2019. According to AVC data, color TV products retail in 2019 The amount was 134 billion yuan, a year-on-year decrease of 11.2%. The industry average price was 2809 yuan, a year-on-year decrease of 9.4%, the lowest in ten years.

How do you think the color TV market is a “pit”, but still can’t stop the future of Xiaomi, redmi, Huawei, glory, realme, one plus, OPPO, can’t help but wonder what they are planning?

At first glance, the “intelligence theory of relativity” has several aspects, or the key that drives them to “know that there are tigers in the mountains, and that they are biased towards tiger mountains.”

First of all, an obvious common feature of mobile phones and TVs is “with screen”, and both use content as a service. This means that they have a lot in common in terms of manufacturing, and mobile phone manufacturers’ supply chain base can be well transferred to TV products. The TV’s “big screen” experience cannot be satisfied with a mobile phone’s “small screen”, and entering the TV market can meet the “big screen” defects of mobile phone manufacturers.

Second, the mobile phone brand “de-mobileization” is a major trend in the industry at present. The layout of the entire category has become the standard model. This is not only a proactive change for the brand, but the incoming TV industry can bring additional benefits to the brand. Can increase brand influence; can it be considered as “kidnapping” by the market, do others do it? The cost of trial and error is low, but any brand cannot afford the cost of missing.

Finally, it is the most critical factor. Driven by the IoT home scene, TV products exist as “hubs” in the era of smart homes, and their imagination space is infinitely enlarged. Mobile phone brands that have mastered the initiative of “small screens”, and then gained the dominance of “big screens”, will realize dual-screen linkage and interoperability, taking the lead in the IoT battle.

Based on the above reasons, mobile phone brands are either “voluntary” or “forced”. In short, they have entered the venue, but the question comes again. Is TV good?

02 Betting on the TV market, what makes a mobile phone brand?

According to market data, at least at this stage, “TV” is really difficult to do. The shrinking market, coupled with the crowded environment, fortunately, the door of the market has not been completely closed, and there is still room for a drill.

1. Although the market is dense, there is no oligarch

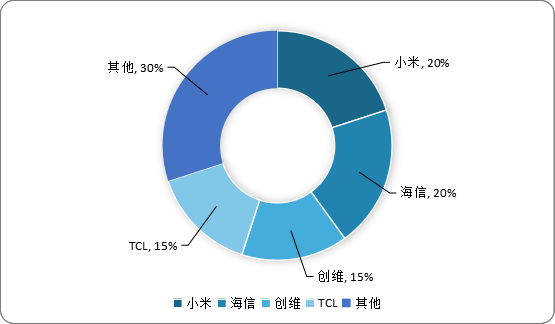

In terms of brand share, the color TV market is more “average” than other categories. Hisense and Xiaomi account for about 20% of the domestic market, while Skyworth and TCL share about 15%. The rest are 30%Divided by other brands.

Compared with Haier’s share of more than 25% in the refrigerator and washing machine markets, Gree’s over 30% in the air-conditioning field, and the “oligarch” in the color TV market has not yet appeared.

Xiaomi’s success in “grabbing the first echelon” is due to its early layout. Xiaomi already entered the TV market in 2013. On the other hand, it shows that the market has a high acceptance of non-traditional TV brands.

Mobile brands such as Huawei, Xiaomi, OPPO have gained market recognition in the technology field. At least their related TV products will not be questioned because of “cross-border”. For example, the Skyworth boss invested in car construction. Maybe you want to be unreliable? But mobile phone brands do not have such concerns in TV.

2. The rise of new categories, “OQ” has new opponents

The TV industry in “忐忑” is not entirely without good news. For example, during the epidemic, offline sales have fallen sharply, but due to the large-scale return of users to the living room, online sales in the 9th week of 2020 have increased year-on-year. It was 16.03%, and color TV was the only one of all categories of household appliances that did not fall but rose during this period.

And there is a single category that has suddenly become popular, that is, “laser TV”. According to data from Zhongyikang on March 2-8, 2020, the retail volume of laser TV online has increased by 211.25% year-on-year. many.

Compared with traditional LED TVs, laser TVs have several characteristics: First, the price of LED TVs tends to increase geometrically with the screen size, and laser TVs are more cost-effective; Second, laser TVs use diffuse reflection imaging. It is more user-friendly for user glasses. Third, laser TVs are more energy efficient, and products of the same size consume only 1/3 of the power of laser TVs at the same time. And laser TV and smart phone operation are similar, which is also an advantage for mobile phone brands.

It is reported that some mobile phone brands have set their sights on this field. After all, compared with LED TVs, lasersTVs are just getting started. Although brands like Hisense have already launched related products, it is clear that there is more room for mobile phone brands in this area.

3. Can the user base bring into the TV market?

The biggest advantage of a mobile phone brand is its huge user base. When the “single screen” demand is increasingly unable to meet users, the importance of the “second screen” is highlighted.

A question arises here: Can the two screens interact well? And this has become an important consideration for users when purchasing smart products. It is also based on this. It can be seen that at present, major consumer electronics brands are using the “open ecology” layout on the IoT track, and open their doors to welcome everyone. In particular, the linkage with mobile phone brands is very active.

However, if the mobile phone brand inherently occupies the “mobile phone” category, it can “make friends”, but it is not so necessary. The word “full category” is more appropriate for mobile phone brands. All they have to do It is much less difficult to figure out how to transfer mobile phone users to home appliances.

In general, with Xiaomi and Huawei as their representatives, mobile phone brands have gradually made their way in the TV market. Of course, traditional TV brands will certainly not sit still. It is foreseeable that there will still be competition in the industry.

03 Same way, different moves

Although mobile phone brands have chosen to start from TV on the road from “small screen” to “big screen”, there are also some differences in the gameplay between brands.

For Xiaomi, who entered the market the first time, they followed a similar path to traditional TV brands, and their supply chain was not much different from traditional TV brands. The panels were supplied by LG, Samsung, and Huaxing Optoelectronics. The chips were supplied by Jingchen. Shares are provided, and Jing Chen is also a supplier of TCL and Skyworth, and in terms of sales, Xiaomi TV products have also continued the “cost-effective” consistent line.

Although Huawei produces TVs, Huawei’s positioning is not “TV”, just like Yu Chengdong once said that “Huawei will not make traditional TV products.” It is also “unique” in the title. At present, Huawei ’s “TV products” are named “smart screens”, but in fact, they are smart TVs. At least they have not changed much from other smart TVs in terms of functions and operations.

In terms of supply chain, the most different are the chips. Huawei’s smart screen products are the three self-developed chips, namely Kirin AI chip, Hongye smart display chip and Lingxiao WiFi chip. This is also the advantage of Huawei. After experiencing the “U.S. Government Incident”, Huawei deeply realized the importance of mastering core technologies in its own hands, and its self-developed capabilities have enabled Huawei to have vertical integration capabilities from terminals to accessories, which is a capability that other mobile phone brands do not have. .

And OnePlus’s routine in the e-commerce market is the same as that of mobile phones. They all adopt the “curve to save the country” method, that is, they start from overseas markets. Last septemberCanada has launched its own TV products OnePlus TV Q1 and OnePlus TV Q1 Pro in India, but has been slow to launch in China.

According to Liu Zuohu, the founder and CEO of OnePlus, last year, OnePlus TV will try to release it in China in 2020, but only for it. No other information is available. Excluding some problems in hardware and software, the delay in failing to go public in China may be due to two reasons.

First, the market environment. In addition to the traditional domestic appliance brands and cross-border brands, the competition in the domestic market also includes competition from overseas brands such as Samsung, LG, and Sony. OnePlus is not “good at” marketing, such as For a long time, Chinese people did n’t know how “beautiful” OnePlus ’s mobile phone is in the overseas market, so it is also positioned in the high-end market, but OnePlus TV has no advantage in branding, even at a disadvantage.

Second is the price. Because it is positioned in the high-end market, the price of OnePlus TV is not close to the people. The selling prices of the two 55-inch products in the Indian market are Rs 699,000 and Rs 99,900, which are about 7,000 yuan and 10,000 yuan. Yuan, and this price range in China can buy up to 75 inches of products. Based on these two points, OnePlus TV still lacks competitiveness in the domestic market.

Anyway, black cats and white cats are good cats if they can catch mice. The differentiation model of mobile phone brands in the TV market may show more diversification as more brands enter. The increasing number of “cross-border” players will make the water in the TV market clearer or more turbid. I believe it won’t take long to be clear.

Summary

Finally, can the entry of mobile phone brands bring new changes to the TV industry? “Intelligence theory” believes that it may be reflected in two aspects.

First, as mobile phone brands invest in high-end and new-type products, while stimulating the “catfish effect”, they may activate bottomed product prices. After all, judging by the current price of mobile phone brand TV products, low.

Second, the way in which smartphones are played may change users ’inherent perceptions of TV products. Some analysts made a comparison. One of the latest iphone11pro can buy 8 TVs. Of course, you can buy them, but the lowest TV price is the extreme price of the highest mobile phone. Judging from the average market price of 2,809 yuan in 2019, one iphone11pro can still “switch” to 2-4 TVs. However, in terms of redemption rates, mobile phone products are 2-3 years, and TVs are 5-10 years or even longer.

Whether mobile phone brands can change the frequency of TV product replacement through channel and marketing capabilities is worth looking forward to.

According to market data, at least at this stage, “TV” is really difficult to do. The shrinking market, coupled with the crowded environment, fortunately, the door of the market has not been completely closed, and there is still room for a drill.

1. Although the market is dense, there is no oligarch

In terms of brand share, the color TV market is more “average” than other categories. Hisense and Xiaomi account for about 20% of the domestic market, while Skyworth and TCL share about 15%. The rest are 30%Divided by other brands.

Compared with Haier’s share of more than 25% in the refrigerator and washing machine markets, Gree’s over 30% in the air-conditioning field, and the “oligarch” in the color TV market has not yet appeared.

Xiaomi’s success in “grabbing the first echelon” is due to its early layout. Xiaomi already entered the TV market in 2013. On the other hand, it shows that the market has a high acceptance of non-traditional TV brands.

Mobile brands such as Huawei, Xiaomi, OPPO have gained market recognition in the technology field. At least their related TV products will not be questioned because of “cross-border”. For example, the Skyworth boss invested in car construction. Maybe you want to be unreliable? But mobile phone brands do not have such concerns in TV.

2. The rise of new categories, “OQ” has new opponents

The TV industry in “忐忑” is not entirely without good news. For example, during the epidemic, offline sales have fallen sharply, but due to the large-scale return of users to the living room, online sales in the 9th week of 2020 have increased year-on-year. It was 16.03%, and color TV was the only one of all categories of household appliances that did not fall but rose during this period.

And there is a single category that has suddenly become popular, that is, “laser TV”. According to data from Zhongyikang on March 2-8, 2020, the retail volume of laser TV online has increased by 211.25% year-on-year. many.

Compared with traditional LED TVs, laser TVs have several characteristics: First, the price of LED TVs tends to increase geometrically with the screen size, and laser TVs are more cost-effective; Second, laser TVs use diffuse reflection imaging. It is more user-friendly for user glasses. Third, laser TVs are more energy efficient, and products of the same size consume only 1/3 of the power of laser TVs at the same time. And laser TV and smart phone operation are similar, which is also an advantage for mobile phone brands.

It is reported that some mobile phone brands have set their sights on this field. After all, compared with LED TVs, lasersTVs are just getting started. Although brands like Hisense have already launched related products, it is clear that there is more room for mobile phone brands in this area.

3. Can the user base bring into the TV market?

The biggest advantage of a mobile phone brand is its huge user base. When the “single screen” demand is increasingly unable to meet users, the importance of the “second screen” is highlighted.

A question arises here: Can the two screens interact well? And this has become an important consideration for users when purchasing smart products. It is also based on this. It can be seen that at present, major consumer electronics brands are using the “open ecology” layout on the IoT track, and open their doors to welcome everyone. In particular, the linkage with mobile phone brands is very active.

However, if the mobile phone brand inherently occupies the “mobile phone” category, it can “make friends”, but it is not so necessary. The word “full category” is more appropriate for mobile phone brands. All they have to do It is much less difficult to figure out how to transfer mobile phone users to home appliances.

In general, with Xiaomi and Huawei as their representatives, mobile phone brands have gradually made their way in the TV market. Of course, traditional TV brands will certainly not sit still. It is foreseeable that there will still be competition in the industry.

03 Same way, different moves

Although mobile phone brands have chosen to start from TV on the road from “small screen” to “big screen”, there are also some differences in the gameplay between brands.

For Xiaomi, who entered the market the first time, they followed a similar path to traditional TV brands, and their supply chain was not much different from traditional TV brands. The panels were supplied by LG, Samsung, and Huaxing Optoelectronics. The chips were supplied by Jingchen. Shares are provided, and Jing Chen is also a supplier of TCL and Skyworth, and in terms of sales, Xiaomi TV products have also continued the “cost-effective” consistent line.

Although Huawei produces TVs, Huawei’s positioning is not “TV”, just like Yu Chengdong once said that “Huawei will not make traditional TV products.” It is also “unique” in the title. At present, Huawei ’s “TV products” are named “smart screens”, but in fact, they are smart TVs. At least they have not changed much from other smart TVs in terms of functions and operations.

In terms of supply chain, the most different are the chips. Huawei’s smart screen products are the three self-developed chips, namely Kirin AI chip, Hongye smart display chip and Lingxiao WiFi chip. This is also the advantage of Huawei. After experiencing the “U.S. Government Incident”, Huawei deeply realized the importance of mastering core technologies in its own hands, and its self-developed capabilities have enabled Huawei to have vertical integration capabilities from terminals to accessories, which is a capability that other mobile phone brands do not have. .

And OnePlus’s routine in the e-commerce market is the same as that of mobile phones. They all adopt the “curve to save the country” method, that is, they start from overseas markets. Last septemberCanada has launched its own TV products OnePlus TV Q1 and OnePlus TV Q1 Pro in India, but has been slow to launch in China.

According to Liu Zuohu, the founder and CEO of OnePlus, last year, OnePlus TV will try to release it in China in 2020, but only for it. No other information is available. Excluding some problems in hardware and software, the delay in failing to go public in China may be due to two reasons.

First, the market environment. In addition to the traditional domestic appliance brands and cross-border brands, the competition in the domestic market also includes competition from overseas brands such as Samsung, LG, and Sony. OnePlus is not “good at” marketing, such as For a long time, Chinese people did n’t know how “beautiful” OnePlus ’s mobile phone is in the overseas market, so it is also positioned in the high-end market, but OnePlus TV has no advantage in branding, even at a disadvantage.

Second is the price. Because it is positioned in the high-end market, the price of OnePlus TV is not close to the people. The selling prices of the two 55-inch products in the Indian market are Rs 699,000 and Rs 99,900, which are about 7,000 yuan and 10,000 yuan. Yuan, and this price range in China can buy up to 75 inches of products. Based on these two points, OnePlus TV still lacks competitiveness in the domestic market.

Anyway, black cats and white cats are good cats if they can catch mice. The differentiation model of mobile phone brands in the TV market may show more diversification as more brands enter. The increasing number of “cross-border” players will make the water in the TV market clearer or more turbid. I believe it won’t take long to be clear.

Summary

Finally, can the entry of mobile phone brands bring new changes to the TV industry? “Intelligence theory” believes that it may be reflected in two aspects.

First, as mobile phone brands invest in high-end and new-type products, while stimulating the “catfish effect”, they may activate bottomed product prices. After all, judging by the current price of mobile phone brand TV products, low.

Second, the way in which smartphones are played may change users ’inherent perceptions of TV products. Some analysts made a comparison. One of the latest iphone11pro can buy 8 TVs. Of course, you can buy them, but the lowest TV price is the extreme price of the highest mobile phone. Judging from the average market price of 2,809 yuan in 2019, one iphone11pro can still “switch” to 2-4 TVs. However, in terms of redemption rates, mobile phone products are 2-3 years, and TVs are 5-10 years or even longer.

Whether mobile phone brands can change the frequency of TV product replacement through channel and marketing capabilities is worth looking forward to.