The story of sunk costs.

Editor’s note: This article is from the WeChat public account “Haomaocaijing” (ID: haomaocaijing), author: Haomaocaijing.

This is the worst time for a domestic company to lose in a gambling performance.

Before and after the beginning of 2019, Ping An of China took over 25.25% of China Fortune fortune from Wang Wenxue’s China Holdings for a total price of nearly 18 billion yuan.

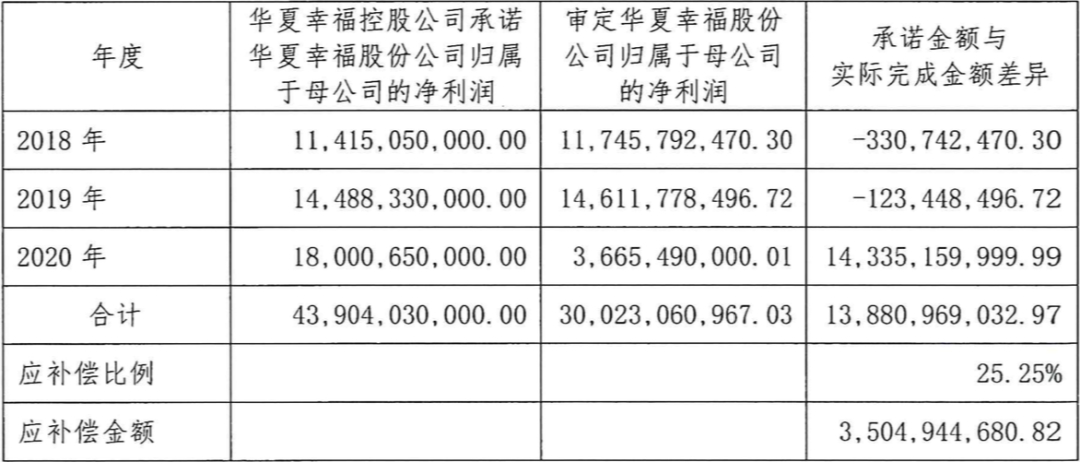

When Ping An became a shareholder, it signed a gambling agreement with Huaxia Holdings, stipulating that the net profit attributable to the parent for 2018-2020 will not be less than 1.142 billion yuan, 1.448 billion yuan, and 1.8 billion yuan.

This time the profit compensation is retrospective. Any year’s net profit does not reach 95% of the expected target, which triggers the profit compensation mechanism.

Compensation amount = (accumulated committed net profit as of the end of the current period-accumulated actual net profit as of the end of the current period) × 25.25% of the shares held by Ping An.

The latest 2020 financial report of Huaxia Holdings shows that the amount of compensation for Ping An’s profits by Huaxia Holdings should be:

3.505 billion yuan.

If the money can be paid smoothly, and Ping An has received nearly 6 billion yuan in dividends from China Fortune in the past two years, Ping An’s equity investment will receive 9.5 billion yuan in cash.

Obviously, China Holdings is currently unable to pay this debt.

Of course, Ping An knows well that it has accrued 18.2 billion yuan in impairment for its 18 billion yuan equity investment and 36 billion yuan debt investment.

As of the end of 2020, China Holdings’ unrestricted cash was only 134 million yuan; as of May 12, China Holdings also defaulted on 1.15 billion yuan in debt.

This default debt is not a credit bond. A bond recently due by China Holdings will be redeemed at the end of November, with a balance of 1.455 billion yuan.

There is a very serious question, that is, where did the 18 billion yuan of Huaxia Holdings’ conversion income go? Why did Wang Wenxue’s business empire end there?

The financial statements of Huaxia Holdings give the answer: Wang Wenxue’s radical investment has lost all this money.

In addition to the consolidated statement of China Fortune, China Holdings has almost no other day-to-day business operations and is an investment platform for pooling funds.

As of the end of 2020, in the balance sheet of China Asset Management’s parent company, current assets were 14.36 billion yuan, of which other receivables were 13.81 billion yuan.

Continuing to dismantle, we can see that 95% of the 13.81 billion yuan is due from “Zhihe Holdings” and its parent company, which is another corporate platform of Wang Wenxue Private Holdings.

In other words, Zhihe Holdings still owes China Xia Holdings tens of billions of funds. If these tens of billions of funds are in place, China Xia Holdings’ debt should not default.

Zhihe Holdings is the controlling shareholder of Visionox (002387.SZ), a listed display panel company.

More than two months ago, Zhihe Holdings sold some of its shares in Visionox for 11 yuan per share for a total price of 1.76 billion yuan. It is most likely to raise funds for the debt repayment of China Holdings.

At the end of 2015, Zhihe Holdings became the controlling shareholder of Visionox for nearly 7 billion yuan, and the ownership cost was as high as 15.31 yuan per share. The sale of some shares this time is a visible “survival with broken arms.”

Visionox is the best example of Wang Wenxue’s investment failure.

In 2015-2017, China Holdings and Zhihe Holdings, controlled by Wang Xuewen, started a crazy investment model and entered manufacturing, finance, travel, new energy vehicles and other industries one after another.

By the end of 2017, at the parent company level of China Asset Management, it was already unable to make ends meet. Interest-bearing liabilities exceeded 32 billion yuan that year, while monetary funds were only 1.1 billion yuan.

It seems that Wang Wenxue’s sale of equity to Ping An in 2018 was indeed anxious to save China Holdings. In the next three years, China Holdings repaid nearly 17.5 billion yuan of interest-bearing debt.

China Holdings, Zhihe Holdings, and China Fortune Land Development were almost wiped out in the last cycle due to strategic misjudgments and business models.

Looking back, I can understand why Ping An got stuck in it.

Wang Wenxue is an ambitious businessman who is eager to cash in. China Fortune Land Development is a platform for investing hundreds of billions in Chinese real estate. These two points are where Ping An’s determination to become a shareholder lies.

But neither Wang Wenxue nor Ping An expected two things:

First, the business of China Fortune Land Development is a strong cash flow business, but the regulation of the property market that has swept across the country has persisted for four years, which has seriously affected the recovery of China Fortune Land Development’s cash flow. The epidemic is only the last blow;

Second, China Fortune Land Development’s accounts receivable from the government will add up to more than 60 billion yuan. The proportion of accounts receivable in the current assets of China Fortune Land Development rose from 4.2% in 2016 to 14.3% in 2020.

Of course, the second point may be that Ping An doesn’t know. Wang Wenxue knows well, but Ping An never imagined that Wang Wenxue would be so obsessed with the new industrial city, so full of gambling.

Maybe Wang Wenxue should learn from Ping An, as the sunk costs are irreversible.