Probably the most comprehensive “ten yuan shop” inventory.

Editor’s note: This article is from ” CBNData consumer station “(www.cbndata.com) , author: Zhang Xiao Sha.

On October 15th, the 7-year-old “Ten Yuan Store” brand Miniso was officially listed in the United States, with a market increase of over 20% on the first day.

Just a few days ago, the first “1 yuan store” of Taobao special edition landed. It is reported that Taobao will open at least 1,000 “1 yuan stores” across the country within three years.

The trend of “ten yuan shop” is re-emerged. Is this model really promising?

Actually, it is not only in China, but also in the retail industry around the world that there is a “ten yuan shop” model, and the oldest one is more than half a century. The CBNData consumer station counted the “ten yuan shops” in China, Japan and the United States. Which mode is the best refer-type=”2″ href=”https://36kr.com/projectDetails/62488″ target=”_blank”>There is money to go? After reading this article, you may have your own answer.

(*Note: Due to differences in exchange rates between countries, China’s “ten-yuan store” corresponds to “hundred-yuan store” in Japan and “one-yuan store” in the United States. For ease of description, this article refers to such stores as “ten-yuan stores”. Yuandian”.)

The originator of the “Ten Yen Shop” in Japan: The lowest gross profit margin of the product is only 2%. How did the annual revenue of 30.3 billion yuan come from?

Speaking of “Ten Yuan Store”, we must mention the “originator” of this retail model-Daiso of Japan.

Daiso started in the 1970s. Most of the products in the store are priced at 100 yen (approximately RMB 6), covering skin care cosmetics, snacks, and various daily necessities.

In the beginning, Daiso founder Yano found a business opportunity from mobile vendors selling defective products. After trying, I found that consumers are enthusiastic about buying. In order to facilitate the pricing, Yano adopted a price of “100 yen for all products.” In order to maintain a profit margin of about 30%, Yano will control the purchase price at about 70 yen.

But, cheapIt always gives the impression of “not good products”, and the quality of the products that cost 70 yen is indeed limited. In addition, at that time, the Japanese economy was in an era of increasing prosperity after the war. With consumption upgrades, simple low prices could not attract consumers with ever-increasing demands.

For this reason, Yano made strategic adjustments-without changing the price, increasing the cost and quality of some products, and the gross profit of a small number of products was even compressed to 2%. Use low-margin products to divert traffic, and then through the profit and loss of high- and low-margin products to ensure overall profitability.

Relying on this model, Yano’s grocery business gradually gained a reputation of “good quality and low price”, and began to gradually abolish the mobile stall model, open physical stores, and conduct corporate operations. The company was officially named “Daiso”.

The presence of physical stores means higher operating costs. In order to increase the store entrance rate and achieve more sales, Daiso continues to push new products while expanding its stores to create more freshness for consumers. Its official website shows that Daiso currently has about 70,000 SKUs, and about 800 new products are developed every month.

In order to maximize gross profit, Daiso started to look for cheaper suppliers outside of Japan. After the order quantity continued to expand, Daiso started the OEM manufacturing model. Over 50% of Daiso’s suppliers are from mainland China.

In terms of saving the cost of opening a store, Daiso often acts as a “receiver” for closed stores. Therefore, in Japan, consumers basically do not see the same two Daiso. In terms of location, Daiso really didn’t pay much attention to it-roadside stores, suburban areas, department stores, etc. are all considered.

Daiso’s store property recruitment conditions|Source: Daiso official website

In order to save human capital, Daiso employs a large number of part-time workers. The official website shows that as of February 2020, Daiso has only 402 full-time employees, accounting for 1.8%.

Daiso is very calm about opening up the international market. After years of deliberation, Daiso started to go to sea in 2001, with the first stop in Taiwan, China. According to Daiso’s official website information, as of February 2020, Daiso (excluding THTEEPPY and other branch brands) has 5741 stores in 27 countries and regions around the world, with overseas stores accounting for 39% (2248). Of the domestic stores in Japan, 76% (2646) are self-operated.

Entering overseas markets means more difficult costsControl and warehousing distribution. Daiso has established close ties with local factories. According to Live Japan reports, Daiso has cooperation with more than 1,400 manufacturers and 8,000 factories in 45 countries and regions. In order to cope with the huge inbound and outbound volume, Daiso has built 8 logistics centers in Japan, and about 200 containers are imported to Japan from overseas every day. 15 logistics centers have also been established abroad to coordinate the cargo management of the world’s stores.

According to the data disclosed by the company on March 31, 2019, Daiso’s annual revenue was 475.7 billion yen (equivalent to 30.3 billion yuan).

The countryside surrounds the city, and the US “Ten Yuan Store” has created two Fortune 500 companies

In the United States, there are two “ten dollar store” giants that have squeezed into the world’s top 500-dollar general and dollar tree, which together account for more than 90% of the US “ten dollar store” market share. According to Dollar tree’s 2019 financial report, it has a total of 15,288 stores across the United States and Canada, with annual revenue of 23.6 billion yuan. And Dollar general has 16,278 stores nationwide, with annual revenue of 27.8 billion U.S. dollars.

Relying on the development route of “rural surrounding the city”, these two “ten-yuan stores” and Wal-Mart and other major supermarkets and grocery stores have launched differentiated competition.

Dollar general, which has a history of 81 years so far, is positioning as a “discount store”, targeting Americans with an annual income of less than US$40,000 and living in the so-called “food desert” (far away from grocery stores). The unit price of in-store merchandise is mostly under US$5, and about 22% of the merchandise sells for less than US$1. The “ten dollar store” of dollar tree is more thorough, and the products in the whole store are basically under $1. (*Although the founding year of dollar general and dollar tree is earlier than Daiso Daiso. But the positioning of dollar tree “everything’s $1” only appeared in the 1980s, so we say that the originator of the “ten yuan shop” model is Daiso.) < /p>

Picture source: dollar tree official website

The two “ten yuan stores” have a wealth of goods on sale. Taking dollar general as an example, the commodities on sale are daily necessities, food and beveragesMainly life consumables, and cover seasonal goods, household goods, clothing, etc. The dollar general financial report shows that consumables with the lowest gross profit margin contributed 78% of sales in 2019; household items, seasonal goods, and clothing together contributed 22% of sales, but they have higher gross margins. Relying on small profits but quicker sales of consumables that are frequently purchased, and relying on other products to increase gross profit, Dollar general has achieved same-store sales growth for 30 consecutive years.

Dollar general’s sales of various products accounted for | Source: dollar general’s 2019 financial report

In terms of suppliers, dollar general’s cooperative brands include Coca-Cola, Pepsi, Mars, Nestlé, Kellogg, General Mills, Unilever, Procter & Gamble, etc., but the prices of the products are cheaper than those of supermarkets and pharmacies About 20%-40%.

They are all brand goods, why can the price of “ten yuan shop” be lower?

The first is to effectively reduce costs in selecting locations to open stores. These two “ten yuan stores” are located in rural and suburban areas, the store area is only about 1/10 of Wal-Mart, and the decoration style is also very simple. It is also very stingy in terms of staffing. Most dollar general stores have only 1-2 staff. The senior vice president of store development at dollar general revealed in an interview with The Wall Street Journal in 2017 that the cost of opening a new store was only about $250,000.

The “ten yuan shops” often follow Wal-Mart and other large supermarkets to open stores, and “white prostitutes” have huge passenger flow. According to data from Leju Finance, 54% of Dollar General’s stores are less than 10 minutes away from Wal-Mart by car, and the proportion of dollar tree is as high as 84%.

The smaller size and lower cost of opening stores have enabled the “ten yuan store” to penetrate into wider areas where Wal-Mart and other large supermarkets cannot reach.

In terms of product selection, dollar general strictly controls SKUs and only handles the best-selling products. The limited selection of products and bulk purchases not only reduce the cost of product management, but also win greater bargaining power for dollar general in front of suppliers.

Strictly control SKU, CoStco also relies on this method to reduce the cost of goods. But unlike Costco’s model of mass sales in large packages, the “ten yuan shop” is more inclined to sell low-priced, small-package products, so that the single-piece price is controlled below $5 or even lower. Consumers seem to spend less money to buy the goods they want, but they may actually pay more for a unit of goods. According to the calculations of commercial real estate headlines, the unit prices of some of the dollar tree products are even more than double that of Wal-Mart. This effectively reduces the cost of decision-making for consumers. Data shows that the entire process from entering the store to completing the purchase for dollar general customers often takes less than 10 minutes.

Source: Guangfa Securities; Picture source: Commercial Real Estate Headlines

This sales model may also conform to the reality of the sinking market to a certain extent. After all, not all consumers have enough budget to buy the same product in bulk. It may be more realistic to spend the same money to buy all kinds of goods you need right now.

The expanding business landscape of the “ten yuan shop” has also allowed big brands such as P&G, Colgate, and Clorox to “bow their heads” and launch more small-package products to adapt to the “ten yuan shop” pricing strategy.

In addition to bulk purchase of branded products, “ten yuan shops” are also committed to developing their own brand products. dollar general has nearly 40 private label product lines. The development of its own brand is conducive to the company’s comprehensive control of production costs, independent pricing, and thus a higher profit margin.

The radical Chinese “ten yuan shop”: all the money is made by franchisees

After reading the “ten yuan shop” model in Japan and the United States, let us focus on the domestic market.

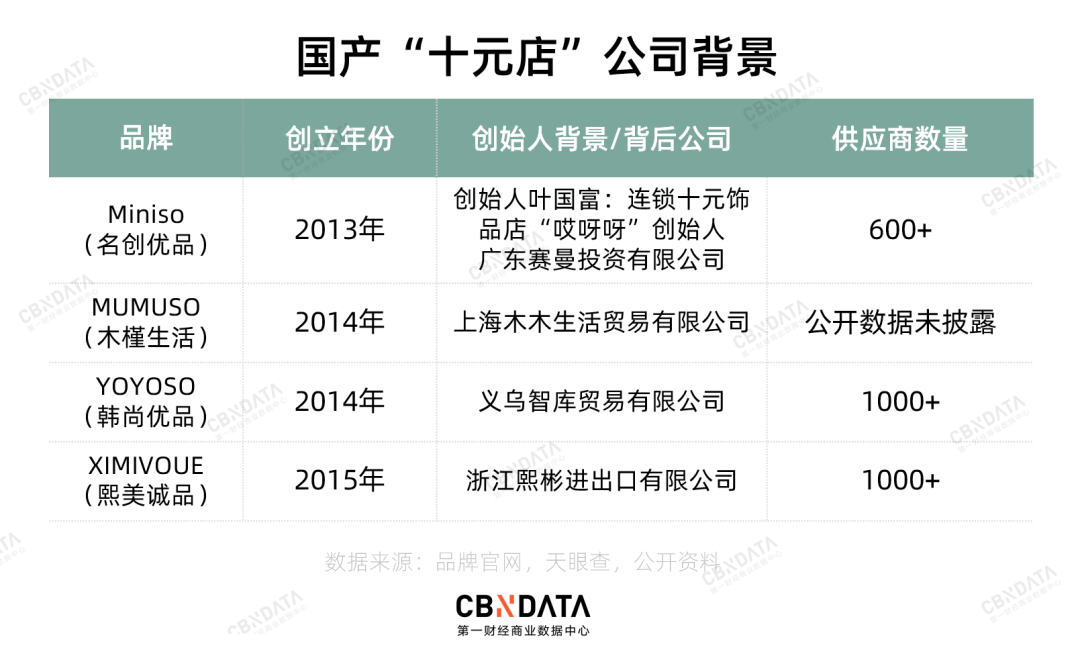

In addition to Miniso, there are also a large number of MUMUSO and YOYOSO in the “ten yuan shop” camp in China, who are stupid and unclear from name to logo.

In China’s “ten yuan shop”, do you know who is who? |Image source: network

Different from the US’s sinking market route, most of China’s “ten yuan stores” started in first- and second-tier cities, and are keen to open stores in densely populated commercial districts and transportation hubs. The styles of the shops and products are simple Japanese and Korean styles, and they belong to the household department store and lifestyle store that “sells good things” to consumers.

The location strategy of MINISO means high land rent costs. In 2017, Ye Guofu, the founder of MINISO, revealed in an interview that at that time, the investment cost of MINISO’s 300 direct-operated stores was close to 1 billion yuan, and the cost per store was more than 3 million. If you want to dilute operating costs, you can only strictly control costs on the product side.

In terms of products, China’s “Ten Yuan Store” has a huge lineup of private-label products. Relying on the strong domestic manufacturing industry, the “ten-yuan shop” directly connects with the foundry, and implements a demand-based production and bulk order model, which shortens the supply chain and reduces costs. It can also be seen from the company’s background that China’s “ten yuan shops” are all backed by the Jiangsu, Zhejiang, Shanghai and Guangzhou regions where the manufacturing industry is developed, and the supply chain advantages are self-evident.

The suppliers behind MINISO are all well-known | Source: MINISO official website< /p>

Different from the “Ten Yuan Store” in the US, which strictly controls SKUs, MINISO has spared no effort in product introduction. According to the prospectus, MINISO has more than 8,000 core styles in 11 categories, including household appliances, electronic appliances, bag accessories, beauty tools, toys, and leisure food. In 2020, on average, more than 600 new SKUs will be launched every month, and new products will be launched almost every week. The official websites of MUMUSO, XIMIVOUE, and YOYOSO claim that their monthly new volume is 800+, 800+, and 500+ respectively. Frequent new updates can continue to bring freshness to consumers and attract more customers to shop. This is consistent with Daiso’s thinking. And the direct connection with the foundry provides a guarantee for the new frequency.

With the US “ten dollar store” focusing on highThe repurchase rate of consumables is different. The high cost of land rent in China’s “ten yuan stores” and the characteristics of “selling good things” rather than daily necessities in big cities require them to maintain their stores through more new products and marketing methods Rate and repurchase rate.

For this reason, MINISO, XIMIVOUEXIMIVOUE and others have joined with Marvel , Kakao Friends, Bear infestation, Forbidden City culture and other well-known IP constructions at home and abroadLizheng version authorized cooperation; MUMUSO created the original cartoon IP family MUMUSO FAMILY, using gimmicks to create more reasons for consumers to spend money. In 2020, MINISO announced that Wang Yibo and Zhang Zifeng will become its brand’s global spokespersons and will spare no effort to attract young people. Compared with foreign down-to-earth “ten yuan stores”, domestic “ten yuan stores” obviously require higher marketing expenses.

In addition, the overseas expansion of domesticThe momentum is fierce. MINISO, which has been established for 7 years, has 1,680 overseas stores, accounting for about 40%. Although Daiso’s overseas stores also accounted for 39%, its overseas presence did not start until 24 years after the company was founded. The combined number of dollar tree and dollar general stores exceeds 30,000, and the scope of stores is still limited to North America.

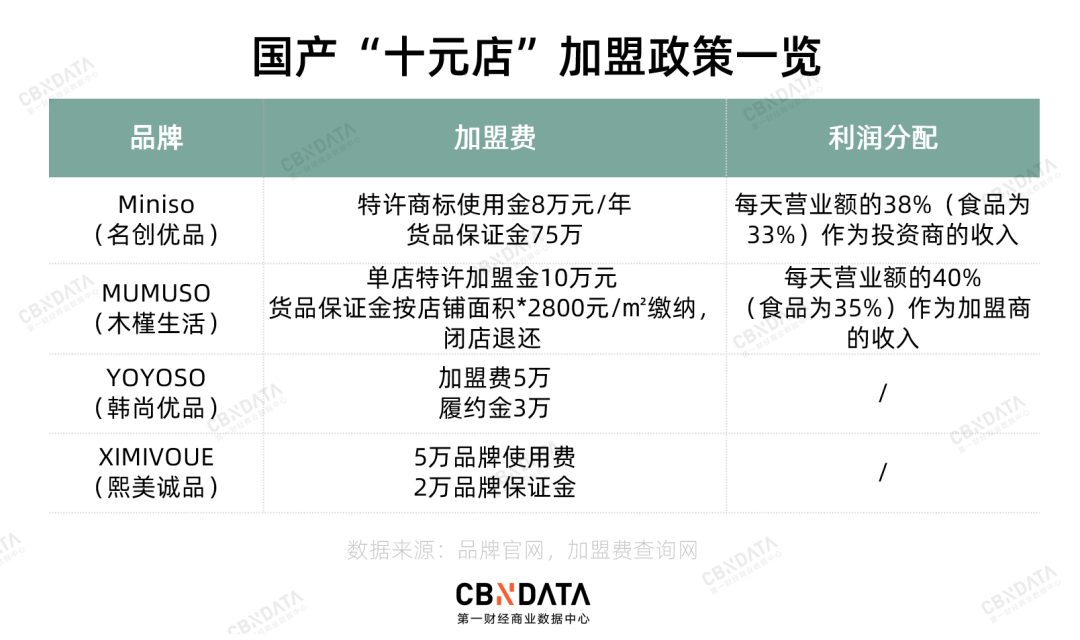

The aggressive overseas expansion stems from the aggressive opening of brands to franchise. If foreign “ten yuan shop” companies are directly doing consumer business, China’s “ten yuan shop” is more like an enterprise for small and medium entrepreneurs, earning money from franchisees-attracting with extremely high cost performance Consumer traffic, and then sell traffic to franchisees.

Only less than 3% of MINISO stores are completely self-operated. The self-operating rate of Daiso’s domestic stores in Japan is as high as 76%. XIMIVOUE、Hanshangyoupin YOYOSO has its own business school and is a franchisee Provide training and other various store support, and vigorously promote their complete store support system on the official website.

China-Japan-US PK: Which “ten yuan shop” model is more interesting?

In a nutshell, Japan’s “ten yuan store” mainly relies on creating low-margin high-quality explosive products to open the market, and then achieve profitability through the combination of high- and low-margin products.

The US “ten yuan shop” is targeting the sinking market, focusing on high-purchasing consumables. It strives to reduce operating costs by controlling land rent, strictly selecting products, bulk purchasing, and developing its own brands.To maintain profits.

The “Ten Yuan Store” in China started in first- and second-tier cities, relying on China’s complete manufacturing supply chain to develop its own brand products. Expand the business scope through global franchise to achieve mass production and sales.

The “ten yuan shop” model in each country has its own characteristics. In terms of scale expansion, especially worldwide expansion, which one is more promising?

Although Daiso’s road to sea is very smooth, it has encountered trouble in the Chinese mainland market. In 2012, Daiso officially entered mainland China, and its first stop was in Guangzhou. At that time, it also stated that it would open 20 stores in Guangzhou by the end of 2013, and finally plans to open 100 stores in Guangdong. But this goal was obviously not achieved. In 2018, Daiso’s distributor in the Guangzhou area, Sizhou Group, announced the termination of cooperation with Daiso. The latter completely withdrew from the Guangzhou market.

In the Shanghai area, all Daiso stores are self-operated. According to Baidu map, currently there are 7 Stores are open. However, Daiso continued its practice in Japan in terms of site selection, always choosing areas with lower rents—next to underground parking lots, the fourth and fifth floors of shopping malls, etc., to save shop opening costs. But in Shanghai, where foreign brands have to seize prime locations, Daiso’s low-key posture is not enough to make consumers in this city interested enough.

Daiso’s failure in the Chinese market is naturally related to the rise of MINISO products. One year after Daiso came to China, MINISO began to thrive. Half of the suppliers are from Daiso in mainland China, no matter in the supply chain or the rhythm of opening stores, it is difficult for this local brand to compete.

At present, China’s “ten yuan shop” is clearly ahead in the matter of going to sea. Will the Chinese model have more advantages?

According to the current overseas map of China’s “Ten Yuandian” brand, we can see that their layout is mostly in Southeast Asian countries and regions.

Because the factories in mainland China have been OEMs for foreign brands for a long time, it can be said that they have experienced many years of “training”. On this basis, the domestic “ten yuan shop” can develop rapidly under the premise of a smooth supply chain end.

And Southeast Asia also has long-term experience in OEM for major brands. Although the factory advantage is currently not as good as that of Chinese manufacturing, it is difficult to say whether there will be a local version in the futureThe “Ten Yuan Store” was born, blocking the expansion of Chinese MINISO.

China’s “Ten Yuan Store” is expanding in the world, Southeast Asia is an important position | Source: Brand Official Website

The gross profit margin is as high as 30%, but the “ten yuan shop” still has these problems

From the perspective of gross profit margin, “Ten Yuan Store” is a good business. MINISO’s prospectus shows that its gross profit margins for fiscal year 2019 and 2020 are as high as 26.7% and 30.4%, respectively, showing an upward trend. The gross profit margin of dollar general in 2019 is also 30.6%. It seems that the “ten yuan shop” with meager profits has achieved good operating data either through expansion of franchise or through strict cost reduction.

The considerable gross profit margin has attracted brands to follow suit. However, the “Ten Yuan Store” has some unavoidable crises.

First of all, low prices will obviously put a lot of pressure on revenue. Although the “ten yuan shops” are trying their best to control costs, nearly half of Daiso’s products are from China, and Dollar Tree’s financial report shows that about 40% of its products are imported. With such dependence on imported goods, once the “world factory” is no longer “cheap”, it is definitely bad news for the “ten yuan shop”.

Brands have also begun to expand the company’s revenue by acquiring and launching sub-line brands with higher unit prices.

On October 8 this year, dollar general announced that it will launch a new brand “Popshelf”. Although the unit price of 95% of the products of the new brand is still US$5 and below, the product type will focus more on non-essential products with higher gross profit. The target audience of the new brand has also changed-stores are planned to be located in the suburbs of first-, second- and third-tier cities in the United States, aiming at high-income hostesses.

Dollar tree acquired Family Dollar, a “ten dollar store” brand with higher prices, but the latter did not contribute excellent revenue to dollar tree.

According to The Sun report, Poundland, a long-established British “ten yuan shop” brand, also announced in October 2019 that it would abandon the price commitment of “Everything’s £1″ (one pound for all products), and the price of some products may be as high as 10 pounds. Although the brand claims that diversified pricing is conducive toAchieve high cost performance within a wide range of options”, but this cannot avoid the problem of the British retail industry being impacted by online shopping and the increase in store commercial rates.

Although the price of MINISO products is not as low as “ten yuan per piece”, Ye Guofu promised in April this year to implement a price reduction strategy: to control the price of more than 95% of MINISO products at 29 yuan Within, the price of newly developed products will be reduced by 20%-30%. The data shows that MINISO’s revenue in 2018 exceeded 17 billion yuan, but the prospectus showed that its revenue for the 2020 fiscal year (as of June 30, 2020) was 8.979 billion yuan, which is only more than half the level of 2018. In the case of weak revenue growth, further lowering the price, how the operating data of MINISO will perform afterwards is not yet known.

In addition, there are quality problems that are difficult to avoid for low-priced products. In April 2018, a hair dye of Daiso was found to contain carcinogens in Japan, and then 75 cosmetics were recalled independently. On the eve of the launch of MINISO, one of its nail polish products was detected by the Food and Drug Administration more than 1,400 times as a carcinogen. In 2018, its two blushes sold in South Korea were also detected to be 10 times more heavy metal antimony.

Can the “Ten Yuan Store” continue to be popular? Which model do you prefer?

Author| Zhang Xiaosha

Data, drawing| Zhang Xiaosha

Edit| Zhong Rui