Establishment of dollar hegemony

The comprehensive economic strength of the United States and the improvement of economic and financial openness, the Fed is actively acting, financial innovation and financial institutions overseas The establishment of branches has played an important role.

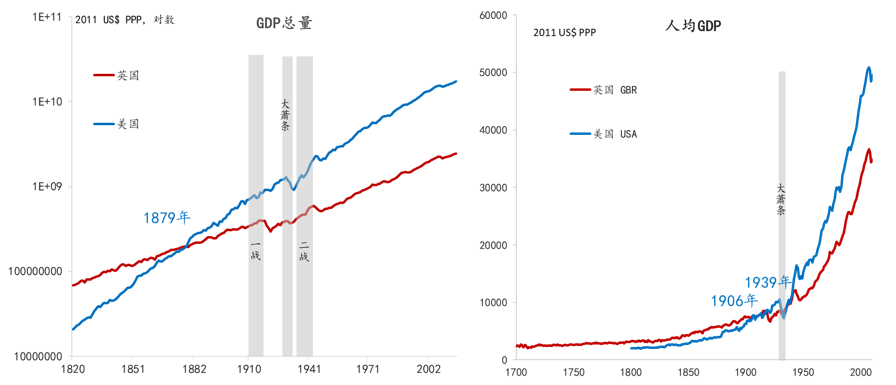

According to Madison’s data, the total GDP of the United States surpassed that of the United Kingdom in 1879, and the per capita GDP exceeded the United Kingdom for the first time in 1906 (Figure 1 ). For the first time, the US dollar surpassed the British pound in foreign exchange reserves. It would have to wait until 1925. Among them, from 1914 to 1925, it can be regarded as a transition period (Eken Green, 2011). Counting from 1879, it took nearly half a century for the US dollar to achieve a certain dominant position. From the perspective of historical experience and the strong externality of international currencies, the overtaking of comprehensive economic power, the complexity of capital and trading networks, and their favorable position in the global value chain or the necessary conditions for the establishment of monetary power.

Figure 1: Comparison of British and American economic strength

Data source: Madison, Oriental Securities; the total GDP is GDP per capita multiplied by the total population.

Using the analogy method, Ekengreen believes that since the 1980s, the US trade deficit and fiscal deficit have been expanding, which is in line with the United Kingdom. The situation before the war was very similar. At the same time, in different periods after World War II, the United States also facesSince the competition of Japan, EU and China, its share in the world economy and trade has also been declining. In addition, China’s efforts to build a financial center in Shanghai are similar to the Fed’s establishment of a trade acceptance bill market in New York in the 1920s, all of which have helped increase the internationalization of the currency. Over the past 10 years, China has made remarkable achievements in promoting the internationalization of the RMB. The RMB has played an increasingly prominent role in trade settlement, foreign exchange reserves, and units of valuation.

Before World War I, the overall economic strength of the United States surpassed that of the United Kingdom, but the pound was still the most important international currency at that time, and London’s status as an international financial center far exceeded that of New York. It is due to the existence of the “locking effect” of international currencies. This mismatch between economic and financial patterns is accompanied by global economic imbalances and financial market shocks (de Cecco, 1984). The famous financial historian Jindelberg believed that the Great Depression began with the world economy’s high dependence on the British pound and London, and its contradiction with the lack of British conditions for maintaining the excellent status of British pounds and London. As the UK’s share of the world economy has declined, its ability to maintain global financial stability and the status of the British pound has also declined. In this way, the only thing that triggered the switch of the world’s monetary system is the British mistake, and the United States seized the opportunity to do something right. This historic opportunity is the two world wars.

Compared to what the US is most right about, what’s more important is what the UK is doing wrong. During the period from the establishment of the gold standard in 1717 to before World War I, whenever a war was encountered, the British government’s fiscal deficit widened, demand for bond financing rose, and interest rates rose. In order to ensure the smooth issuance of government bonds, common measures include adding new taxes, restricting the issuance of commercial bonds, limiting capital outflows, and closing the gold exchange window. To reduce the issuance rate, the British government may pressure the Bank of England, for example, to issue Treasury bonds at a lower agreed interest rate, or the Bank of England may purchase a share of the market that cannot be digested. This is essentially “fiscal monetization”, which will weaken the credibility of the pound. However, on the one hand, the UK will win the war most of the time; on the other hand, after the war, the UK will return to the gold standard at the original price and take measures to repay the debts accumulated during the war; thus making the British pound and the British national debt in a longer period of time Maintain the highest credibility. In addition, the reason I have to mention is that the currency that can replace the British pound has been missing for a long time. The Franc and the German mark are strong competitors, but they are still more limited to the European continent and its overseas colonies.

From the Napoleonic Wars to the eve of World War I, the balance of British national debt decreased from 830 million pounds to 700 million pounds, but this trend followed the outbreak of World War I Completely reverse. British military expenditure in World War I was as high as 7.5 billion pounds, equivalent to 19138 times the fiscal expenditure in 3 years. In 1919 after the end of World War I, the balance of outstanding national debt as a percentage of GDP rose from 28% in 1914 to 128%.

In the early days of World War I, Britain believed that the war would end soon, on the grounds of deepening economic interdependence and the destructive nature of full-scale war. Therefore, the United Kingdom still continues its traditional thinking, with the premise of restoring the gold standard after the war to maintain economic openness. After the outbreak of war, European capital stopped flowing, and banks began to recover liquidity, which led to the lack of liquidity in the British financial market and the real economy began to shrink. In order to ease the pressure of capital outflow, the Bank of England increased the discount rate from 3% to 10% within a month, but this in turn increased the domestic deflationary pressure. Therefore, the implementation of the “Peel Regulation” was suspended and the Bank of England was allowed to issue negotiable bonds. And bank notes that exceed the legal limit. At the same time, the Bank of England also financed the war through direct purchase of national debt. The United States banned the outflow of gold as early as September 1917, while the United Kingdom “boiled” until March 1919. As early as 1915, the pressure to maintain the stability of the sterling exchange rate has been highlighted, but as Keynes discussed, “If there is a sign of emergency that stops paying gold, the status of the City of London will be severely hit.” Ways to hedge the pressure of capital outflows and pay war costs have triggered post-war inflation, making it more difficult for Britain to restore the gold standard at the original price in 1925. Keynes later changed his mind, calling this kind of gold worship in Britain “the remains of a barbaric era.”

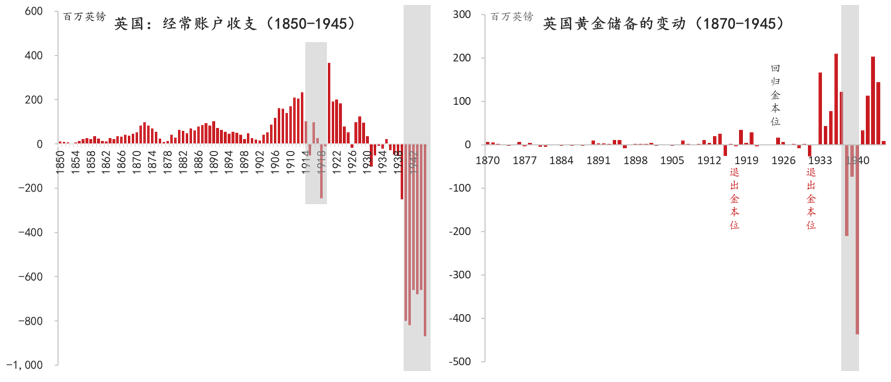

Britain’s current account surplus balance of payments pattern has been broken during World War I since 1850. In 1915, the UK experienced a deficit for the first time (£50 million), which expanded to 250 million in 1918 (Figure 2, left panel). After the restoration of the gold standard in 1925, there was another deficit in 1926, the deficit expanded to 100 million pounds in 1931, the United Kingdom withdrew from the gold standard again, and only then achieved a surplus in 1935. From 1936 to the end of World War II, the British current account continued to deficit, 1945 The year is close to 900 million pounds. The trade deficit coincided with the reduction of gold reserves. British gold reserves decreased significantly during (or before) the two world wars, especially from 1938 to 1940 (Figure 2, right picture).

Figure 2: UK current account income and expenditure and changes in gold reserves

Data source: NBER Macrohistory data, Oriental Securities

The combination of the British macroeconomic account in the two world wars is: fiscal deficit + current account deficit + gold outflow + currency investment. For the credibility of the British pound and British government bonds, it can be described as the “worst combination.”

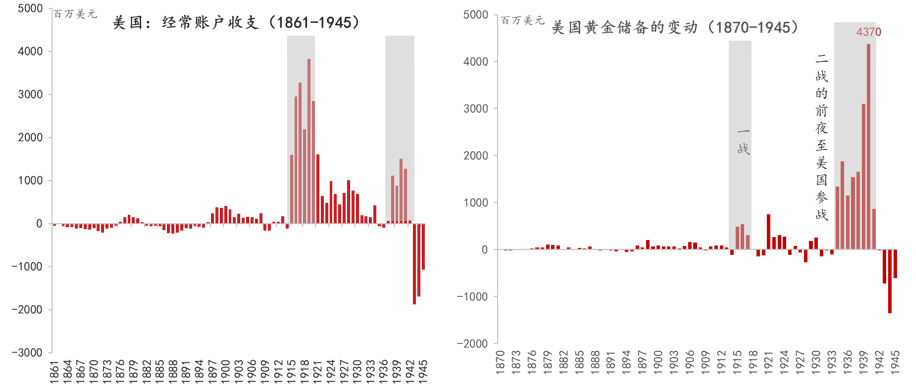

The subtlety is the time difference between war and peace. Staying away from the battlefield and being involved in the war later made the United States the world’s largest trade surplus and creditor country in this “extreme age” and the country with the most abundant gold reserves, which laid the dollar’s “arrogant privilege” The basics. From 1861-1914, the current account of the United States basically maintained a balance, with a smaller surplus or deficit. From 1915 to 1942, the United States achieved a trade surplus for 28 consecutive years (Figure 3, left panel), and therefore accumulated a large amount of foreign exchange reserves, including gold reserves (Figure 3, Picture on the right). In 1934, the U.S. currency gold reserves began to increase significantly, which was closely related to the changes that Hitler took to power in 1933 and brought about changes in the situation in Europe. In the eight years from 1934 to 1941, the U.S. gold reserves increased by a total of 16 billion US dollars, an average annual increase of 2 billion. Among them, in the early years of World War II, 1939 and 1940 increased by 3.1 billion and 4.4 billion US dollars, respectively. It was precisely because World War II spurred demand that the United States got rid of the Great Depression. After the end of World War II, the United Kingdom made many compromises in the Bretton Woods system by virtue of the “lease terms”, and the international economic and trade pattern based on the “gold-dollar” system was established.

Figure 3: US current account income and expenditure and changes in gold reserves

Data source: NBER Macro Historydata,Oriental Securities

Two world wars changed the way the British government financed and paid off since the 19th century. Tomita Toki summarized it in “History of National Debt” as 6 points:

First, in addition to the haircut of Treasury bills and loans from the central bank, hair notes were also issued;

Second, the frequency of Treasury bill issuance has increased, and the method of price competition bidding has been changed to the government setting interest rate;

Third, the issuance of medium-term bonds of 3-10 years;

Fourth, when issuing long-term government bonds, the conditions are more favorable to investors, such as interest tax reductions, etc.;< br>

Fifth, promote individual investors to purchase government bonds;

Sixth, start issuing in US dollars, Japanese yen, etc. Treasury bonds issued in foreign currencies.

These reflect the increasing demand for British government financing from different aspects. Among them, the first point makes the boundary between finance and currency more and more blurred.

Independence of the Fed

The US economy, military and gold reserves are undoubtedly all It is the basis for establishing the credibility of the US dollar and federal government bonds, but another detail that is often overlooked is the independence of the Fed. This may be regarded as a “cold joke” in the current context, because there is a view that the Fed’s decision has been affected by Trump and is to “save the market” for Trump, so it has a certain political color. .

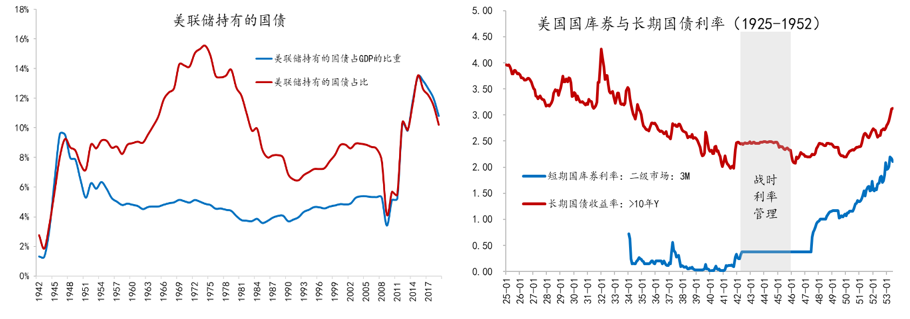

Actually, the Fed’s purchase of government bonds can be traced back to the Great Depression. The Banking Act of 1932 authorizes the Fed to purchase Treasury bonds in the secondary market and use it as the basis for currency issuance. This is the legal basis for quantitative easing. After the United States participated in World War II, the fiscal deficit continued to expand, reaching 15% and 30% in 1942 and 1943, respectively, and fell slightly to 22% in 1944-1945. The proportion of national debt balance in GDP rose from 43% in 1941 to 1946. 120%. During this period, the balance and proportion of Treasury bonds held by the Federal Reserve also increased significantly (Figure 4, left panel). But from the FedDid not purchase government bonds in the primary market. Of course, the Fed does have the possibility of suppressing long-term interest rates and supporting the price of government bonds. From 1941 to 1951, the US 5-year Treasury bond rate never exceeded 2.5% (Figure 4, right panel), which is considered to be the result of the Treasury’s pressure on the Federal Reserve because of the wartime government It needs financing, and after the war, it needs to repay the principal and interest of debt accumulated during the war through low interest renewal. But Tomita believes that although the Fed’s fixing of the Treasury bill rate at 3.75% has an impact on the formation of the national debt rate, the Fed’s policy of supporting the price of government bonds is not sustainable, so this explanation is not convincing.

Figure 4: Federal Government debt and wartime interest rate policy held by the Federal Reserve

Data source: FRB; NBER Macro History data; CEIC; Oriental Securities

After World War II, the United States actually entered another war, not only the Cold War with the Soviet Union, but also the Korean War and the Vietnam War. Beginning in late 1949, long-term government bond interest rates began to rise. Then, in June 1950, the Korean War broke out. On September 15, MacArthur landed in Incheon. The US government expects the fiscal deficit to increase, thereby advocating the maintenance of long-term government debt interest rate ceilings. President Truman also wrote to Thomas McCabe, then chairman of the Federal Reserve, stating that “the lifting of fixed interest rates is exactly what Stalin expected.” The Fed immediately increased its holdings of national debt. At the FOMC meeting in January 1951, the Aix board member said, “If the Federal Bank buys Treasury bonds in response to the call to fix interest rates on Treasury bonds, the Fed will become the engine of inflation.” Obviously, the Fed and the President’s Opinions conflicted. A week later, Truman attended the FOMC meeting unprecedentedly, noting that the form the United States was facing was even more severe than World War II, and pointed out that “if the nationals lose trust in the national debt, then the situation will be very dangerous” (Toda Junji, 2015) , Require the Fed to maintain the stability of the national debt market. The response of President McCabe is that the interest rate can be fixed according to the president’s request, but he will choose to resign.Compared with the way that the President requires to maintain the price of Treasury bonds through the purchase of Treasury bonds, the Fed has taken a different approach and removed itself from the obligation to maintain Treasury bonds. At the FOMC meeting on March 3, 1951, McCabe and Treasury Secretary Snyder issued a joint statement: The Ministry of Finance and the Commonwealth Bank fully reached a consensus that they should further improve the national debt management policy and financial policy so that the government Successfully allocated funds and achieved the common goal of minimum monetization of debt. Long-term Treasury interest rates rose to more than 2.5%, and the market believes that the Fed is freed from its responsibility to support the price of Treasury bonds. Tomita Junki believes that the day of the agreement can be regarded as the “independence day” of the Fed. After the agreement was published, the Fed limited its open market intervention to treasury bills, which is significantly different from wartime government debt management policies. Obviously, after the 2008 crisis, the Fed may have forgotten the “Declaration of Independence.”

Strengthening the hegemony of the dollar

Historically, the “special moments” that required the Fed to manage the national debt were mostly wars, which turned into a financial crisis after World War II . Over the past half century, the frequency of crises has become higher and higher, but the risk of inflation has become lower and lower. Under this background, post-Keynesian economists have proposed modern monetary theory. In short, when interest rates fall On the premise that zero-sum does not cause inflation, the fiscal deficit can be monetized, that is, the central bank can finance the fiscal deficit by issuing paper money and buying treasury bonds in the primary market. The government then adopts a series of counter-cyclical policies such as the “last employer plan” Stimulate domestic demand and free the economy from difficulties. We believe that this is a historical retrogression and abuse of power, thereby jeopardizing the credibility of the US dollar and US Treasury bonds.

There is a view that Nixon’s closing of the golden window in 1971 was a breach of contract, but the dollar hegemony has not only been damaged, but has strengthened. It can also be seen that every time a liquidity shock strikes the financial market, the US dollar will become stronger and US debt will be more sought after by investors. Therefore, the US dollar and US debt are regarded as scarce and safe assets. Therefore, the United States has the privilege of printing money and monetizing fiscal deficits. This is like the fact that the United Kingdom also restricted the outflow of gold many times before World War I, and then returned to the gold standard intact. The credibility of the British pound and British government debt did not seem to be affected by this, because the international monetary system would not A “screw” loosens and disintegrates, but in some cases, if multiple screws loosen at the same time, the system will collapse. The two world wars directly led to the switch of the international monetary system, because it formed such a combination for the UK: fiscal deficit + trade deficit + monetary easing + gold outflow + dollar substitution.

It is undeniable that the US dollar will continue to occupy a hegemonic position for a longer period of time, and the hegemonic position of the US dollar is more stable than that of the British pound. This is not only due to the “locking effect” due to a higher degree of globalization “It is also because the structure of the current international monetary system is significantly different from that of the 19th century pound system.

Before the complete collapse of the Bretton Woods system in 1973, “Gold-dollar The “Gold-Pound Sterling” system has a high similarity, although the former is more of an institutional construction, the latter is a spontaneous order. The “Gold-Pound Sterling” system is as follows (Figure 5, left picture< /strong>), it is essentially a gold standard, and the exchange rates of different currencies are set to gold parity. The pound is just a certain “anchor currency” because it plays a greater role in international trade and finance. Role, but its status is significantly lower than that of gold. Once investors are worried about the devaluation of the pound, they will be required to convert it into gold coins. Because of this, during the First World War, the UK’s gold reserves decreased significantly, which directly caused the credibility of the pound to decline.

Figure 5: Changes in the international monetary system

Source: Draw by the author, Eastern Securities

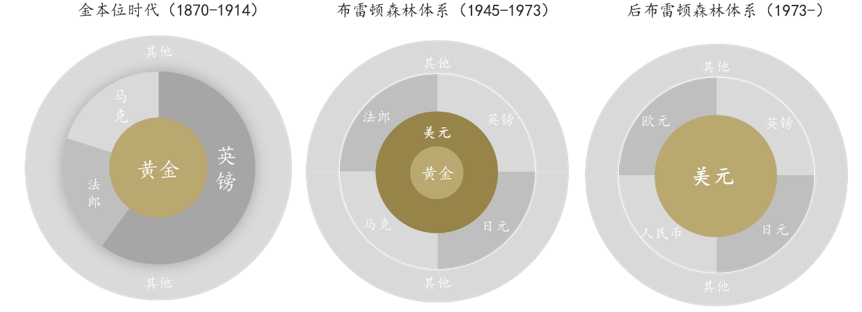

The picture shows Breton The structure of the forest system, the dollar is linked to gold, and other currencies are linked to the dollar, so it is a double-layered nested currency system, which has the meaning of “holding gold to make princes.” The US dollar has largely replaced the monetary attributes of gold. In terms of convertibility with gold, the Bretton Woods system is very similar to the gold standard system. When worried about the depreciation of the US dollar, the US dollar reserve country can exchange it for gold. Before 1964, the supply of gold in South Africa and the former Soviet Union met the market demand, but since 1965, the supply has declined. At the same time, European countries such as France and Italy are disgusted with dollar hegemony, on the other hand, they are also worried about the ability of the United States to maintain the Bretton Woods system. Therefore, they have been increasing their gold holdings, leading to the United States’ gold reserves The rapid passage eventually caused President Nixon to close the golden window in 1971. In 1973, the transitional “Smithson Agreement” lapsed, The Bretton Woods system completely disintegrated.

In the post-Bretton Forest system (Figure 5, right panel), the status of gold’s reserve currency has become a symbol, currency Attributes are lost, no longer play the role of transaction medium and value standard, and the US dollar has become the only “anchor currency”. Although the euro, pound sterling, yen and renminbi are also considered international currencies, they are still in the “periphery” relative to the dollar. As mentioned earlier, the reason why the US dollar can quickly replace the pound as the most important world currency is because in the gold standard system, the credibility of the pound is not only constrained by fiscal discipline, but also by gold reserves. A higher level of substitution. It is precisely because of this substitution of gold, coupled with the passing of British gold reserves and the increase of American gold reserves during the war, that accelerated the replacement of the US dollar with the British pound. However, in the current US dollar-centric international monetary system, there is no such super-sovereign third-party currency to replace the US dollar, which also increases the difficulty of the “locking effect” of the US dollar and the internationalization of the RMB.

The prospects for dollar hegemony

Even so, with the rise of emerging market countries, the US share of the international economy and trade is declining, The share of the US dollar in the international financial market is also constantly being cut.

Since the 1980s, the scale of the US balance of payments deficit and fiscal deficit has continued to expand, showing a trend of further expansion since the 21st century. Despite the strong performance of the US dollar during the turmoil in the financial market and the stable exchange rate of the US dollar, it still plays a leading role in international trade, foreign exchange transactions and international reserves, but its relative advantage is declining. For example, in international reserves, the US dollar has fallen from 70% at the beginning of the century to 60% in 2019. Considering that the monetary and financial systems and the economic and trade pattern must be consistent over a long period of time, we believe that the pattern of “one super, many strong” in the international monetary system will change towards “three-legged”, and the euro and the renminbi will be financial and trade in their respective regions. Play a more important role in China, thereby continuing to divide the dollar’s share. For the renminbi, the premise is to maintain exchange rate stability, which in turn depends on national credit built on fiscal discipline.

It is rumored that the Trump administration’s sloppy idea of hitting the dollar debt held by China will be a departure from the fine tradition of America. In 1789, Washington was elected the first president of the United States, and Hamilton was the first finance minister. In order to pay off the debt owed by the War of Independence, Hamilton announced that the federal government accepts all internal and external debt, andPay at face value. He also said: “Like individuals, the state can only gain trust if it abides by the agreement, otherwise it will have the opposite fate.” Even if it is not to freeze or refuse to pay debts for some reason, but to implement a nominal negative interest rate, it is essentially a kind of beggar The policy of the United States will weaken the credit of the US dollar and US debt. Like the pound sterling before and after World War I, it will inevitably be liquidated by history, but there is still a lack of alternative media.

Although there are countless reasons to support the strong position of the US dollar and US debt, the continued expansion of the US government’s fiscal deficit and the continuous backlog of federal debt have resulted in the loss and independence of the Fed’s independence. The normalization of the quantitative easing policy on the bottom line will weaken the credibility of the US dollar, US debt and the Fed in the long run.

(Author Shao Yu is the chief economist of Dongfang Securities, Chen Dafei is a macro analyst of Dongfang Securities; this article is a comparative study of the history of the world monetary system of major projects of the National Social Science Fund “(18ZDA089)’s staged results.)