The construction of a smart ecosystem is an important strategic direction for the bank’s new round of digital transformation. It is based on the open integration of banks and the development of new technologies.

Editor’s note: href=”https://mp.weixin.qq.com/s/hsZRJD0B6VJVZ1IdB01mpQ”> “light financial” (ID: Qjinrong) This article from the micro-channel public number , Author: Li Jing flaw .

“Technology is the only power that can subvert the business model of banks”. In the annual report / public occasion, the presidents of the two joint stock banks of China Merchants Bank and Shanghai Pudong Development Bank all expressed This same view.

The emergence of new technologies has given a new breakthrough path to the development model of traditional banks. However, if a bank still stays in a passive and moderate fintech innovation, but lacks reform innovation and destructive creation, it will inevitably be ahead of Peer farther away.

So we saw that on the one hand, more and more banks are increasing their investment in fintech year by year, and strengthening the reserve and training of fintech talent; on the other hand, banks are exploring the integration of technology and financial business, and building basic technology platforms , Open and integrated ecological promotion, institutional and institutional cultural transformation, etc., is the real battlefield of bank financial technology.

What is the latest layout of financial technology by banks? Through interviews, investigations and annual report retribution, Light Finance fully presented the financial technology layout of banks.

First, Fintech Strategy and the latest layout

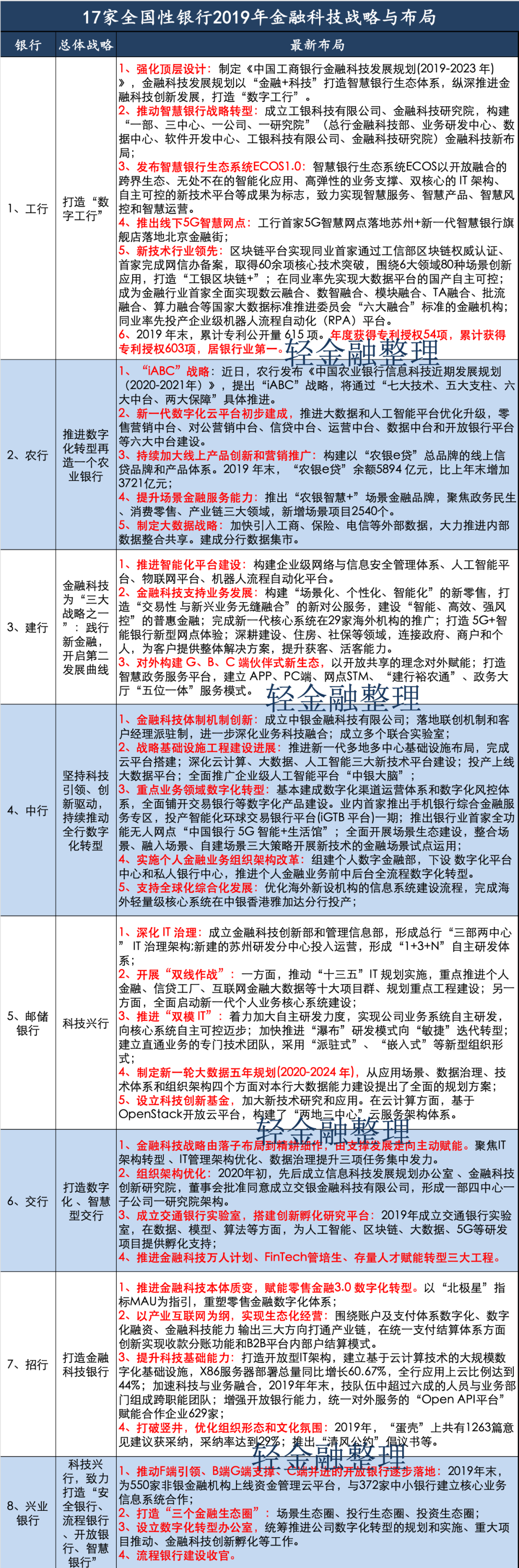

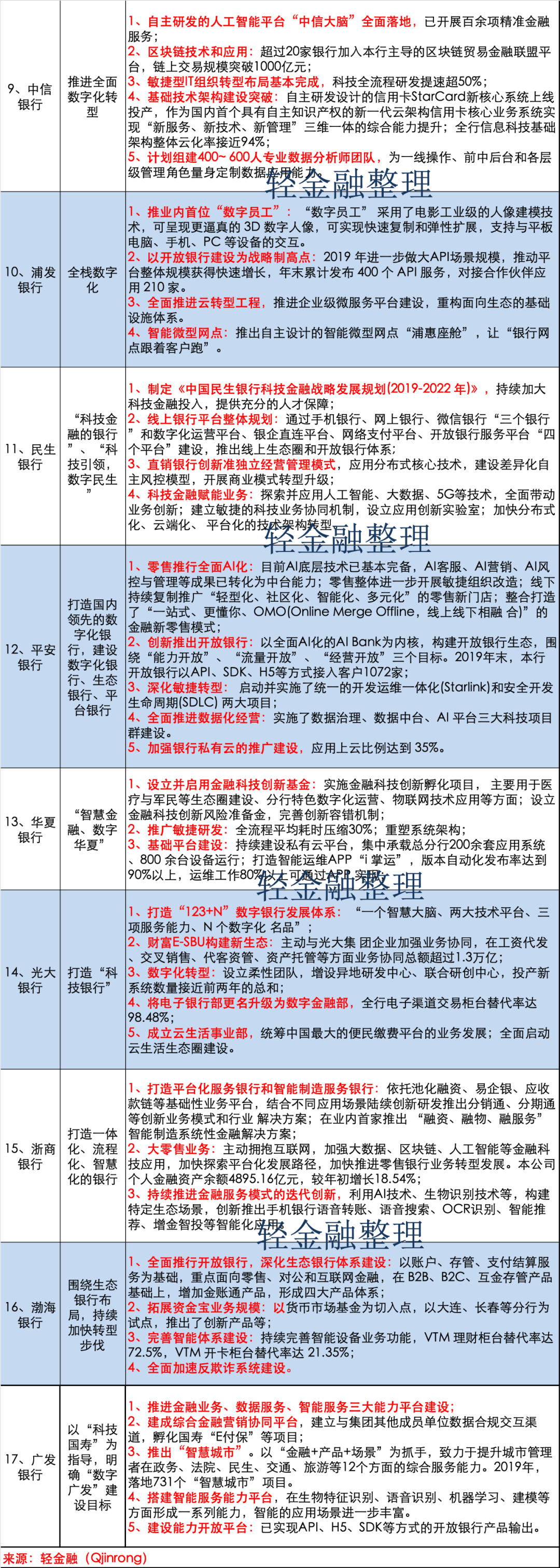

First of all, to look at the most important content in this article, we have compiled the latest fintech strategies and layout of 17 national banks (including 6 state-owned banks and 11 stock banks).

1. Fintech reform innovation

In the past year, the bank ’s strategy for fintech has become clearer and clearer.As the saying goes, “The fintech strategy has shifted from layman to intensive cultivation, and from supporting development to active empowerment.” One of the outstanding features of the bank’s fintech active empowerment is the accelerated integration of fintech and business.

For example, Cosmos Bank has implemented several major projects in 2019. Chairman Chen Siqing called it “three major events”: one is the establishment of a technology subsidiary ICBC Technology in Xiong’an, and the other is the establishment of a financial technology research institute. The third is to launch the smart banking ecosystem ECOS1.0.

China Merchants Bank is looking for a qualitative change in financial technology, promoting the transformation of retail 3.0, and building a new model of online user acquisition and management. The monthly active users (MAU) of the two major apps exceeded 100 million, becoming the main platform for customer operation.

2. Organizational structure adjustment

For banks to break through the constraints of traditional mechanisms, the organizational structure adjustment must keep up.

In early 2020, Bank of Communications established the Information Technology Development Planning Office, the Fintech Innovation Research Institute, and the Fintech subsidiary. Prior to this, the bank also transformed the Information Technology Management Department into the Financial Technology Department, forming a new pattern of “one four centers, one subsidiary, one research institute” (financial technology department, data center, test center, software development center, data management And Application Center, Bank of Communications Jinke, Fintech Innovation Institute).

At the end of December last year, China Merchants Bank changed the strategic planning and execution department of the former head office into a “financial technology office”, and split the original R & D center of the Information Technology Department into four R & D centers. It can be seen that the structural change of China Merchants Bank has the overall planning role of the financial technology office on the top floor, while the fission of the R & D center is more accurately connected to each business line.

After the establishment of the Financial Technology Research Institute in November last year, ICBC completed the “One, Three Centers, One Company, and One Research Institute” (Headquarters Financial Technology Department, Business R & D Center, Data Center, Software Development Center, ICBC Technology Co., Ltd., Fintech Research Institute) the construction of a new financial technology structure. This organizational change has more powerful and agile support for the transformation of smart banks.

The changes in the financial technology structure of banks are to better adapt to the rapidly changing future of new technologies.

3 , Zhongtai Construction Speed up

Increase the capacity building of banks in China and Taiwan has become the consensus of the banking industry.

In the big bank, Agricultural Bank of China put forward the “iABC” strategy, “thin front desk, thick middle platform, strongThe “backstage” IT architecture system promotes the construction of six central platforms, including retail marketing central office, corporate marketing central office, credit central office, operating central office, data central office and open banking platform.

In the personal financial digital service, CCB also proposes to synchronously promote the capacity building of the business platform that supports digital operations; BOC proposes to adhere to “smart priority”, build an intensive platform, and promote the implementation of multiple products such as smart accounts; Bank of Communications promotes the market Construction of a risky central Taiwan system; the Postal Savings Bank has also achieved the same data and the same caliber, as well as unified processing and shared use, to lay the foundation for the further evolution of the data central office.

China Merchants Bank is also working hard to improve the capabilities of the China Merchants Group, building an open architecture, agile and iterative system mezzanine. “We expect to establish a mezzanine empowerment front desk and front desk feedback to promote the loop of the mid-stage iteration and promote the self-evolution of China Merchants Bank organization. China Merchants Bank said in its 2019 annual report.

Ping An Bank regards data center as one of the key implementation of the construction of the three major technology project groups, and accelerates the construction of the data index platform, data service platform, and the “five databases” of customers, products, personnel, channels, and cases. In addition, the bank has 11 AI projects in Taiwan that have all been put into production.

With the advent of the bank 4.0 era of “financial services will be ubiquitous”, the capacity building of banks in the middle office will not be limited to the establishment of a system, but will focus on the agility of the entire organizational structure of the bank and the overall ecology. Way of thinking.

As the banking industry has increased the construction of China and Taiwan, on the one hand, it helps to break the previous situation where the efficiency of the bank ’s front desk and back office are not equal, and accelerates the agile response of the entire organization; Comply with rapid changes in customer-centric needs. In the future, the creation of modular, “Lego” agile capabilities will become a major trend.

4. Open and integrated ecological battle

The construction of a smart ecosystem is an important strategic direction for the bank ’s new round of digital transformation, which is based on the bank ’s open integration and the development of new technologies.

To establish an ecology, a bank must first find “Where is the customer”, build an ecology around customer needs, and drive the new ecology with new technologies. This is the current ecological construction approach explored by banks, including the 2B2C2G model.

For example, ICBC has opened more than 1,000 financial services to more than 2,000 ecological partners through open platform API and financial ecological cloud through two ways of “going out” and “introducing”; CCB proposes to build G and B externally , C-end partner-style new ecology, externally empowered with the concept of open and shared; whether it is retail, business and other businesses, China Merchants Bank has put forward the development of ecological management ideas.

Therefore, it is foreseeable that the battle of digital transformation of banks is bound to be a battle of ecological construction. Who can go deeper into the field